DEEP RESEARCH · Battery Supply Chain

U.S. battery strategy reset: Ford cancellations and the narrow opening for Chinese technology

Reading the Korea-U.S. battery alliance recalibration through OBBBA, CATL licensing, and LMR

0. Bottom line first

My conclusion is that the United States has not opened the main gate to Chinese batteries. It is blocking Chinese capital and control while leaving a narrow exception for already contracted LFP technology licensing.

Official fact: The source describes Ford's cancelled Turkey JV with LG Energy Solution as a roughly KRW 9.6tn, USD 6.5bn contract cancellation. It treats the BlueOval SK restructuring with SK On in the same cost and technology-reset context.

Interpretation: This is less about excluding Korean battery companies and more about U.S. automakers moving from expensive NCM dependence toward technological agnosticism across LFP, LMR, and ESS.

Chasm

The EV slowdown from late 2024 into 2025 exposed price sensitivity.

OBBBA

The July 4, 2025 law changed subsidies and China-related restrictions.

LMR

Korea's counter-card between NCM and LFP on cost and performance.

1. Why Ford stepped away

The Ford-Korean battery alliance originally relied on high-nickel NCM's energy density and long driving range. But mainstream consumers wanted price parity with internal-combustion vehicles more than maximum range, and expensive NCM was difficult for Ford's E-Transit and affordable EV strategy.

Official fact: NCM is exposed to nickel and cobalt price volatility and has high manufacturing cost. LFP has lower energy density, but is cheaper and has stronger fire safety.

Interpretation: The stated reason of demand reassessment reads like an admission that NCM is too expensive for mass-market models.

In the BlueOval SK restructuring, the source says Ford takes over and independently operates the Kentucky plant, while SK On independently operates the Tennessee plant. Ford is seeking flexibility to repurpose plants, move into ESS, or license LFP technology rather than remain locked into an exclusive battery-manufacturer alliance.

2. OBBBA's paradox: closed gate, narrow opening

Official fact: The source says OBBBA repealed IRA Section 30D, the new-EV purchase tax credit of up to USD 7,500, effective September 30, 2025.

Interpretation: If the consumer subsidy disappears, automakers have less reason to use expensive non-Chinese batteries merely to satisfy FEOC rules. The source presents GM's August 2025 plan to import CATL LFP batteries for the next Bolt EV as an example of this regulatory gap.

Official fact: Section 45X production tax credits remain or are strengthened, and OBBBA upgrades FEOC to PFE. Chinese government ownership of 25% or more, board control, or contractual effective control can disqualify subsidies.

The Ford-CATL Marshall, Michigan project survives because OBBBA includes a grandfather clause for technology license agreements signed before July 4, 2025. Ford can keep 100% plant ownership while using CATL technology.

3. Politics: transactional isolationism and a hard-line Congress

The source frames Trump 2.0 as transactional isolationism. It can maintain or raise 100% EV tariffs and 25% battery tariffs while taking a practical view if a project builds factories and hires workers in the United States. But implementation still blocks Chinese ownership and control.

| Actor | Source position | Meaning |

|---|---|---|

| White House | Made in USA first | Chinese technology may be tolerated through licensing if U.S. jobs and plants are present |

| Marco Rubio | Criticized Ford-CATL | Security-driven China battery restrictions could intensify |

| House hard-liners | Led H.R.1166 | Pushes DHS purchase bans on CATL and Gotion batteries |

| Treasury | Must finalize guidance by end-2025 | Royalty and volume-control terms decide effective-control risk |

