DEEP RESEARCH · DK-LOK (105740.KQ)

DK-LOK Deep Dive: At the Center of Korea's Manufacturing Renaissance & Value-Chain Revolution

Re-framing DK-LOK from a legacy fittings vendor into an "extreme-environment fluid-control solutions partner" for aerospace, defense, semiconductor, and robotics

0. Bottom line first

DK-LOK sits in a "Perception Gap" zone. The market still prices it like an oil-price-driven legacy fittings name, but the actual fundamentals have already evolved into a core component supplier for aerospace, defense, and semiconductor — backed by NADCAP certification + KF-21 production references + Samsung UHP entry. The 3Q 2025 74% export ratio and earnings turnaround are just the opening signal. Fundamentals justify re-rating from industrial-goods (P/E 8–10x) into defense/aerospace-component multiples (P/E 15–20x).

Official fact: 3Q 2025 exports / domestic = 74% / 26%. Distributor network in 47 countries (100+ dealers), 300+ tier-1 customers (Exxon Mobil, Dow, HD Hyundai Heavy, Gazprom, etc.). First Korean fittings maker to receive NADCAP certification (Aug 2022). Localized and supplied 18 hydraulic / fuel-line fittings for the KF-21 prototype. Roadmap: aero+defense to reach 15% of revenue (KRW 20B+) by 2030.

Interpretation: Developed-market OPM 15–20% vs. domestic -10%~+5% — just shifting mix to exports structurally upgrades earnings quality. Stack aerospace ASPs (tens of times higher) and semi UHP ASPs (multiples higher) on top, and Q · P · C all move favorably at once.

1. Hardware renaissance and DK-LOK's strategic value

1.1 A paradigm shift in global industry

As of 2025, the efficiency-first globalization era is giving way to economic block-formation and re-industrialization centered on security and supply-chain stability. America's "Genesis Mission" energy-and-manufacturing resurgence, geopolitical risk from the Russia–Ukraine war and Middle East conflict, and the Physical AI revolution that extends AI into the physical world together demand a fundamental restructuring of manufacturing.

The result is a hardware renaissance. CAPEX in data centers, semiconductor fabs, defense procurement, and energy infrastructure has become more important than ever — and the resulting structural demand for piping, fluid control, and precision components is moving from cyclic recovery to a super-cycle.

