DEEP RESEARCH · Y-BIOLOGICS

Y-Biologics: Commercializing an Antibody Discovery Platform

A review of Ymax®-ABL, ALiCE, pH-sensitive antibodies, the YBL-034 deal, and 2026 catalysts

0. Bottom line first

Y-Biologics should be viewed not just as an antibody discovery CRO but as an antibody discovery platform company expanding into bispecific antibodies, ADCs, and immunocytokines. The key question is whether the global deal reference shown by YBL-034 can repeat across follow-on platforms.

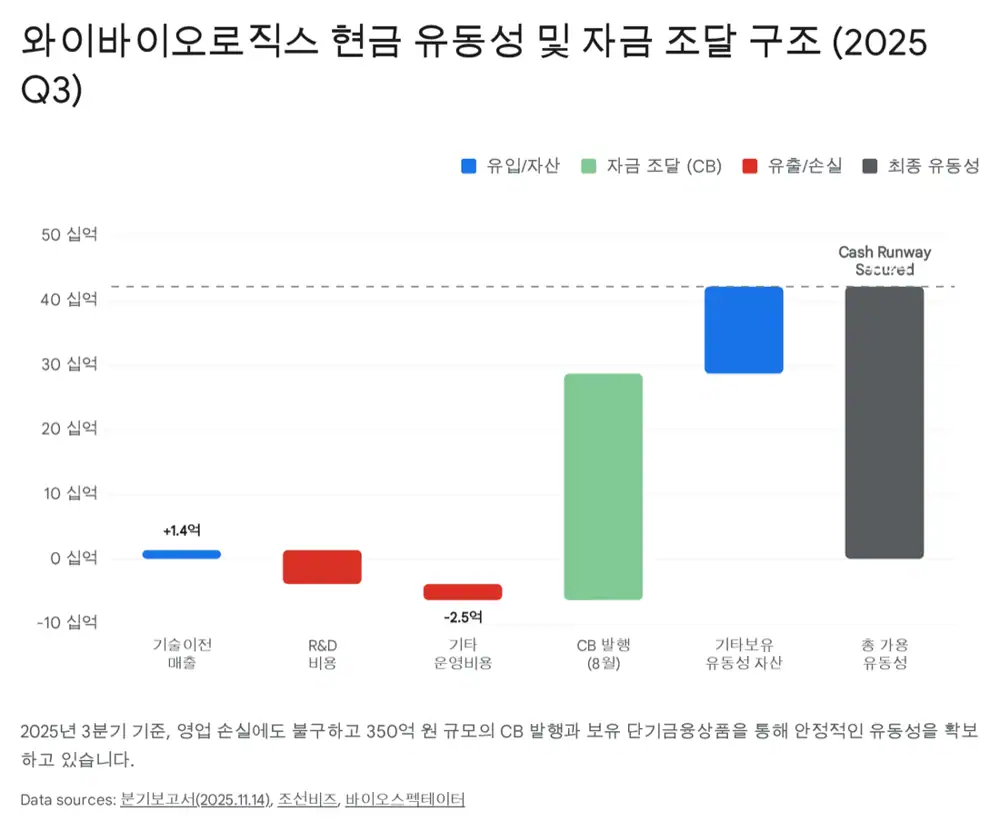

Official fact: The source says Y-Biologics was founded in 2007 and owns Ymax®-ABL, a fully human antibody library with more than 100 billion human antibody gene diversity. It also issued KRW 35bn of convertible bonds in August 2025.

Interpretation: The company’s value depends less on near-term revenue and more on how many collaboration and license-out options its platform can generate.

1. Market background and company position

The global pharma and biotech industry is moving beyond monoclonal antibodies into multi-modality approaches such as bispecific antibodies, ADCs, and immunocytokines. The source cites an antibody therapeutics market outlook of roughly USD 804.3bn around 2030.

Official fact: Keytruda has become the standard of care as the top-selling immune checkpoint inhibitor, but the source notes an efficacy ceiling with overall cancer-patient response rates around 20-30%.

