DEEP RESEARCH · NOTA

Nota: Optimization Infrastructure for the On-Device AI Era

A company analysis across NetsPresso, hardware-aware optimization, and the software bridge for Korean NPUs

0. Bottom line first

Nota should be viewed as an AI optimization platform company, not simply an AI model developer. As AI shifts from cloud training toward edge inference and on-device execution, NetsPresso becomes more valuable if it can solve hardware constraints through software.

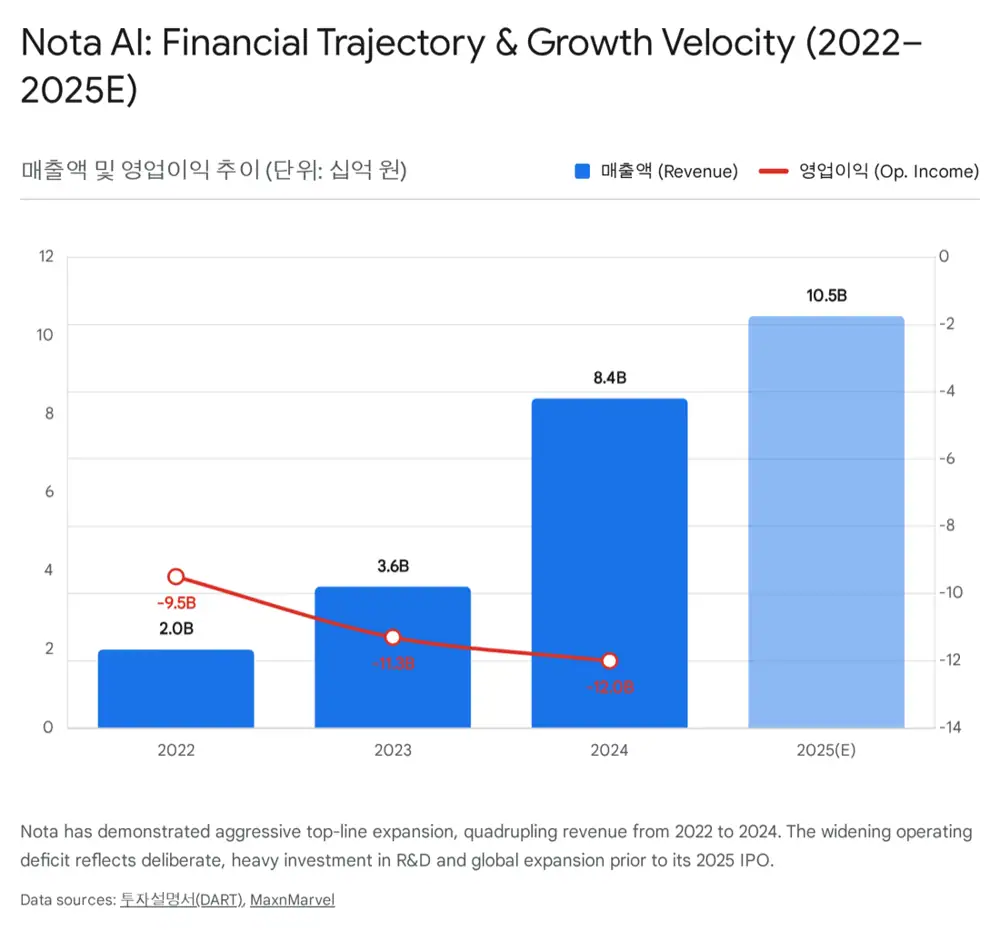

Official fact: The source says Nota began as a KAIST campus venture and that its core product is NetsPresso, a hardware-aware AI optimization platform. Revenue rose from about KRW 2bn in 2022 to KRW 8.4bn in 2024, more than 4x growth, and the company secured about KRW 26.5bn in IPO proceeds through its November 2025 KOSDAQ listing.

Interpretation: My main question is not near-term overhang but whether Nota can become a real standard software layer between Korean NPUs and global edge hardware.

