DEEP RESEARCH · G2GBIO

G2GBio: Long-Acting DDS Moat and Commercialization Inflection

An analysis of the InnoLAMP microsphere platform, IPO funds, GB-5001/GB-7001 pipelines, and patent risk

0. Bottom line first

G2GBio is trying to connect its InnoLAMP microsphere platform to commercial production in long-acting injectables. The technical points are sustained efficacy and scalable manufacturing; the investment checkpoints are the second GMP plant in 2027, core pipeline licensing, and FTO after the semaglutide patent dispute.

Official fact: The source says G2GBio was founded in March 2017 and listed on KOSDAQ as a technology-growth special-listing company on August 14, 2025. The IPO price was set at 58,000 won, the top of the 48,000-58,000 won range, and total offering proceeds were KRW 52.2bn.

Interpretation: This is not yet an earnings stock. It is a platform stock based on production technology, clinical options, and licensing options. Patent and overhang risks still require long-horizon verification.

1. Company overview and IPO structure

G2GBio was founded in March 2017 around CEO Lee Hee-yong. The source describes him as a specialist who served as research center head and executive director at Peptron and spent 27 years researching long-acting medicines. The company raised KRW 8bn in Series A in 2018, KRW 11.4bn in Series B in 2020, KRW 2bn bridge financing in 2021, and KRW 14.6bn in Series C in 2022.

| Item | Details | Note |

|---|---|---|

| Final IPO price | 58,000 won | Top of range |

| Offer shares | 900,000 shares | All new shares |

| Total offering | KRW 52.2bn | KRW 52,200,000,000 |

| Allocation | Institutions 68.3% / retail 30.0% / employee stock 1.7% | Institutions 614,700 shares, retail 270,000 shares |

| Bookrunner | Mirae Asset Securities | Firm commitment underwriting |

Official fact: The source says about KRW 50.4bn after issuance expenses will be used for mid- to long-term growth. Facility funds for the second GMP plant are presented as about KRW 21.7bn in one paragraph and about KRW 24.7bn in a later funding-use section. Clinical and scale-up research costs are about KRW 12bn, and research staff plus operating funds are about KRW 13.6bn.

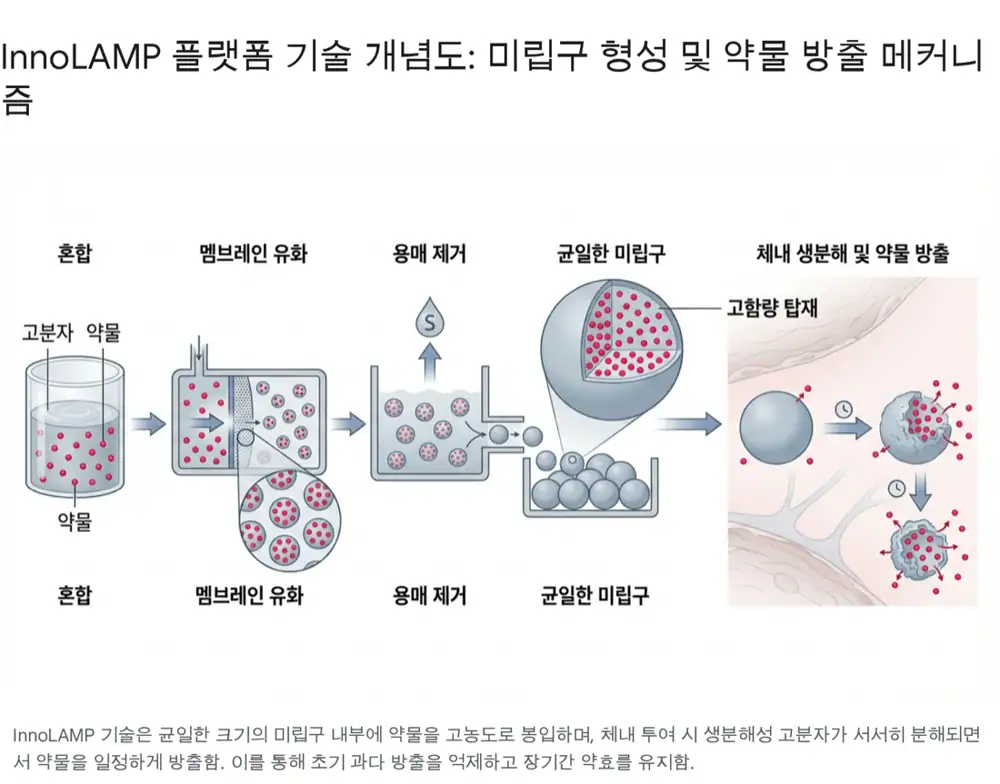

2. Core technology: InnoLAMP microsphere platform

InnoLAMP stands for Innovative Long-Acting Microsphere Platform. It uses biodegradable polymers such as PLGA and PLA to encapsulate drugs and release them slowly in the body. Existing microsphere technology has clear limits: initial burst release, low drug loading, complex manufacturing, and difficult scale-up.