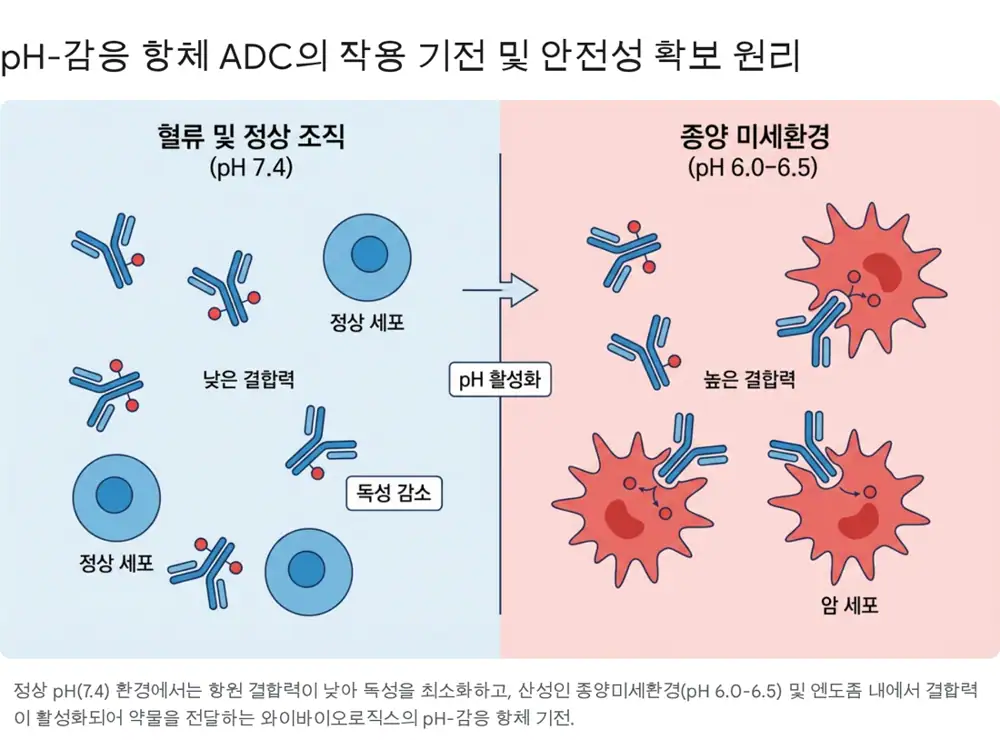

Y-Biologics is framed as a platform company with a fully human antibody library, the ALiCE T-cell bispecific platform, and pH-sensitive antibodies that activate in acidic tumor microenvironments.

2. Platform moat: three technology axes

Naive library

A fully human antibody library based on B-cell-derived cDNA, with low immunogenicity and fast phage-display screening.

2:1 asymmetric structure

Two Fab arms bind cancer antigens strongly, while one Fv arm binds T-cell CD3 at a controlled level to reduce CRS toxicity.

ADC therapeutic-index improvement

The switch mechanism suppresses binding at normal pH 7.4 and increases binding in acidic tumor environments around pH 6.0-6.5.

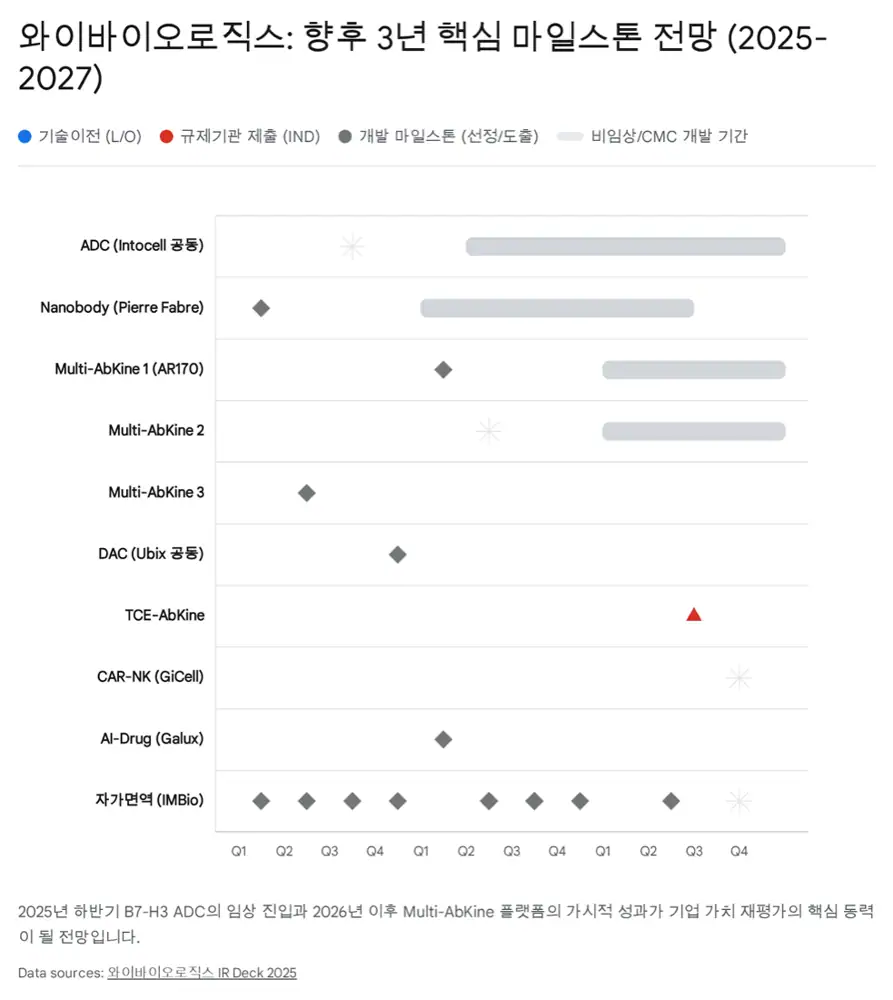

3. Pipelines and deal structure

| Pipeline | Description | Key source fact |

|---|---|---|

| YBL-006 acrixolimab | PD-1 immune checkpoint inhibitor | Global phase 1/2a completed; overall ORR 15.9%, NET ORR 25.0% |