1.2 DK-LOK's repositioning

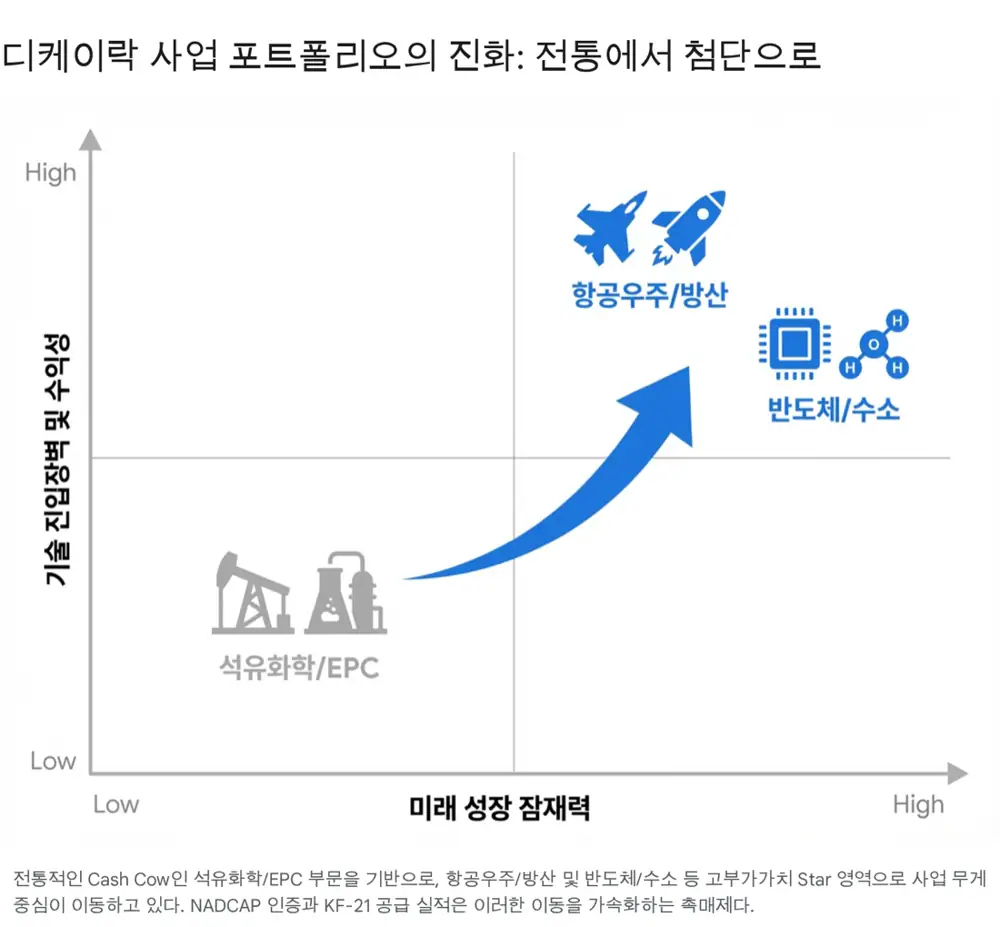

Founded in 1986, DK-LOK was historically viewed as an industrial-goods company tethered to oil-and-gas / petrochemical plant cycles. But several years of R&D and certification have expanded the portfolio into aerospace, defense, semiconductor, and robotics. We re-frame DK-LOK as an "extreme-environment fluid-control solutions partner."

2. Core competitiveness — breaking a global oligopoly with technology

Instrumentation fittings & valves are not generic piping materials. They connect micro-tubing carrying hydrogen, toxic gases, and ultra-high-pressure fluids; a single leak can mean a plant explosion, casualties, or contamination of a semiconductor line worth hundreds of billions of KRW. The market has long been dominated by a handful of global majors — Swagelok, Parker — and DK-LOK punched through that wall on pure technology.

2.1 Technological moat — Intermix & Interchangeability

- Difficulty: Tightening the nut compresses a ferrule, which plastically deforms the tube to seal. Tolerances down to 1/1000 inch matter; any deviation leaks under pressure.

- Certification value: DK-LOK is certified by TUV Rheinland for full Intermix performance with Swagelok components — an extremely rare credential globally. This lets end users keep installed Swagelok systems while substituting DK-LOK parts → a "Lock-in Release" lever.

- Materials tech: Proprietary corrosion-resistant ferrule prevents intergranular corrosion in offshore plants and semi lines — extending product life. Vertical integration extends from heat treatment to surface treatment.

2.2 Global network and geographic risk dispersion

74% (3Q 2025)

Distributors in 47 countries (100+), 300+ tier-1 customers — decoupled from Korean domestic cycle.

15–20%

US/Europe segment OPM; North America energy infra + European supply-chain reshuffle drive higher mix.

-10% to +5%

Hyper-competitive domestic market. Export mix lift = structural margin upgrade.

2.3 Production efficiency — smart factory + robot automation

DK-LOK runs an MES system and robotic machining lines at its Gimhae HQ plant. Unmanned night/weekend operation absorbs fixed-cost pressure and, once revenue clears breakeven, maximizes operating leverage.

