DEEP RESEARCH · JS Link (127120.KQ)

JS Link Deep Dive: From Genomics Company to "Non-China Rare-Earth Permanent Magnet" Strategic Materials Maker

Orbitech exits → Juseong CN Air takes over → Korea (Yesan) · Malaysia (Kuantan) · US (Georgia) tri-pole production — pairing Lynas feedstock with IRA tailwinds to reposition as a supply-chain security play

0. Bottom line first

JS Link is no longer a "bio theme" stock. As of 2025, it has fundamentally swapped identities — genomics company → NdFeB rare-earth permanent magnet maker. After Orbitech's financial exit (invested ~KRW 9B → recovered ~KRW 30B), logistics specialist Juseong CN Air took control and is now standing up a Korea-Malaysia-US tri-pole production network. The core positioning: fill the "Non-China" supply-chain void created by US-China rivalry as a security partner.

Official fact: China controls >90% of rare-earth mining, refining, and magnet manufacturing. On 2025-01-07 Juseong CN Air acquired 3,192,341 shares (14.20%) of JS Link for ~KRW 23.94B (~KRW 7,498/share); a subsequent KRW 20B third-party private placement lifted stake to 24–26%. In July 2025, signed an MoU with Australia's Lynas for a 3,000-tonne/year magnet plant in Kuantan, Malaysia. In September 2025, announced an ~USD 223M (~KRW 300B) 3,000-tonne plant in Columbus, Georgia — ~520 jobs, target operation late 2027.

Interpretation: Seven straight years of operating losses + negative operating cash flow = the company cannot fund operations from earnings, let alone CAPEX — yet a ~KRW 590B market cap already prices in much of the magnet-business success. Macro tailwinds (China tightening + IRA + CRMA) are clearly favorable, but execution — Yesan yield ramp, Lynas definitive contract, US subsidies, OEM supply deals — is the litmus test.

1. Overview — a textbook "Strategic Pivot"

JS Link's recent moves go far beyond a rename or diversification. They are a strategic pivot that rewrites identity and viability. Founded in 2000 as a genomics / precision-medicine company, JS Link veered hard into NdFeB magnet manufacturing in 2025.

Two forces converge — (1) chronic losses and growth limits in the legacy biotech, and (2) a "de-China" rare-earth value chain opening up via US-China rivalry. NdFeB magnets are the "heart" of EV traction motors, wind turbines, defense, and UAM — demand is exploding — but supply is >90% Chinese. That fault line is JS Link's opportunity.

1.1 Milestone timeline

| Date | Event |

|---|---|

| 2024-11 | Purchased Yesan factory site in Chungnam |

| 2025-01-07 | Share Sale-Purchase Agreement signed with Juseong CN Air |

| 2025-03 | Name change (DNA Link → JS Link), bylaw amendment, Yesan groundbreaking |

| 2025-07 | MoU with Lynas for Kuantan, Malaysia magnet plant |

| 2025-09 | Yesan pilot production + Georgia investment announcement |

| 2025-11 | Yesan plant occupancy approval |

2. Governance overhaul — Juseong CN Air arrives, Orbitech exits

2.1 End of the Orbitech era — a financial exit

Orbitech (nuclear-plant inspection + aerospace precision parts) became DNA Link's largest shareholder via a third-party share issue in November 2023. The market hoped for precision-machining × biotech convergence, but practical integration was minimal. Orbitech expanded to 21.1% via CB purchases, then abruptly chose to exit in early 2025.

Official fact (estimate): Orbitech invested ~KRW 9B in DNA Link → recovered ~KRW 30B (control-premium share sale ~KRW 24B + CB gains). 3x+ return — a successful exit.

Interpretation: Rather than absorb the huge CAPEX risk of the magnet pivot, Orbitech harvested a near-PE-style return.

2.2 The new owner — Juseong CN Air

International freight forwarder

Founded Feb 2008, private. Sea & air cargo forwarding. Strong on the North America corridor — ranked ~25th globally among North America export forwarders.