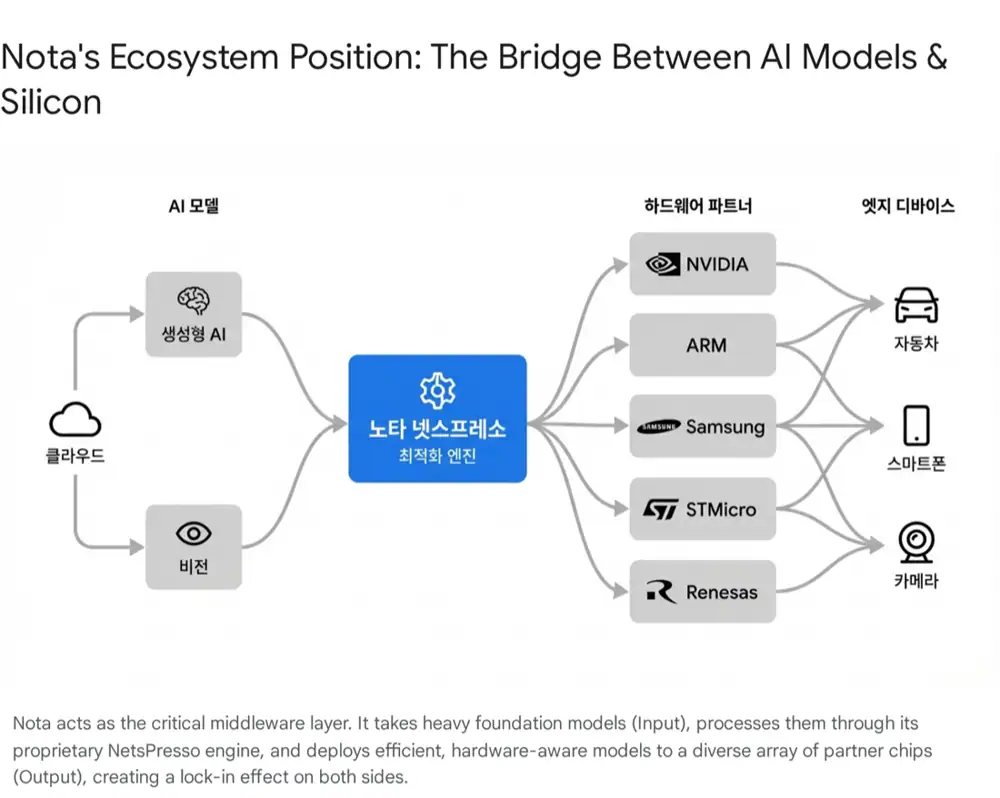

1. Business model: what NetsPresso sells

Nota is about optimization technology that makes AI models run on target hardware. As models grow larger, edge devices, MCUs, NPUs, and mobile APs face memory, power, and latency constraints. NetsPresso targets that bottleneck.

B2B SaaS / On-Premise

Enterprise customers use NetsPresso to optimize their own AI models for target hardware.

Optimization projects

Nota performs NPU-specific and vision-AI porting projects for semiconductor makers and large OEMs.

Packaged solutions

It supplies software solutions using optimized models for ITS and driver monitoring systems.

2. Financials and cash flow: the J-curve phase

| Item | Source figure or detail | Meaning |

|---|---|---|

| Revenue | About KRW 2bn in 2022 → KRW 8.4bn in 2024 | More than 4x growth |

| Operating loss | About KRW 12bn in 2024 | R&D and global talent burden |

| Workforce | Engineers are more than 70% of total headcount | High-wage technical workforce |

| IPO proceeds | About KRW 26.5bn in November 2025 | Capital to ease impairment issues and deepen technology |

Official fact: The source says operating cash flow has remained negative over the latest three years and through 2025 Q3. Financing cash flow was positive through Series B/C investments, RCPS issuance, and IPO proceeds.

Interpretation: This is not a factory-heavy CAPEX story, but high-performance servers, test equipment, capitalized development, and global office buildout still make the path to breakeven a central checkpoint.