3. Aerospace & defense — the core re-rating engine

3.1 NADCAP certification — a "fast pass" into global aerospace

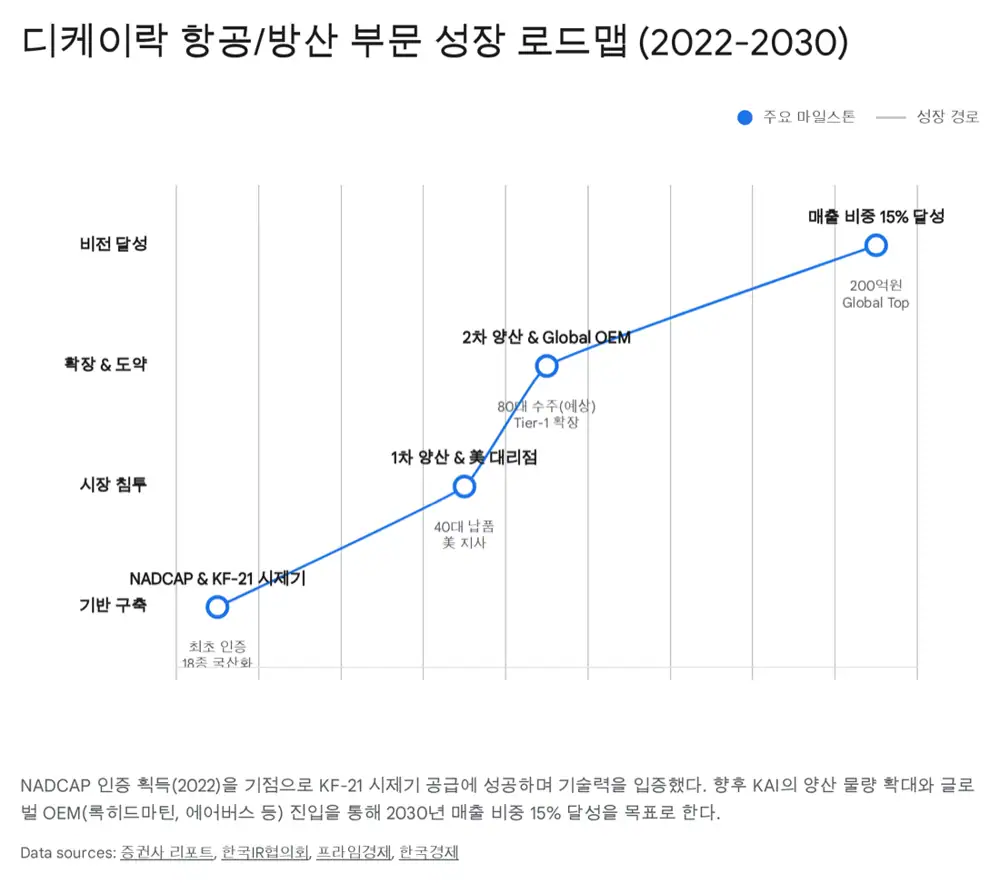

Official fact: In August 2022 DK-LOK became the first Korean fittings maker to receive NADCAP (National Aerospace and Defense Contractors Accreditation Program) from the US PRI (Performance Review Institute).

Interpretation: NADCAP is a mandatory special-process accreditation required by Boeing, Airbus, Lockheed Martin and other primes when selecting suppliers. It validates not dimensions but heat treatment, welding, NDT, and the entire manufacturing flow against aerospace standards. The credential allows direct supply into global OEM chains — the catalyst for export expansion.

3.2 KF-21 Boramae and the K-defense trickle-down

- KF-21 supply track record: As a key KAI partner, DK-LOK localized and supplied 18 component types in the hydraulic and fuel systems of the KF-21 prototype — a "Flight Proven" reference.

- Mass-production outlook: Following the initial production contract in 2024, a 2nd batch (80 units) in early 2026 is highly likely. Once KF-21 mass production ramps, aerospace revenue inflects upward.

- FA-50 export expansion: Likely application to FA-50 units exported to Poland, Malaysia, etc. KAI's export backlog directly translates into DK-LOK's revenue potential.

3.3 Expansion into ground and naval weapon systems

DK-LOK has completed quality approval for hydraulic fittings used in Hyundai Rotem's K2 tank and wheeled armored vehicles, and started shipments. Post–Ukraine war global tank demand + K2's Poland export deal form a second pillar of defense revenue.

3.4 Roadmap — 15% revenue mix by 2030

Management has laid out a roadmap to lift aero+defense to 15% of total revenue (KRW 20B+ annually) by 2030. Aerospace fittings carry ASPs tens of times higher than general industrial ones — this mix change structurally lifts company-wide OPM.

4. Semiconductor & robotics — concretizing the new growth engines

4.1 Semiconductor UHP (Ultra High Purity)

- 4th plant in Pyeongtaek secured to expand UHP (electro-polished) fittings/valves capacity.

- Pursuing/executing supply into Samsung Electronics P4 / P5 construction and Hook-up. Strong localization demand in a UHP market previously monopolized by Fujikin (JP), Swagelok / Parker (US).

- KIRI projection: semiconductor mix from ~10% in 2024 to ~15% in 2025 — ~40% CAGR.

4.2 Robotics — a stealth beneficiary of the Physical AI era

- Industrial robots and hydraulic quadruped robots (e.g. Boston Dynamics Spot) require high-pressure fittings in joints/actuators that withstand vibration and shock. DK-LOK owns a patented vibration-resistant anti-loosening technology.

- KRW 7.1B supply contract with Nudraulix — a signal of robotics/automation traction (~6.4% of prior-year revenue).

- Doosan Robotics, Rainbow Robotics, etc. domestic growth → gradually expanding demand for components inside finished robot units.