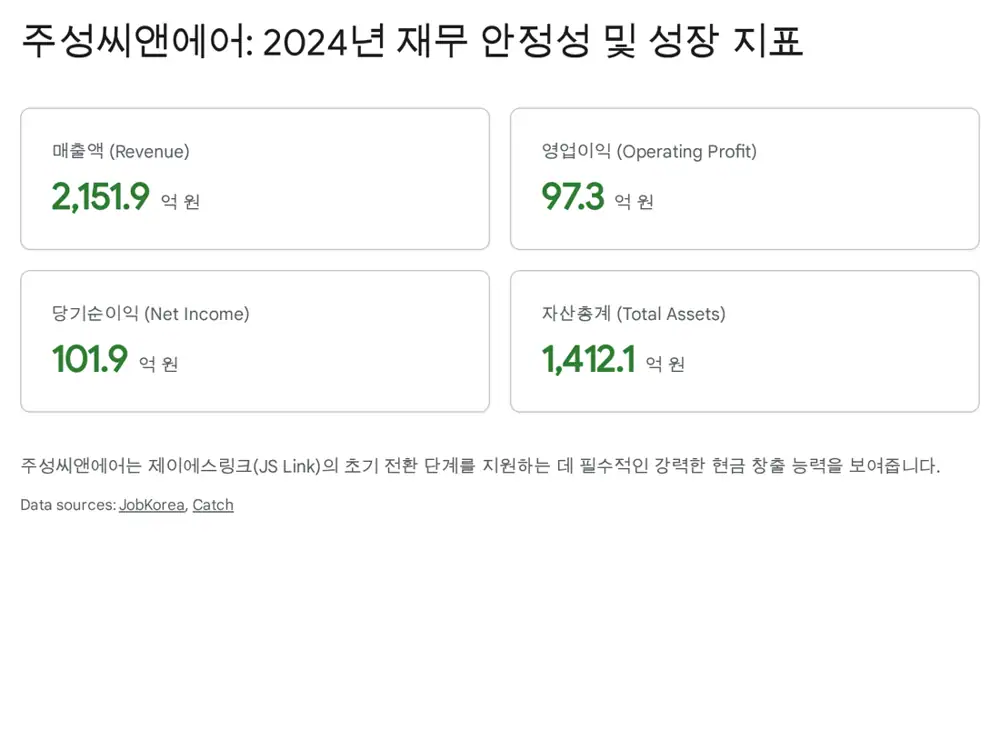

KRW 215.19B

Operating profit KRW 9.73B · net income KRW 10.19B · total assets KRW 141.2B. Cash-flow / WATCH ratings solid.

LA/Long Beach hub

Partnered with Busan Port Authority for US-side logistics. Immediately after the acquisition, signed lobbying agreement with US law firm Baker & Hostetler LLP.

2.3 Acquisition logic — "logistics × resources" synergy

- Internalizing supply-chain logistics: Lynas → Korea/Malaysia processing → US export is a complex movement of materials. Juseong CN Air can capture this as a captive flow and grow its own revenue.

- North America network: Reduces the early-entry friction for the Columbus, Georgia plant.

- Government affairs & lobbying: The Baker & Hostetler engagement is a foothold for securing IRA tax credits and DoD grants — a speed only possible with a globally savvy parent.

3. Why pivot — genomics to permanent magnets

3.1 Structural limits of the legacy biotech

For 20+ years JS Link ran disease-prediction and diagnostic services on genomics. But the small Korean market, fierce competition, and high R&D burden produced seven consecutive years of operating losses. The 3Q 2025 report still shows operating losses + continuing negative operating cash flow. Management concluded that biotech alone cannot lift corporate value — or even ensure survival.

3.2 The rare-earth magnet "super-cycle"

- Demand explosion: EV traction motors, offshore wind turbines, robotics, UAM — permanent magnets are no longer "industry vitamins" but the "industry heart".

- Supply crisis: China holds >90% of mining + refining + magnet manufacturing and uses it as a resource-weapon lever.

- De-China opportunity: US IRA and EU CRMA introduce massive subsidies and rules to reduce China dependence — opening a wide door for non-China players.

4. Operations strategy — a tri-pole global production system

4.1 Yesan (Chungnam) — domestic tech hub

- Location/scale: Ochuri, Godeok-myeon, Yesan-gun; 10,208 m². Broke ground March 2025, occupancy approval November 2025.

- Capacity: 1,000 tonnes/year — enough for ~500k EV traction motors.

- Status: Major equipment (large smelting furnaces for alloy flake precursor) installed by Sep 2025; pilot production underway. Samples will be supplied to Hyundai Motor, Kia, and other domestic / overseas customers for qualification.

- Tech: Recruited Japanese magnet expert Kenji Konishi (and others) to acquire sintering and grain-boundary diffusion know-how.

4.2 Kuantan, Malaysia — feedstock proximity (Lynas JV)

- July 2025 MoU with Australia's Lynas for a 3,000-tonne/year magnet plant in Kuantan.

- Adjacent to Lynas's LAMP refining facility → immediate oxide supply, lower logistics cost, total feedstock stability.

