DEEP RESEARCH · GREEN RESOURCE

Green Resource: An Enabler for Advanced Nodes and Fusion Energy

A review of SD specialty coating, superconducting wire equipment, and the quality of Q3 2025 earnings.

0. Bottom line first

Green Resource looks less like a simple coating company and more like a vertically integrated materials, equipment, and process provider targeting both semiconductor etch-yield problems and superconducting-wire productivity for fusion. But the Q3 2025 revenue surge must be separated by quality because trading revenue was a major driver.

Materials-equipment-process integration

The company links fine-powder synthesis, coating-equipment design, and custom process recipes.

SD coating and IBAD

Advanced etch environments below 5nm and superconducting-wire equipment are long-term options.

Margin dilution

The Q3 2025 revenue jump was heavily affected by a higher trading mix.

1. Technology moat: SD specialty coating

Official fact: The source says Green Resource was founded in 2011, built rare-earth-based functional-material capabilities, and localized protective coating powder for semiconductor and display plasma etch equipment in 2013.

Interpretation: The key point is not only coating service, but a Total Solution Provider model covering materials, PVD/APS equipment, and process recipes.

| Item | Conventional APS | Green Resource SD coating |

|---|---|---|

| Microstructure | Porous and rough | Dense and smooth |

| Porosity | About 1-3% | <0.1%, near zero |

| Hardness | 600-800 Hv | 1,000-1,200 Hv or higher |

| Etch rate/lifetime | Corrosion-resistance limits | Potential 3-5x longer replacement cycle |

| Use cases | Legacy processes | Advanced 5nm, 3nm, and 2nm processes |

2. End markets: semiconductors and fusion

In foundry, 2nm competition among TSMC, Samsung Electronics, and Intel, together with GAA adoption, increases demand for protective coatings on etch-chamber parts. In memory, 3D NAND moving beyond 300 layers toward 400 and 500 layers lengthens high-aspect-ratio etch time and structurally increases parts consumption.

IBAD equipment for superconducting wire is the option that could re-rate the company as a fusion-equipment name. The source highlights technology that widens wire from 12mm to 120mm, potentially improving productivity by more than 10x.

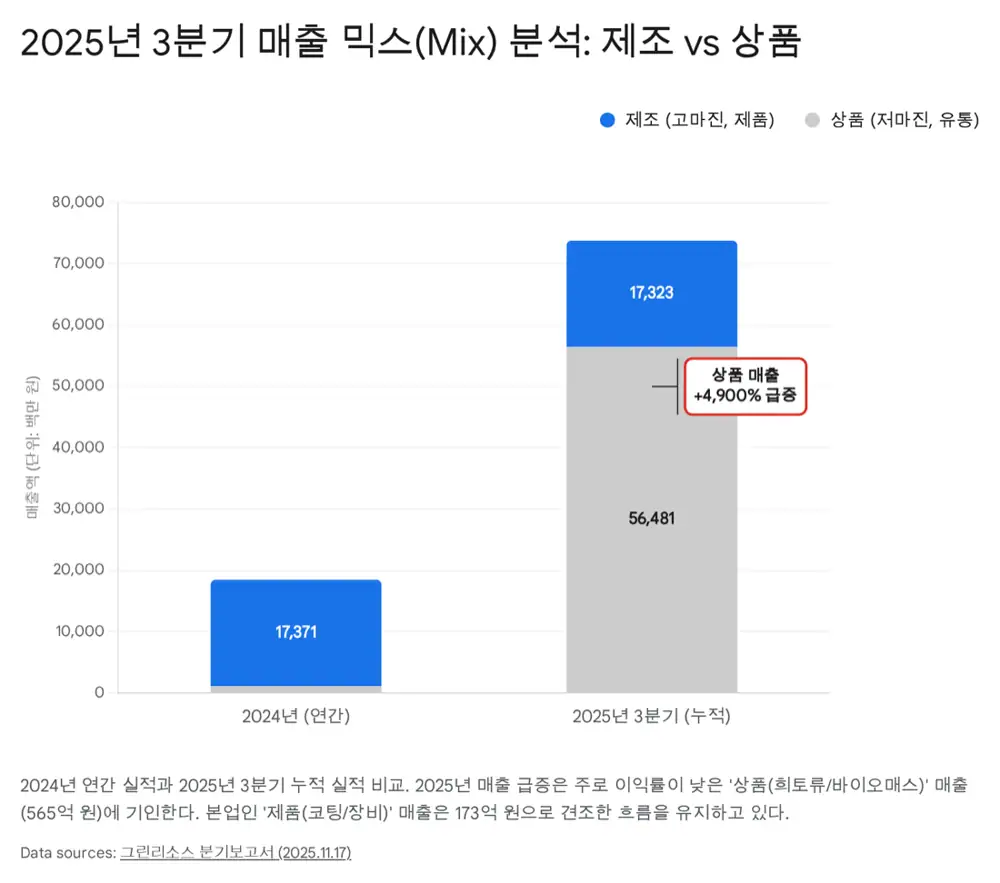

3. Q3 2025: separate size from quality

Official fact: Q3 2025 cumulative revenue was KRW 73.8bn, up 299% from KRW 18.5bn a year earlier, and operating profit was KRW 3.6bn, up 236% from KRW 1.07bn.