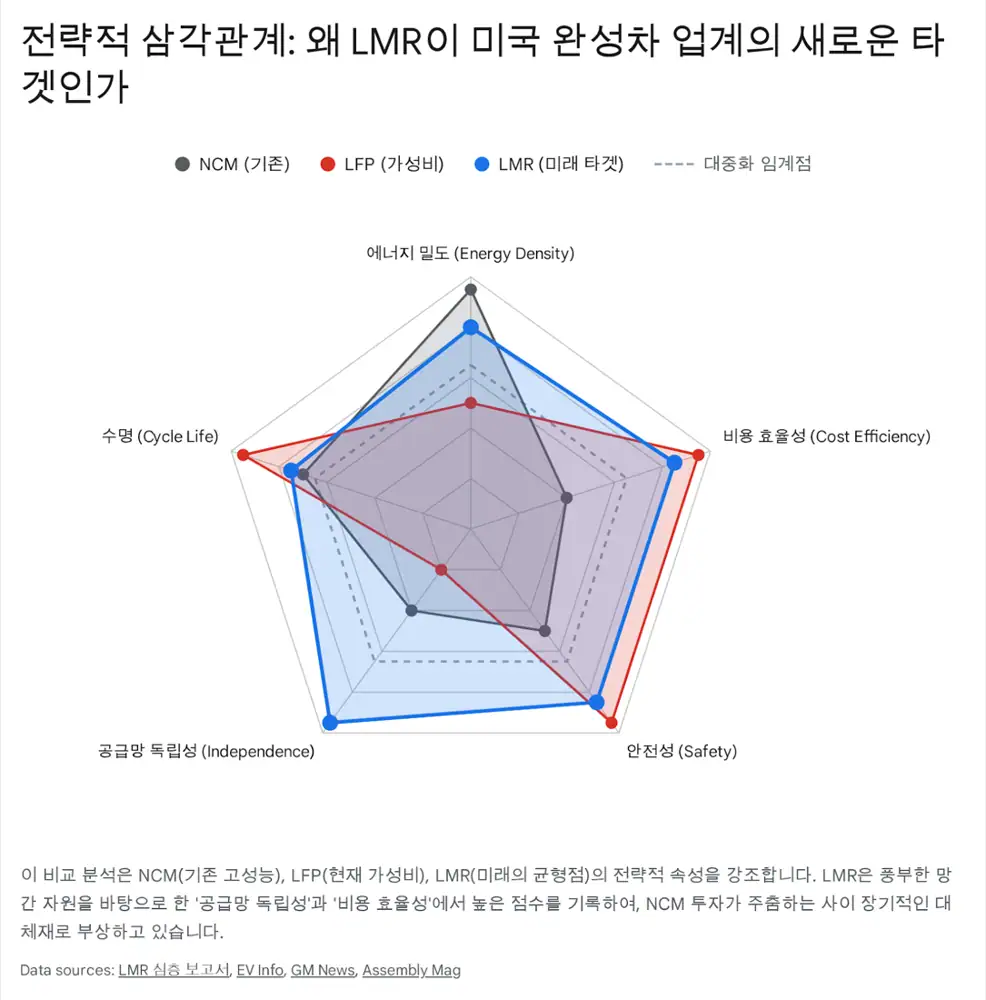

4. LMR and limited Chinese entry

LMR batteries reduce expensive cobalt and nickel while lifting manganese to 60-70%. The source says LMR targets roughly 33% higher energy density than LFP while lowering manufacturing cost versus NCM enough to compete with LFP.

Official fact: The source says GM and LG Energy Solution are developing LMR batteries with a 2028 commercialization target.

Interpretation: Ford's NCM cancellation may reflect a decision to skip expensive NCM capacity now and move later toward LMR or other next-generation low-cost chemistries.

| Case | Detail | Implication |

|---|---|---|

| Gotion Michigan | USD 2.4bn cathode/anode project effectively collapsed after local resistance, political attacks, and subsidy clawback | Large Chinese greenfield investments face strong rejection |

| Gotion Illinois | Manteno battery-pack plant reuses a closed Kmart distribution center, targeting 2025 production | Existing-facility projects with job-creation logic can be tolerated selectively |

5. Korean battery company response

LG Energy Solution is described as responding to the Ford volume cancellation by expanding Mercedes-Benz supply, accelerating cylindrical 46-series cells for customers such as Tesla, developing LFP, and strengthening ESS. ESS is linked to rising AI data-center power demand.

SK On gains more freedom after the BlueOval SK restructuring to diversify beyond Ford toward Hyundai, Kia, and other automakers. The Korean strategy is not to fight Chinese LFP purely on price, but to shift the field with LMR, high-voltage mid-nickel, solid-state, and other technologies balancing cost and performance.

6. Investor checkpoints

- Watch how the U.S. Treasury finalizes PFE and effective-control guidance at the end of 2025.

- The key question is whether CATL technology licensing expands to new contracts or remains limited to grandfathered exceptions like Ford.

- Track LGES and GM's 2028 LMR commercialization roadmap, and the pace of Korean 46-series and ESS revenue conversion.

- The current situation is better understood as a cold recalibration for cost efficiency, not the collapse of the Korea-U.S. battery alliance.