- Malaysian PM Anwar Ibrahim noted JS Link has completed site purchase and finalized investment — the project has moved past MoU into execution.

4.3 Columbus, Georgia (USA) — market beachhead

- ~USD 223M (~KRW 300B) investment, 3,000 tonnes/year, ~520 jobs, target operation late 2027.

- Heart of the US "Battery Belt" — Hyundai HMGMA + SK On and other battery cell makers cluster nearby.

- US production satisfies IRA critical-mineral / component rules — DoD / DOE grants are expected, with federal-government talks underway.

5. Financials — the bright and dark sides of mega-investment

5.1 Cash flow and profitability

The 3Q 2025 report still shows operating losses. Biotech weakness continues, while magnet-business hiring, R&D, and CAPEX prepayments inflate SG&A and CAPEX. Operating cash flow remains negative — the company can't cover operations from earnings, let alone investment. External funding is a survival condition.

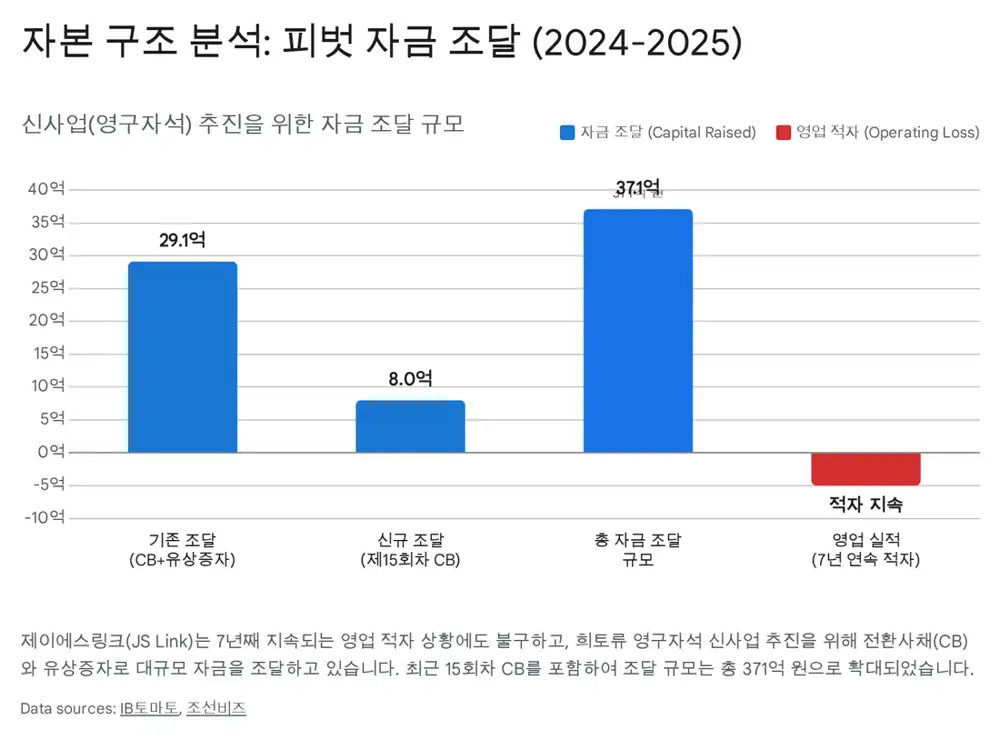

5.2 Aggressive financing — CB + private placements

- Convertible bonds: Multiple issuances from 2H 2024 through 2025. The 15th-series CB and others raised ~KRW 37.1B. Interest cost is low but conversion creates dilution overhang; refixing clauses also add downside-conversion risk.

- Private placement: Third-party allotment to Juseong CN Air for KRW 20B — improved capital structure and entrenched control, but minority dilution.

5.3 Market view and risks

Market cap ~KRW 590B — rich for a loss-maker; magnet-business success is largely priced in. Risks to monitor:

