DEEP RESEARCH · COWINTECH

Cowintech: Integrated Solutions for Smart Factories and the Battery Value Chain

An analysis centered on AMR Direct Docking, TopMaterial synergy, and KRW 256.7bn order backlog.

0. Bottom line first

Cowintech's 2025 numbers show growing pains, but KRW 256.7bn of backlog and Direct Docking AMR technology show that medium-term automation demand remains alive. The key is how fast the company can endure the battery chasm while expanding into semiconductor, ESS, and general logistics customers.

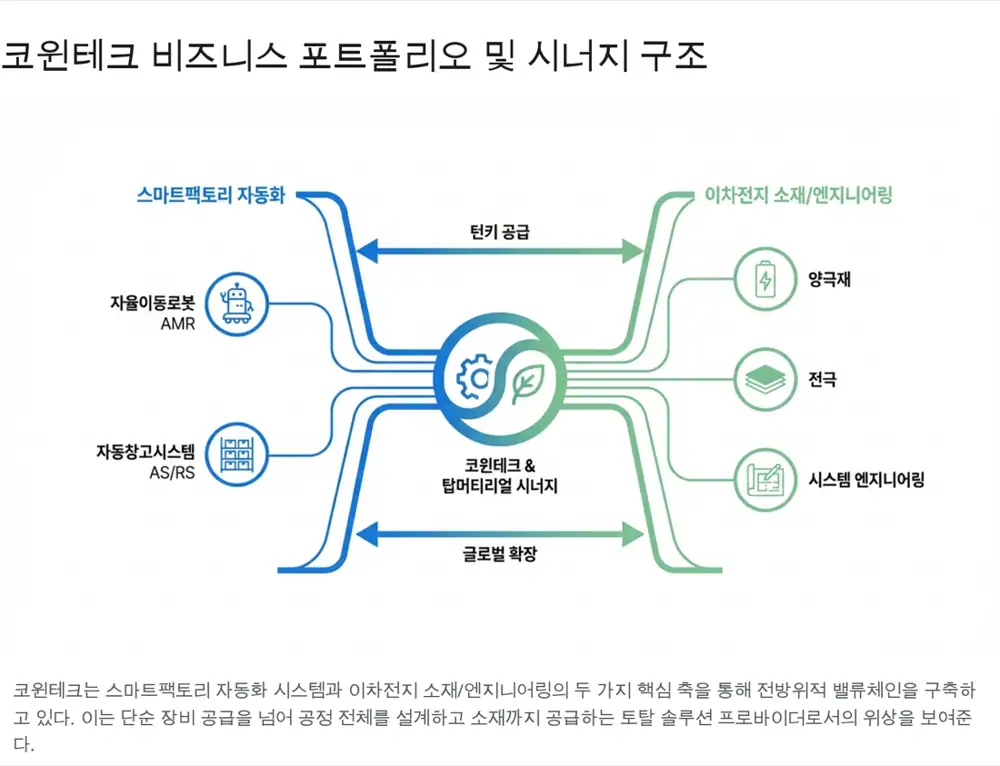

1. Company structure and global bases

Cowintech was founded on October 14, 1998 as an automation-equipment company. It entered battery process automation in 2012, and the source says it built the world's first full-process battery automation system in 2017. After listing on KOSDAQ in 2019, it invested in TopMaterial in 2021 to secure a materials and engineering value chain.

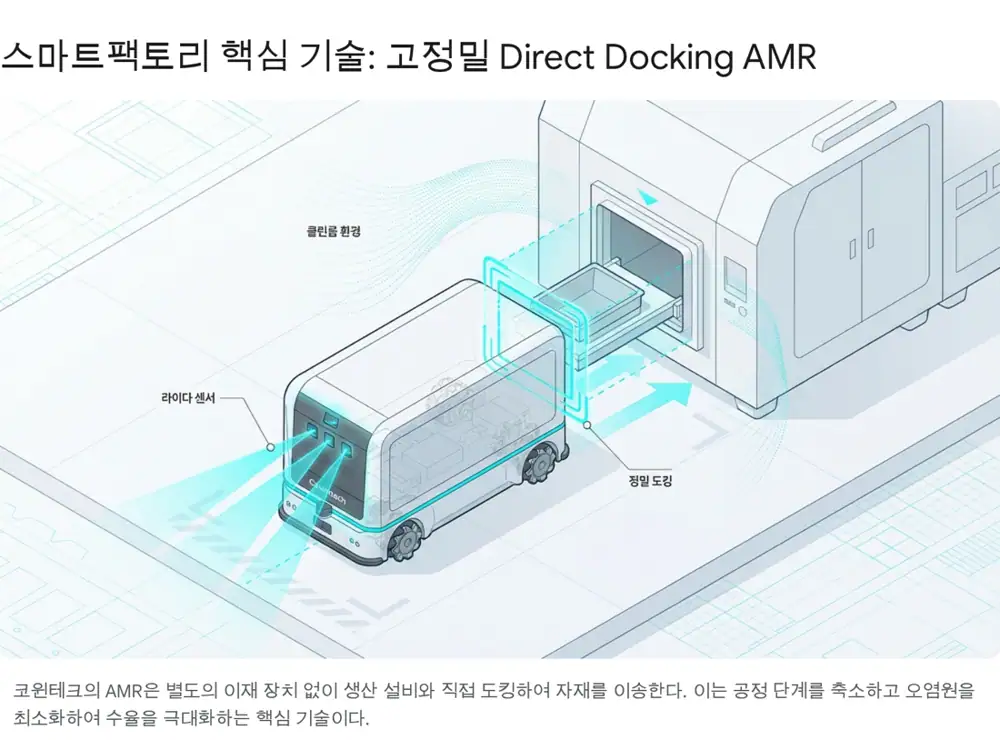

2. Technology moat: Direct Docking AMR

Cowintech's core capability is automating electrode, assembly, and formation processes. Front-end automation is difficult because materials such as electrode rolls can weigh up to one ton and are sensitive to vibration.