Sources

- Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224124375543

- Ford Cancels Multi-Billion-Dollar Battery Contract with LGES: https://battery-news.de/en/2025/12/23/ford-cancels-multi-billion-dollar-battery-contract-with-lges/

- LG Energy's $6.5 bn EV battery supply deal with Ford terminated - KED Global: https://www.kedglobal.com/batteries/newsView/ked202512170012

- SK On pivots to stationary energy storage after Ford joint venture ends | Utility Dive: https://www.utilitydive.com/news/ford-skon-dissolving-blueoval-sk-ev-battery-joint-venture/808012/

- Marshall breathes sigh of relief as Ford battery plant spared from Trump EV cuts - Bridge Michigan: https://bridgemi.com/business-watch/marshall-breathes-sigh-relief-ford-battery-plant-spared-trump-ev-cuts/

- Ford Taps Michigan for New LFP Battery Plant: https://www.fromtheroad.ford.com/us/en/articles/2023/ford-taps-michigan-for-new-lfp-battery-plant--new-battery-chemis

- From IRA to OBBBA: A New Era for Clean Energy Tax Credits | Advisories | Arnold & Porter: https://www.arnoldporter.com/en/perspectives/advisories/2025/07/from-ira-to-obbba-a-new-era-for-clean-energy-tax-credits

- Unpacking the FEOC Provisions in HR 1, the One Big Beautiful Bill Act: https://bipartisanpolicy.org/explainer/unpacking-the-feoc-provisions-in-the-one-big-beautiful-bill-act/

- Is Ford's pullback from LG Energy a warning shot for Korean battery makers?: https://koreajoongangdaily.joins.com/news/2025-12-18/business/industry/Is-Fords-pullback-from-LG-Energy-a-warning-shot-for-Korean-battery-makers/2481156

- LG Energy Solution to sell Ohio battery plant building to Honda for $2.85bn - Just Auto: https://www.just-auto.com/news/lges-ohio-battery-plant-building/

- Ford's EV Reset Leaves A Multibillion-Dollar Hole In The Battery Industry - InsideEVs: https://insideevs.com/news/782099/ford-ev-reset-multibillion-dollar-hole-battery-industry/

- Ford, SK On plan to end BlueOval SK joint venture; SK On will operate Tennessee battery plant | News From The States: https://www.newsfromthestates.com/article/ford-sk-plan-end-blueoval-sk-joint-venture-sk-will-operate-tennessee-battery-plant

- Ford Follows Customers to Drive Profitable Growth; Reinvests in Trucks, Hybrids, Affordable EVs, Battery Storage; Takes EV-Related Charges: https://www.fromtheroad.ford.com/us/en/articles/2025/ford-reinvests-trucks-hybrids-affordable-electric-vehicles

- What the Ford-SK On Split Means for the Battery Supply Chain: https://www.batterytechonline.com/battery-manufacturing/what-the-ford-sk-on-split-means-for-the-battery-supply-chain

- Big Beautiful Bill changes: EV tax credits, car loan interest, and bonus depreciation: https://www.hrblock.com/tax-center/irs/tax-law-and-policy/one-big-beautiful-bill-vehicle-tax-credits/

- FAQs for modification of sections 25C, 25D, 25E, 30C, 30D, 45L, 45W, AND 179D under Public Law 119-21, 139 Stat. 72 (July 4, 2025), commonly known as the One, Big, Beautiful Bill (OBBB) | Internal Revenue Service: https://www.irs.gov/newsroom/faqs-for-modification-of-sections-25c-25d-25e-30c-30d-45l-45w-and-179d-under-public-law-119-21-139-stat-72-july-4-2025-commonly-known-as-the-one-big-beautiful-bill-obbb

- GM to Source CATL Batteries, Revive Second-Generation Bolt EV | ChinaEVHome: https://chinaevhome.com/2025/08/08/gm-to-source-catl-batteries-revive-second-generation-bolt-ev/

- GM to import EV batteries from China's CATL, source says | HOT 96: https://hot96.com/2025/08/07/gm-to-import-ev-batteries-from-chinas-catl-source-says/

- Understanding the New Prohibited Foreign Entity Rules for Clean Energy Tax Credits | HUB: https://www.klgates.com/Understanding-the-New-Prohibited-Foreign-Entity-Rules-for-Clean-Energy-Tax-Credits-9-18-2025