| Category | Source figure | How to read it |

|---|---|---|

| Products/manufacturing | KRW 17.3bn | Nearly matched full-year 2024 revenue of KRW 17.4bn in three quarters |

| Goods/trading | KRW 56.5bn, about 76% of total | Driven by biomass and rare-earth raw-material trading |

| OPM | 9.8% in 2024 to 4.9% in Q3 2025 | Diluted by lower-margin goods revenue |

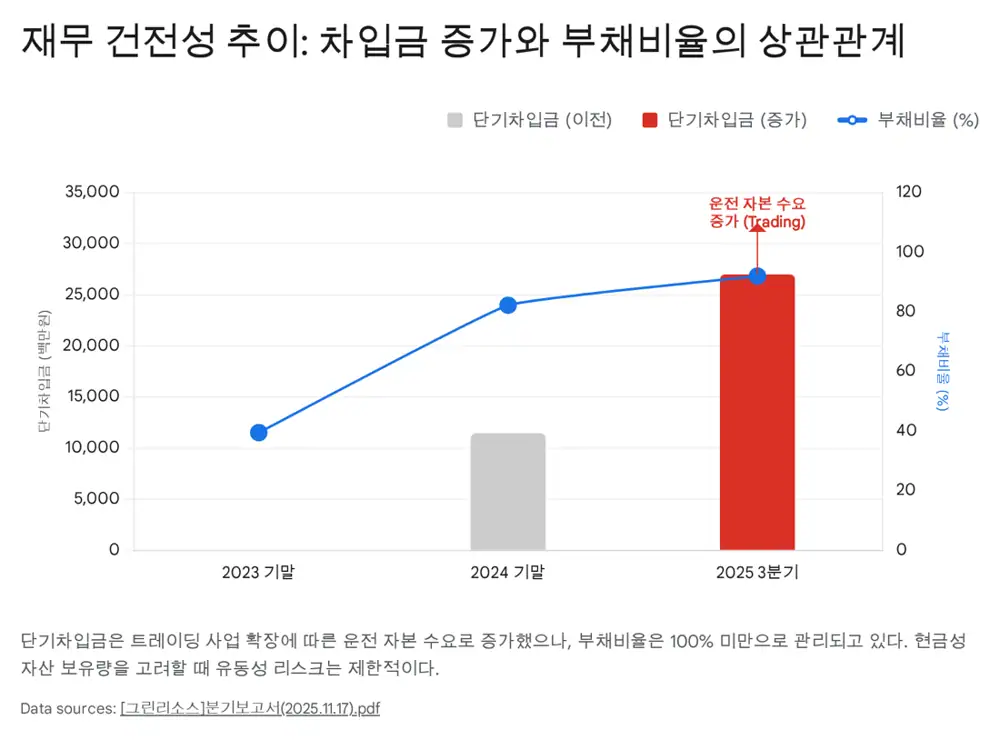

| Current borrowings | About KRW 27.0bn, more than double KRW 11.5bn at year-end | Working capital and Cheongna new-factory investment |

Interpretation: I read these numbers as a portfolio-transition phase more than a simple profitability breakdown. Still, the key checks are whether manufacturing mix rises again and borrowings are managed.

4. Valuation and monitoring points

The source puts market cap around KRW 130bn and share price around KRW 7,900. Annualizing Q3 cumulative net income of KRW 11.8bn implies about KRW 15.0bn of 2025 net income and a P/E of roughly 8.7x, below the KOSDAQ semiconductor materials/components/equipment average of 12-15x.

- Whether semiconductor recovery raises the high-margin manufacturing mix.

- Whether additional superconducting-wire equipment orders, especially IBAD, appear.

- Whether short-term borrowings stabilize as working capital is collected.

- Whether CB overhang limits the re-rating.

5. Conclusion

My conclusion is that Green Resource is in a growth-restructuring phase. Near-term trading revenue and borrowings blur the numbers, but broader SD coating adoption in advanced nodes and the fusion-related IBAD option remain the main medium-term re-rating arguments.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224124510119

- Source 2: https://bits-chips.com/article/global-semiconductor-equipment-sales-continue-to-rise/

- Source 3: https://www.semi.org/en/semi-press-release/global-semiconductor-equipment-sales-projected-to-reach-a-record-of-156-billion-dollars-in-2027-semi-reports

- Source 4: https://www.tradingview.com/news/zacks:ed0eb7f75094b:0-will-dram-strength-drive-applied-materials-next-growth-phase/

- Source 5: https://www.businesswire.com/news/home/20250926273024/en/Global-Nuclear-Fusion-Energy-Market-Report-2026-Highlights-Commercialization-Path-to-2046---ResearchAndMarkets.com

- Source 6: https://kind.krx.co.kr/external/2024/03/08/000322/20240308000851/00591.htm

- Source 7: https://sisa-news.com/mobile/article.html?no=247270

- Source 8: https://mobile.newsis.com/view/NISX20241008_0002912853

- Source 9: https://comp.fnguide.com/SVO2/ASP/SVD_Main.asp?gicode=A402490

- Source 10: https://www.investing.com/equities/green-resource