Official fact: The source explains that Direct Docking AMR lets the robot dock directly with production equipment to insert or retrieve materials without a separate transfer device.

Interpretation: Positioning precision of ±1mm, real-time robot-equipment communication, and LiDAR/Vision sensor fusion are the core advantages. Customer value comes from better space efficiency, lower CAPEX, and fewer particles.

Autonomous mobile robots

SLAM-based robots avoid obstacles and move everything from heavy electrode rolls to light boxes.

Automated storage

Stacker-crane systems with explosion-proof and dust-proof design for battery materials.

Software

Robot control, dispatch, lot tracking, and MES/ERP integration.

3. TopMaterial: the turnkey puzzle piece

TopMaterial's system-engineering business provides factory layout, equipment specification, and process optimization consulting to new battery companies and automakers with limited manufacturing experience. Cowintech equipment can be specified during that process, creating a loop from engineering to equipment orders and material supply.

- LFP cathode: a material seeing higher demand as EV price competition intensifies.

- Electrode foundry: a model that supplies semi-finished electrodes from the Asan fourth-site high-performance electrode line.

- Turnkey strategy: bundles engineering, materials, and equipment into a one-stop solution for new battery companies.

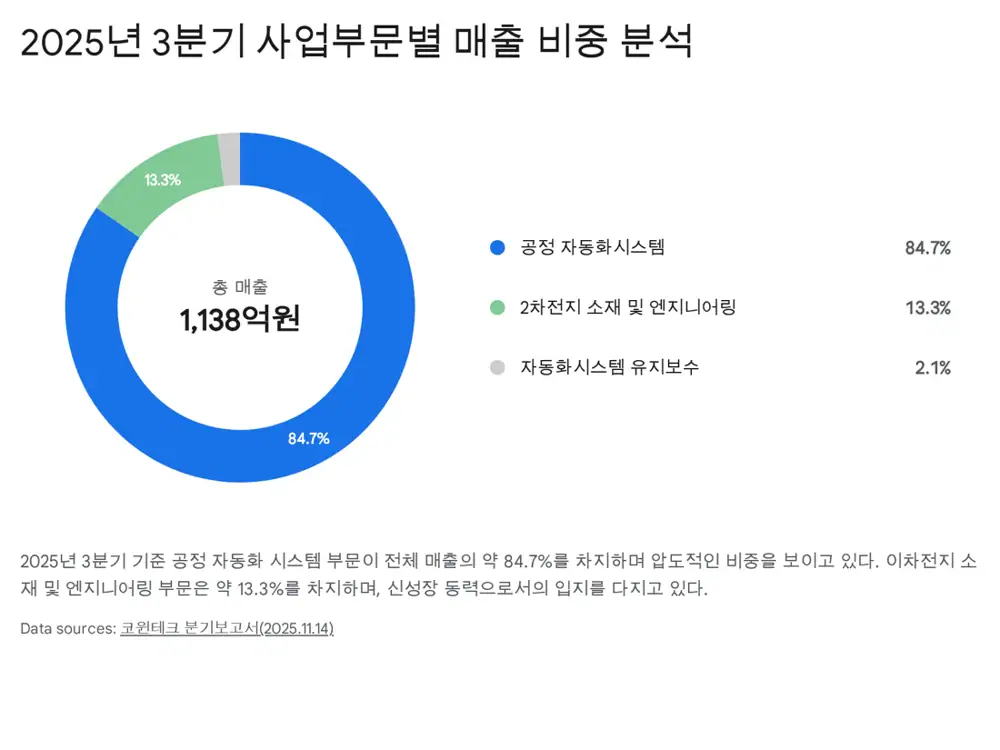

4. Q3 2025: losses and backlog together

Official fact: Cumulative Q3 2025 revenue was KRW 113.774bn, down about 46% from KRW 210.559bn a year earlier, and operating profit turned to a KRW 5.2bn loss.

| Item | Source figure | Meaning |

|---|---|---|

| Order backlog | KRW 256.779bn | Above 2024 annual revenue of KRW 244.390bn |

| Process automation | KRW 225.9bn | Most of the backlog |

| Battery engineering | KRW 30.9bn | Linked to TopMaterial |

| R&D | KRW 4.3bn, 3.8% of revenue | Technology investment continued despite losses |

The source attributes weak earnings to delayed customer investments during the EV chasm, fixed costs from the Asan third-site expansion and overseas staffing, and continued R&D. It also cites an A- credit rating from Korea Rating Data in April 2025 as evidence of financial stability.

5. Market and risks

The source says the global AMR market is expected to grow from about USD 4.49bn in 2025 to USD 9.26bn in 2030, a 15.6% CAGR. Cowintech is also trying to reduce EV battery dependence through ESS manufacturing-line AMR supply.

- End-market investment slowdown: prolonged chasm could delay or cancel orders.

- Raw materials: steel, copper, and aluminum price increases pressure cost.

- FX: higher overseas revenue raises volatility.

- Responses: semiconductor/general logistics, MRO, diversified sourcing, and currency futures hedging.

6. Conclusion

My conclusion is that Cowintech should be judged more by backlog and automation technology than near-term earnings. The 2026 recovery depends on how fast orders such as the KRW 23.9bn electrode-process automation contract from January 2025 and the KRW 19.8bn AMR supply contract from July are recognized as revenue.