| YBL-034 OXTIMA | OX40L x TNF-alpha bispecific | Licensed to Navigator Medicines for up to USD 940mn including USD 20mn upfront, about KRW 1.3tn |

| AR153 | B7-H3 ADC using IntoCell OPHAS linker | B7-H3 is overexpressed in solid tumors and low in normal tissue; no approved drug yet |

| Multi-AbKine | AR166, AR169, AR170 | Preclinical completion and IND filings expected in 2026-2027 |

Official fact: Existing literature cited in the source shows Keytruda monotherapy ORR of 3.7-12% in neuroendocrine cancer, while the source highlights YBL-006’s NET ORR of 25.0% as a basis for an orphan/fast-track strategy.

Interpretation: YBL-034 is more than a licensing headline. It demonstrates a model in which an antibody discovered by Y-Biologics combines with partner technology, becomes a global deal, and generates profit sharing for the original platform owner.

4. Financial position and CB overhang

The source frames Y-Biologics as a high-growth R&D biotech. Pipeline value and runway matter more than near-term quarterly revenue swings.

| Item | Source figure as of 2025 Q3 | Interpretation |

|---|---|---|

| Cumulative revenue | About KRW 2.46bn | Down from about KRW 5.76bn YoY due to milestone timing |

| Revenue mix | License revenue KRW 1.45bn (59%), contract research KRW 0.95bn (39%) | Mixed license-fee and CRO model |

| Operating loss | About KRW 6.28bn | Continuing R&D investment |

| R&D expense | About KRW 5.24bn | More than 200% of revenue |

| Liquidity | Cash KRW 0.44bn + short-term financial products KRW 41.7bn | The source reads usable liquidity as ample |

| CB | KRW 35bn, 0.0% coupon, 3.0% yield to maturity, conversion price 11,430 won | Conversion period starts August 7, 2026 |

5. Risks and mitigation

- License-out uncertainty: DLK1 ADC YBL-001, co-developed with LigaChem Bio and licensed to Pyxis Oncology, was discontinued and rights were returned.

- Mitigation: The company restarted follow-on development with LigaChem Bio using a changed payload and is diversifying through Multi-AbKine and pH-sensitive ADC programs.

- Financial volatility: Large fixed revenue sources outside license fees remain limited.

- Mitigation: Contract research service expansion can support cash flow and identify future collaboration partners.

6. Catalysts after 2026

The source frames 2026 as the first year in which Multi-AbKine and pH-sensitive ADC technologies can move beyond preclinical work toward clinical entry or larger license-out validation.

B7-H3 ADC licensing

Global pharma L/O discussions may become concrete around AR153 phase 1 entry.

Milestone inflow

Navigator Medicines’ US clinical progress can bring staged milestone income and support financial stability.

Preclinical data

Conference data can validate the platform and accelerate partnering.

7. My conclusion

Y-Biologics combines a validated platform, Ymax®-ABL, a clinical-stage internal asset, YBL-006, and revenue-generating partnership reference, YBL-034. Near-term earnings volatility is high, but concentrated clinical-entry and data catalysts in 2026 could revalue the platform.

Sources

- Naver Blog source: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224124270880

- 글로벌인포메이션 항체 치료제 시장: https://www.giikorea.co.kr/report/vmr1402197-global-antibody-therapeutics-market-research.html

- 조선비즈 - 와이바이오로직스 CB 350억: https://biz.chosun.com/science-chosun/bio/2025/08/07/JHOIQL6HYJAKFD7E4ZKHLAL3IY/

- BQURA - YBIOLOGICS: https://bqura.com/company/104

- Grand View Research - bispecific antibodies: https://www.grandviewresearch.com/industry-analysis/bispecific-antibodies-market-report

- PMC - Bispecific antibodies review: https://pmc.ncbi.nlm.nih.gov/articles/PMC8131538/

- KRX 공시 - 와이바이오로직스 분기보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250514000707&docno=&viewerhost=&

- PMC - KEYNOTE-158 neuroendocrine tumors: https://pmc.ncbi.nlm.nih.gov/articles/PMC7811789/

- Targeted Oncology - immunotherapy combos: https://www.targetedonc.com/view/immunotherapy-based-combos-may-be-necessary-in-neuroendocrine-neoplasms

- Biospectator - 350억 CB 발행: https://www.biospectator.com/news/view/25903