Drug content 100-200%

The source says drug content is raised versus competing technologies, reducing total injected microsphere volume by more than 40%.

Zero-order profile

The platform aims to suppress initial burst release and reduce foreign-body reaction with an anti-inflammatory co-platform.

10-20kg pilot equipment

The current pilot setup is estimated by the source to produce doses for about seven million people.

3. Competitive technology comparison

| Category | G2GBio InnoLAMP | Peptron SmartDepot | Inventage Lab IVL-DrugFluidic |

|---|---|---|---|

| Base technology | Membrane emulsification + continuous solvent removal | Ultrasonic spray drying | Microfluidics |

| Strength | High loading, easy mass production, uniform particles | Fast solvent removal, continuous process possible | Excellent particle uniformity, initial-release control |

| Weakness | Complex process-variable control | Protein-denaturation risk from high-temperature exposure | Production speed and scale-up difficulty |

| Main pipeline | GB-5001 dementia, GB-7001 obesity | PT403 obesity, PT320 Parkinson’s | IVL3021 obesity, IVL3003 dementia |

Interpretation: Peptron has production-speed advantages, and Inventage Lab has particle-uniformity advantages. G2GBio is trying to balance mass production and high loading. For high-demand drugs such as GLP-1 obesity therapies, cost-competitive mass production can decide CDMO wins.

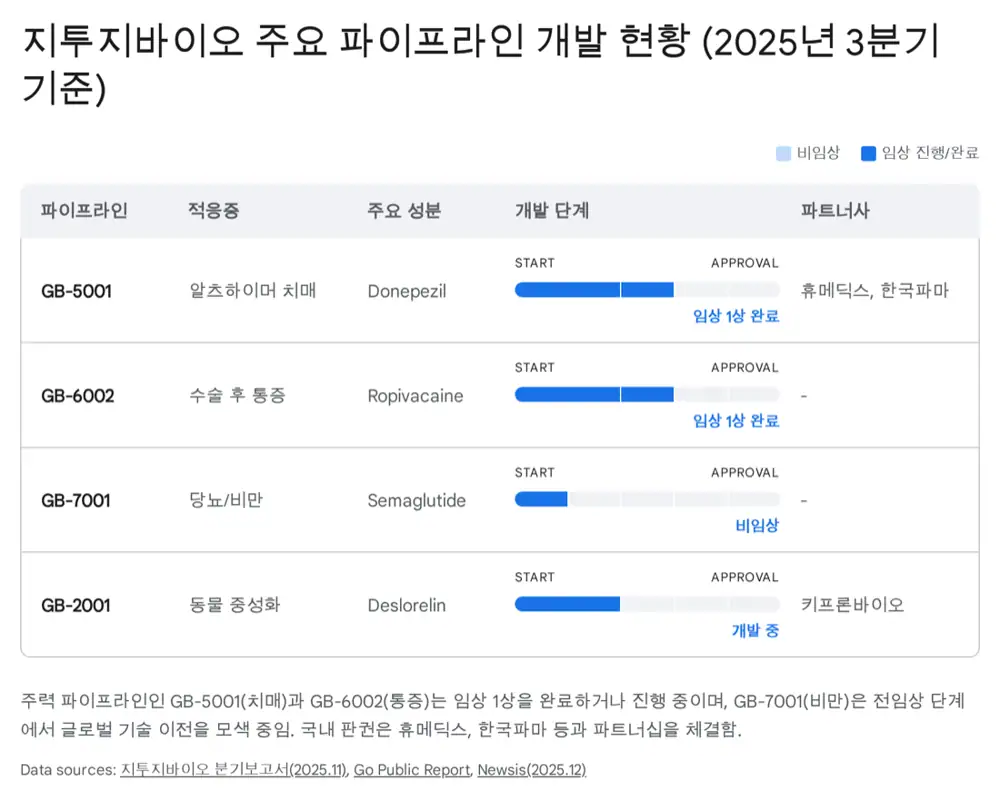

4. Key pipelines

| Pipeline | Disease/drug | Source detail |

|---|---|---|

| GB-5001 | Once-monthly donepezil for Alzheimer’s | Canada phase 1 IND approval in Oct. 2021, Korea/Canada phase 1 completed, blood half-life 3-4x longer than oral drug |

| GB-7001 | Once-monthly semaglutide for obesity/diabetes | Preclinical efficacy confirmed, ADA data presented, licensing and joint research discussions with multiple global pharma companies |

| GB-6002 | Ropivacaine for post-surgical pain | Phase 1 confirmed 72-hour pain relief and safety, AUC maintained and Cmax reduced |

Official fact: The source says the global Alzheimer’s therapeutics market is expected to grow at about 9.8% annually through 2032. It also cites the global injectable drug delivery market reaching about USD 823.3bn by 2030.