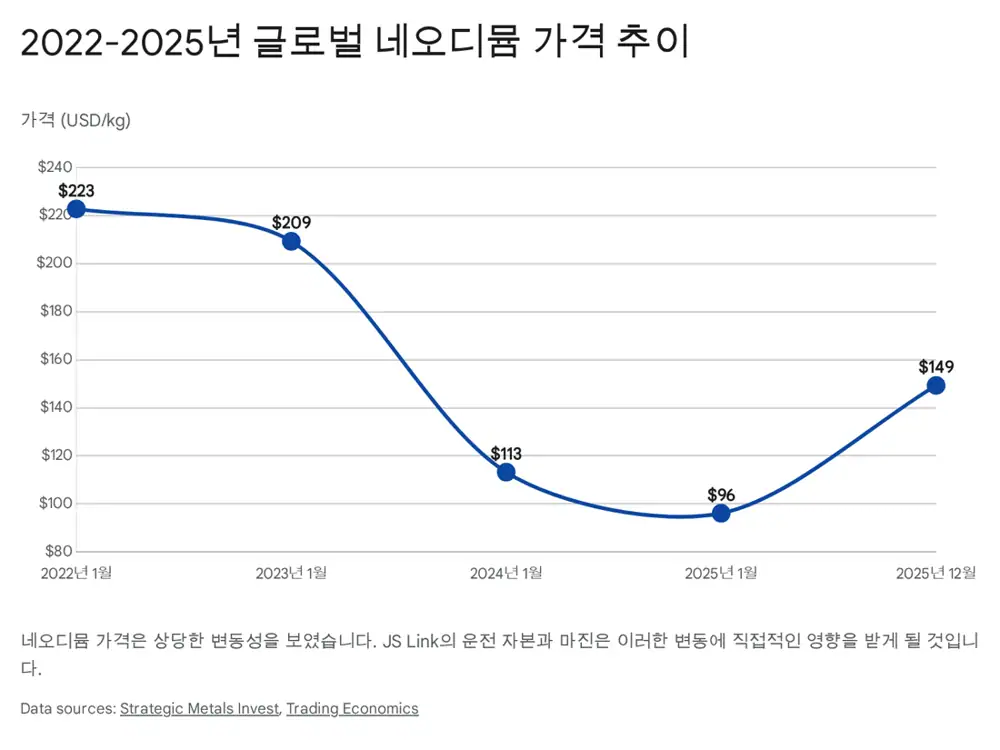

- Neodymium price volatility: Off 2022 peaks, recently bouncing — sharp spikes raise working-capital pressure.

- Execution capability: Can a former biotech ramp the precision-controlled sintering process to stable yields fast enough? The "Valley of Death" between pilot and mass production is the binary question.

- Geopolitics: Tightening Chinese controls boost JS Link's value, but a US-China thaw or Chinese dumping would erode price competitiveness.

6. Conclusion & outlook

JS Link is making the most dangerous yet most compelling bet in its corporate history. Shedding the biotech shell and diving into the front line of the global supply-chain war is timely. The Orbitech exit and the Juseong CN Air arrival are not a routine ownership swap — they mark JS Link's evolution from an "investment vehicle" into a "real manufacturing + logistics platform".

Juseong CN Air's logistics + Lynas's feedstock + the Yesan-Kuantan-Columbus triangle — on paper a perfect "Non-China supply chain" puzzle. But the only thing that turns theory into reality is execution:

- Yesan yield stabilization

- Definitive Lynas contract

- Securing US government subsidies

- Supply contracts with global OEMs

Investors should track financial health (need for further funding) and watch quarterly disclosures for the timing of first magnet-business revenue and order wins. JS Link is no longer a biotech theme — it now stands before the market as a "supply-chain security" stock leveraging geopolitical risk into opportunity.

Sources

- Naver blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224124579147

- Seven years of losses, new owner takes on building first — Chosunbiz: article

- Juseong CN Air 2025 company info — JobKorea: profile

- Juseong CN Air becomes DNA Link's largest shareholder — ThePublic: article

- JS Link control change SPA — KRX Disclosure: disclosure

- JS Link KRW 20B third-party private placement — MarketIn: article

- DNA Link begins US lobbying — NewsDream: article

- Korea's global supply-chain diversification strategy: material

- China's 94% rare-earth magnet monopoly — esnews: article

- JS Link to set up 3,000t magnet plant in Georgia — Daum: article

- JS Link Yesan plant — Sankun: info

- JS Link Plans New Magnet Plant in Georgia — Magnetics Magazine: article

- Kenji Konishi patents — Justia: profile

- Lynas bolstered by rare-earths deal — Australian Mining: article

- Lynas signs MoU with JS Link — ASX: PDF

- Malaysia PM on $142M magnet plant — MINING.COM: article

- JS Link America $223M in Georgia — MINING.COM: article

- Gov. Kemp on Korean Magnet Facility — Georgia gov: press release

- JS Link CB / capital raises — IBTomato: article

- JS Link price — AlphaSquare: chart

- Neodymium Price — Strategic Metals Invest: data

- Neodymium — Trading Economics: data