3. Partnerships and moat

Nota’s customers and partners span the global semiconductor ecosystem. The source lists partnerships with around 17 global semiconductor makers including NVIDIA, ARM, Qualcomm, Renesas, STMicroelectronics, and NXP. Domestic partners include Samsung Electronics System LSI and Exynos optimization cooperation, LG CNS, and Kakao Enterprise. In public infrastructure, Saudi Arabia and broader Middle East ITS projects are cited.

- Technical moat: Nota optimizes model structure and inference speed for the target device architecture, not only parameter count.

- Relationship moat: Official partner status with chip vendors such as ARM and NVIDIA can create a loop in which chip vendors recommend Nota to OEM customers.

- Experience moat: Optimization data and field problem-solving experience across mobility, security, smart cities, and heterogeneous hardware are difficult for followers to copy quickly.

4. History, leadership, and investors

Nota was founded in 2015 as a KAIST campus venture. Its first item was a soft-keyboard app that reduced typos. While trying to run typo-correction deep-learning models on low-performance smartphones, the team realized the optimization technology was more valuable than the app and pivoted into B2B AI optimization.

| Timing | Event | Meaning |

|---|---|---|

| 2015~2016 | Naver D2SF first portfolio company, Bluepoint Partners | Seed-stage technical validation |

| 2019.08 | Pre-A KRW 1.5bn, Stonebridge Ventures | Early growth funding |

| 2020.08 | Series A KRW 8bn, LB, Stonebridge, Samsung Venture Investment | Strategic cooperation with Samsung ecosystem begins |

| 2021.11 | Series B KRW 17.5bn | NetsPresso platform development |

| 2024.07 | Series C KRW 27.2bn | Largest pre-IPO round |

| 2025.11.03 | KOSDAQ listing | Public-market growth capital |

CEO Chae Myung-soo is described as a KAIST-trained founder who emphasizes customer problems. CTO Kim Tae-ho is the key architect of NetsPresso, and CFO Hyung Nam-baek is presented as leading IPO execution and financial stability.

5. Competition and differentiation

The competitive set includes Deci AI, OmniML, Hugging Face, SqueezeBits, and Clika. Deci AI and OmniML were acquired by NVIDIA. Hugging Face offers Optimum. SqueezeBits is strong in quantization, while Clika targets edge devices through automated lightweighting solutions.

Broad hardware support

The source highlights support from Renesas and STMicro MCUs to high-performance server-class NPUs.

SaaS automation

NetsPresso turns optimization into a scalable platform rather than a consulting-only model.

LLM and multimodal support

Nota has expanded from vision into on-device LLM and generative-AI optimization.

6. Growth strategy and risks

Official fact: The source says Nota invested funds raised over the last eight quarters into offices in San Jose and Germany, local engineering hires, and high-performance computing infrastructure for generative-AI optimization.