GB-5001 includes domestic licensing and co-development contracts with Korea Pharma and Humedix. GB-7001 rides the GLP-1 market growth theme, but the extinguishment of semaglutide manufacturing patent No. 2375262 is a key risk.

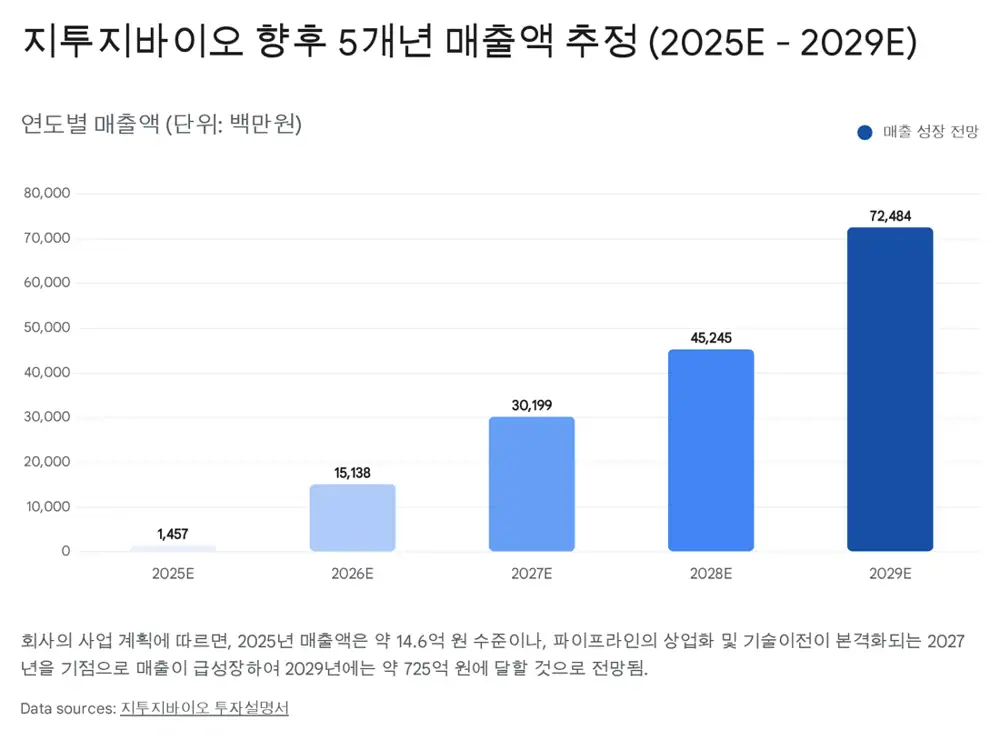

5. Financials and funding use

G2GBio has the early financial profile of a technology-special-listing company. 2025 Q3 cumulative revenue was about KRW 220mn, and full product-sales revenue has not yet begun. Most revenue comes from time-recognized license upfronts or small research-service income.

| Item | Source figure | Checkpoint |

|---|---|---|

| 2025 Q3 cumulative revenue | About KRW 220mn | Pre-commercial revenue stage |

| Accumulated deficit at end-2024 | About KRW 129bn | Accumulated R&D burden |

| Cash before listing, 2025 Q1 | About KRW 7bn | Pre-IPO liquidity |

| IPO proceeds | KRW 52.2bn | Near-term liquidity risk eased |

| Second GMP plant | Expected completion in 2027 | Core for commercial production and CDMO expansion |

Interpretation: The IPO proceeds are both survival capital and production-capacity capital. Because microsphere formulations require dedicated production equipment, the 2027 second-plant ramp will determine how real the platform value is.