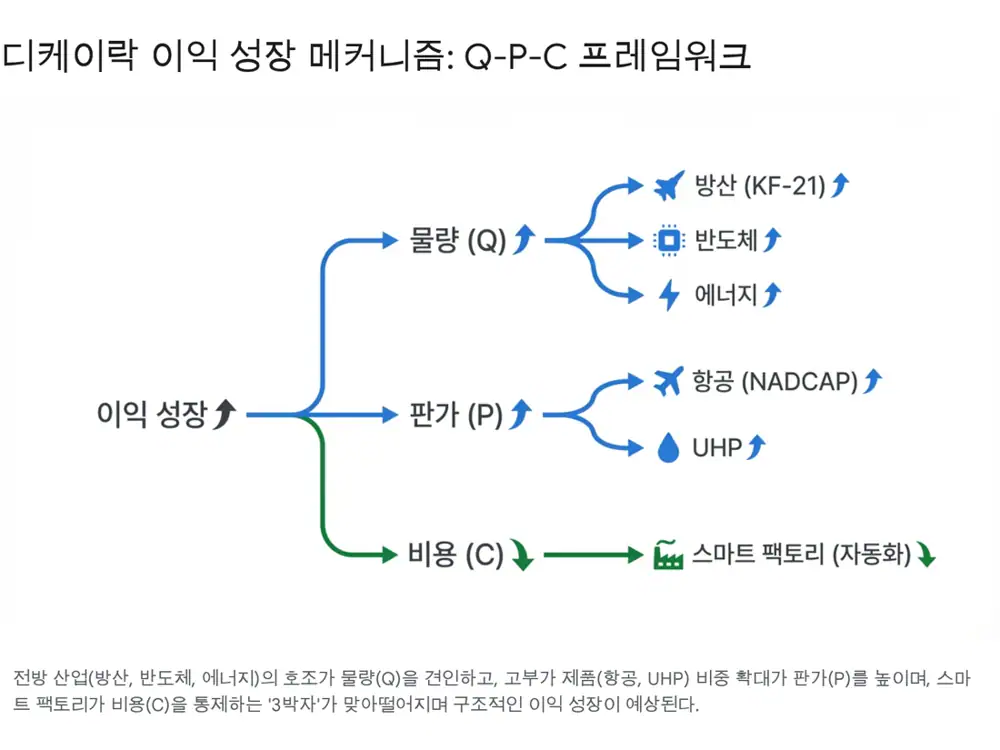

5. Q · P · C framework — earnings impact

5.1 Q — simultaneous booms across end-markets

- K-defense / aero: Post-Ukraine global defense-budget lift. 2025–2026 overlaps FA-50 export deliveries + KF-21 production ramp.

- Energy infrastructure: US "Genesis Mission" + Middle East NEOM stimulate LNG and hydrogen plant orders → solid base demand.

- Semiconductors: AI data-center build-out + HBM & leading-edge node investments → structural UHP demand.

5.2 P — high-value mix shift and FX

Aero fittings command ASPs tens of times higher than general; semi UHP multiples higher. As generic price-competitive volume shrinks and high-end share grows, average ASP rises on mix alone. With ~74% exports, the strong-USD regime lifts KRW-converted P.

5.3 C — fixed-cost dilution and production efficiency

As a fixed-cost-heavy process industry, OP growth massively outpaces revenue growth once revenue clears breakeven. The Gimhae smart factory and robotic automation cap labor expense and lower defect rates; raw-material (stainless, nickel, moly) volatility is countered with pass-through and process efficiency.

6. Risks & checkpoints

- FX volatility: 74% exports cuts both ways. Sharp KRW strength would compress KRW-translated revenue/profit. Partly hedged through natural offset of raw-material imports + derivatives.

- End-market investment delays: Slower semiconductor recovery or oil-price-driven delays to Middle East / US energy projects would increase near-term variability. Notably, Samsung P4/P5 schedule shifts directly affect UHP revenue.

- Raw-material spikes: If stainless steel, nickel, or molybdenum spike and can't be passed through promptly, transient margin squeeze.