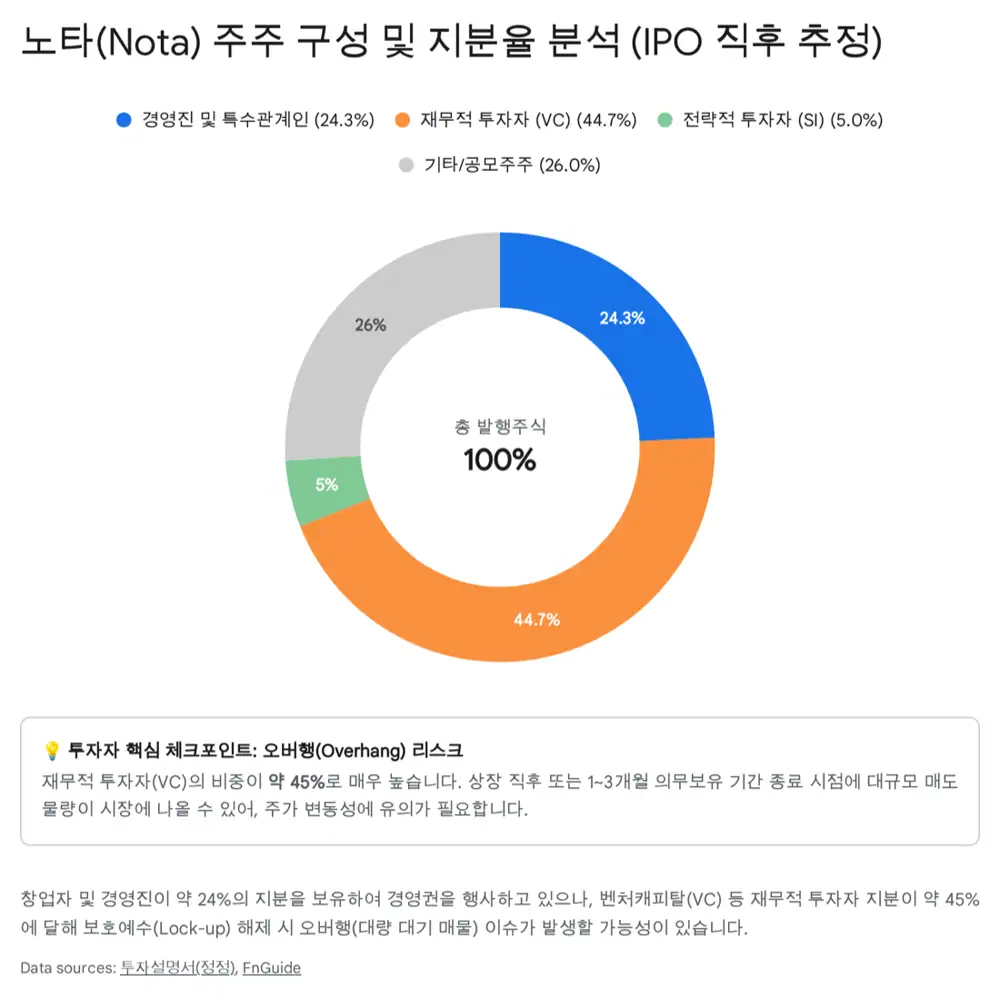

- Overhang: Venture capital investors hold about 45% of total shares, and lock-up expirations at one, three, and six months may create selling pressure.

- CB risk: No large disclosed outstanding CB balance is identified, but future mezzanine issuance for M&A or operating capital cannot be ruled out.

- Commoditization: If big tech releases strong lightweighting tools for free, demand for paid solutions may weaken.

7. Policy tailwind and my conclusion

The source views Korea’s AI Semiconductor Industry Leap Strategy and K-Cloud project as tailwinds. The policy core is to apply domestic AI semiconductors, including NPU and PIM, to data centers and edge devices by 2030 and reduce dependence on NVIDIA.

Interpretation: Korean NPU fabless companies such as Rebellions, Sapeon, and FuriosaAI may have strong hardware but weaker software stacks compared with CUDA. The source’s central thesis is that Nota can act as the software bridge that lets AI models run smoothly on those domestic NPUs.

Ultimately, Nota sells the optimization layer that remains necessary even when AI models or semiconductor chips change. The key indicators are recurring NetsPresso revenue, chip-vendor recommendation loops, and adoption in domestic NPU projects.

Sources

- Naver Blog source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224124350566

- Toss Securities disclosure link: https://www.tossinvest.com/stocks/A150900/news?menu=disclosure&symbol-or-stock-code=A150900&contentType=disclosure&contentParams=%7B%22id%22%3A%22DART%3AA%3A150900-20251113000644%22%2C%22companyCode%22%3A%22150900%22%2C%22reportItem%22%3A%224.2.0%22%7D

- FnGuide Nota share analysis: https://wcomp.fnguide.com/CompanyInfo/ShareAnalysis?cmp_cd=486990

- Yonhap Infomax Stonebridge Ventures article: https://news.einfomax.co.kr/news/articleView.html?idxno=4388116

- AI semiconductor industry leap strategy: https://epts.kdi.re.kr/share?cte_seq=81887&dvs=them

- Yonhap fabless expansion article: https://www.yna.co.kr/view/AKR20251210098851003