- The “One Big Beautiful Bill” Act – Navigating the New Energy Landscape - Sidley Austin LLP: https://www.sidley.com/en/insights/newsupdates/2025/07/the-one-big-beautiful-bill-act-navigating-the-new-energy-landscape

- The One Big Beautiful Bill Act that redefines the US clean energy initiatives - CRU Group: https://www.crugroup.com/en/communities/thought-leadership/2025/the-one-big-beautiful-bill-act-that-redefines-the-us-clean-energy-initiatives/

- [Insight] Battery Industry Changes Triggered by the One Big Beautiful Bill Act (OBBBA): https://www.rebiogroup.com/post/insight-battery-industry-changes-triggered-by-the-one-big-beautiful-bill-act-obbba

- Breaking Down the US-China Trade Tariffs: What's in Effect Now?: https://www.china-briefing.com/news/us-china-tariff-rates-2025/

- Biden finalizes China tariff hikes, including for EVs, batteries and solar panels | Utility Dive: https://www.utilitydive.com/news/joe-biden-china-tariff-hikes-ev-battery-semiconductor-final/727014/

- CATL open to US expansion if Trump approves - Teslarati: https://www.teslarati.com/catl-us-expansion-trump-china-approval/

- Republicans slam Ford's battery bet, oppose tax credits - POLITICO Pro: https://subscriber.politicopro.com/article/eenews/2023/02/14/republicans-slam-fords-battery-bet-oppose-tax-credits-00082759

- Washington Likely Reason For Ford's Pause On CATL EV Battery Factory: https://prosperousamerica.org/washington-likely-reason-for-fords-pause-on-catl-ev-battery-factory/

- Committee Legislation to Combat the CCP's Malign Influence, Supply Chain Dominance Sent to the Senate: https://homeland.house.gov/2025/03/10/committee-legislation-to-combat-the-ccps-malign-influence-supply-chain-dominance-sent-to-the-senate/

- H.R.1166 - 119th Congress (2025-2026): Decoupling from Foreign Adversarial Battery Dependence Act: https://www.congress.gov/bill/119th-congress/house-bill/1166

- A Comprehensive Guide to Prohibited Foreign Entities for Clean Energy Tax Credits: https://www.reunioninfra.com/insights/comprehensive-guide-to-prohibited-foreign-entities-for-clean-energy-tax-credits

- LMR 배터리 산업 현황 및 전망: https://drive.google.com/open?id=1m-gwKvMWFv6dcc3a4xCGBGFVmH3_2MAAU4JkChAAVTA

- Ford Makes Breakthrough With Lithium Manganese Rich (LMR) Battery Chemistry: https://evinfo.net/2025/04/ford-makes-breakthrough-with-lithium-manganese-rich-lmr-battery-chemistry/

- GM and LG to Develop LMR Battery Technology - Assembly Magazine: https://www.assemblymag.com/articles/99279-gm-and-lg-to-develop-lmr-battery-technology

- GM and LG Energy Solution to pioneer LMR battery cell technology - GM News: https://news.gm.com/home.detail.html/Pages/news/us/en/2025/may/0513-GM-LG-Energy-Solution-pioneer-LMR-battery-cell-technology.html

- Michigan: Gotion battery plant plan is dead after years of controversy: https://bridgemi.com/business-watch/michigan-gotion-battery-plant-plan-is-dead-after-years-of-controversy/

- State scraps controversial EV battery plant near Big Rapids | WCMU Public Radio: https://radio.wcmu.org/local-regional-news/2025-10-24/state-scraps-controversial-ev-battery-plant-near-big-rapids

- Gotion EV Battery Plant FAQ & Video - Economic Alliance of Kankakee County: https://kankakeecountyed.org/about-us/news-and-updates/gotion-ev-battery-plant-faq-video/

- Where mega battery, EV projects stand after $1 billion in Michigan subsidies: https://bridgemi.com/business-watch/where-mega-battery-ev-projects-stand-after-1-billion-michigan-subsidies/

- LG Energy Solution ends $3.9bn FBPS deal, shifts focus to ESS and profitability - Chosunbiz: https://biz.chosun.com/en/en-industry/2025/12/26/UE2JEYL4VNELLIZCR3SW4Z32YQ/

- LG Energy scraps $2.8 bn US contract in 2nd supply cancellation in December - KED Global: https://www.kedglobal.com/batteries/newsView/ked202512260005