7. Conclusion & investment view

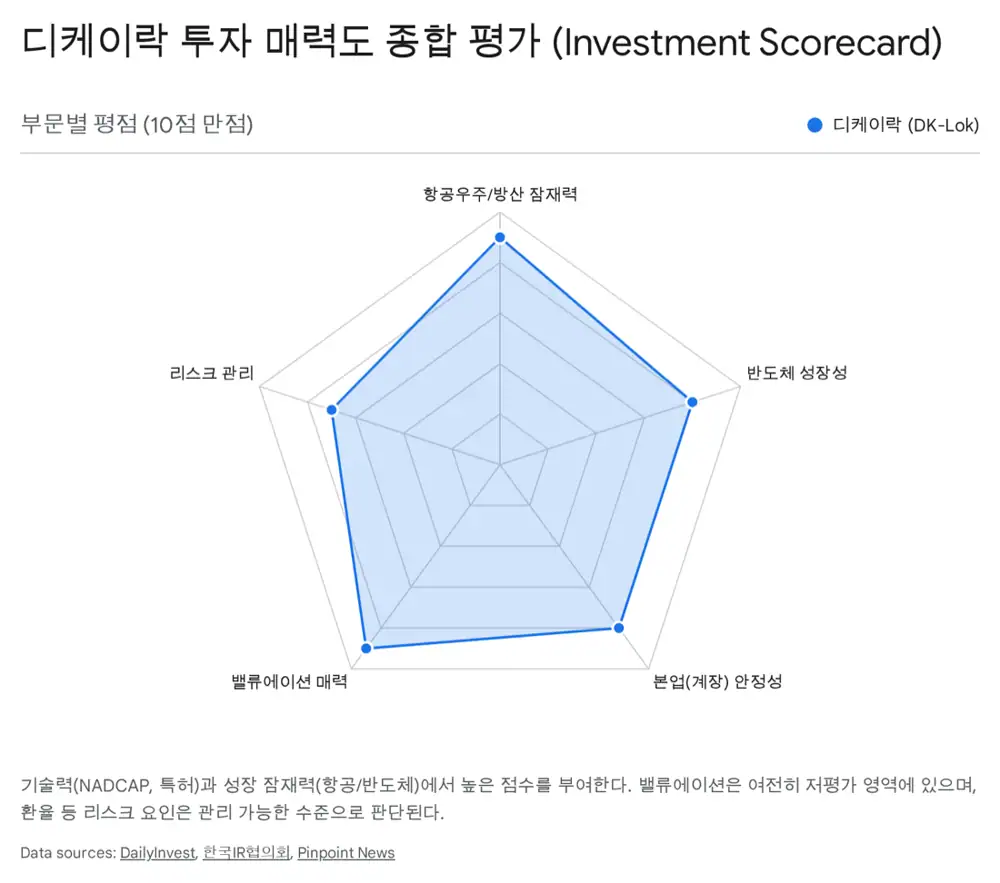

7.1 Opportunity born of the Perception Gap

- Clear growth roadmap: K-defense export rally + AI-semi cycle + NADCAP & KF-21 references = a moat competitors cannot cross overnight.

- Earnings turnaround: Strong 3Q 2025 and rising export mix are not one-offs but a structural recovery. From 2026, KF-21 production + new fab orders should produce a quantum jump.

- Valuation appeal: The current 8–10x P/E does not reflect the new-business value. As aero/defense and semiconductor become visible in the P&L, a 15–20x defense/aerospace component multiple is appropriate.

7.2 Final view

DK-LOK is a "Hidden Champion" aligned with Korea's manufacturing upgrade. Rather than chase short-term volatility, lean into the re-rating from industrial goods to advanced materials/components over the medium-to-long term. Investment view: Strong Buy.

Sources

- Naver blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224124274032

- Korea space-company investment proposal: Google Drive

- DK-LOK: semi customer CAPEX restart — DailyInvest: article

- DK-Lok Tube Fittings PDF: PDF

- DK-LOK supplies 300+ instrument-grade fitting customers — HanKyung: article

- DK-LOK launches aero fittings business reaching KF-21 — PinPoint News: article

- DK-LOK (105740) report — Naver Stock: PDF

- "EPC awakens DK-LOK" — Mobile HanKyung: article

- KF-21 Boramae development schedule — Namu Wiki: wiki

- DK-LOK accelerates aero, semi, marine-plant expansion — Newspim: article

- DK-LOK defense/semi acceleration — Prime Economy: article

- DK-LOK USA — UHP: site

- DK-LOK semi fittings/valves reach Samsung — Prime Economy: article

- DK-LOK Nudraulix KRW 7.1B contract — DailyInvest: article