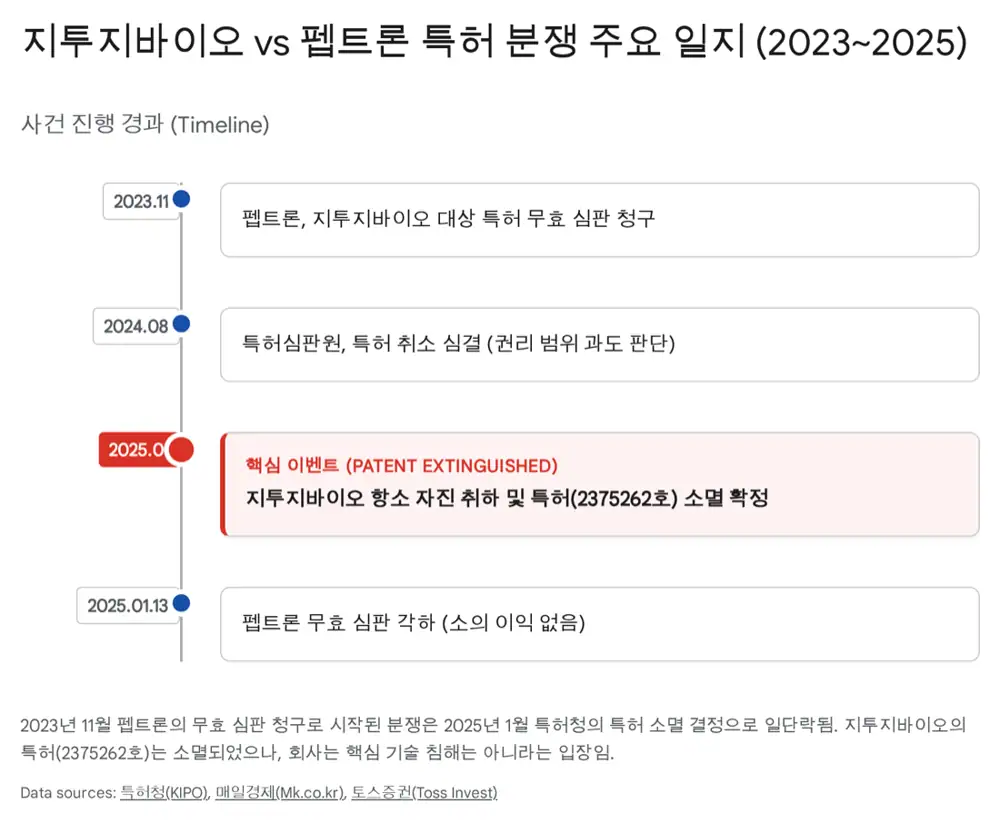

6. Risks: patent, overhang, clinical execution

- Patent dispute: In January 2025, the Korean patent office extinguished G2GBio’s semaglutide-related patent No. 2375262. The source ties this to a dispute with Peptron and says the rights scope was judged excessively broad.

- FTO check: The company says commercialization of core pipelines is not affected, but investors must verify follow-on patent strategy and freedom to operate.

- Overhang: VC and financial-investor exit shares can appear after a technology-growth special listing, and some lock-ups are short at one to three months.

- Clinical and licensing risk: GB-7001 faces intense global big-pharma competition, so differentiated clinical data and timely licensing will drive value.

7. My conclusion

G2GBio is targeting the long-acting DDS market through the InnoLAMP platform. Patent disputes and overhang remain near-term burdens, but the second plant, CDMO ramp, and licensing outcomes for GB-5001 and GB-7001 can become long-term valuation inflection points.

The right checklist is CAPEX execution, GMP capacity, global partnerships, and FTO strategy, in that order.

Sources

- Naver Blog source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224124621820

- Grand View Research - injectable drug delivery devices: https://www.grandviewresearch.com/industry-analysis/injectable-drug-delivery-devices-industry

- NIH - long-acting GLP-1 receptor agonists: https://pmc.ncbi.nlm.nih.gov/articles/PMC7035886/

- G2GBIO History: https://www.g2gbio.com/en/m11.php?section=1

- Global Market Insights - Alzheimer therapeutics market: https://www.gminsights.com/ko/industry-analysis/alzheimers-therapeutics-market

- Press9 - 월 1회 치매주사제 임상 성공: https://www.press9.kr/news/articleView.html?idxno=69483

- Newsis - InnoLAMP 상업성 시험대: https://mobile.newsis.com/view/NISX20251226_0003455067

- ADA - Semaglutide Depot 1689-P: https://diabetesjournals.org/diabetes/article/74/Supplement_1/1689-P/158525/1689-P-Semaglutide-Depot-a-Long-Acting-Injection

- ADA - microsphere formulation 641-P: https://diabetesjournals.org/diabetes/article/70/Supplement_1/641-P/140600/641-P-Novel-Microsphere-Formulation-Developments

- MK - Z2G Bio patent extinguished: https://www.mk.co.kr/en/it/11219675

- 토스증권 - 비만치료제 특허 소멸: https://www.tossinvest.com/news?contentType=news&contentParams=%7B%22id%22%3A%22maekyung_000011219675%22%7D

- Sportal Korea - GB-6002 안전성 확인: https://www.sportalkorea.com/news/articleView.html?idxno=2025052909552847921