DEEP RESEARCH · TSAVORITE

Tsavorite Scalable Intelligence Deep Dive

A review of whether OPU, MultiPlexus Fabric, TAOS, and Samsung Foundry cooperation can become a post-GPU alternative.

0. Bottom line first

Tsavorite's appeal is not a direct replacement of NVIDIA GPUs, but a targeted attempt to solve inference and agentic-AI efficiency through composable chiplets. However, the source includes estimates and simulated analysis, so verifiable orders, production, and customer evidence matter most.

- TSI is described as a fabless company headquartered in Milpitas with a core R&D center in Bengaluru.

- The main products are OPU, Helix AI appliances, and the TAOS software platform.

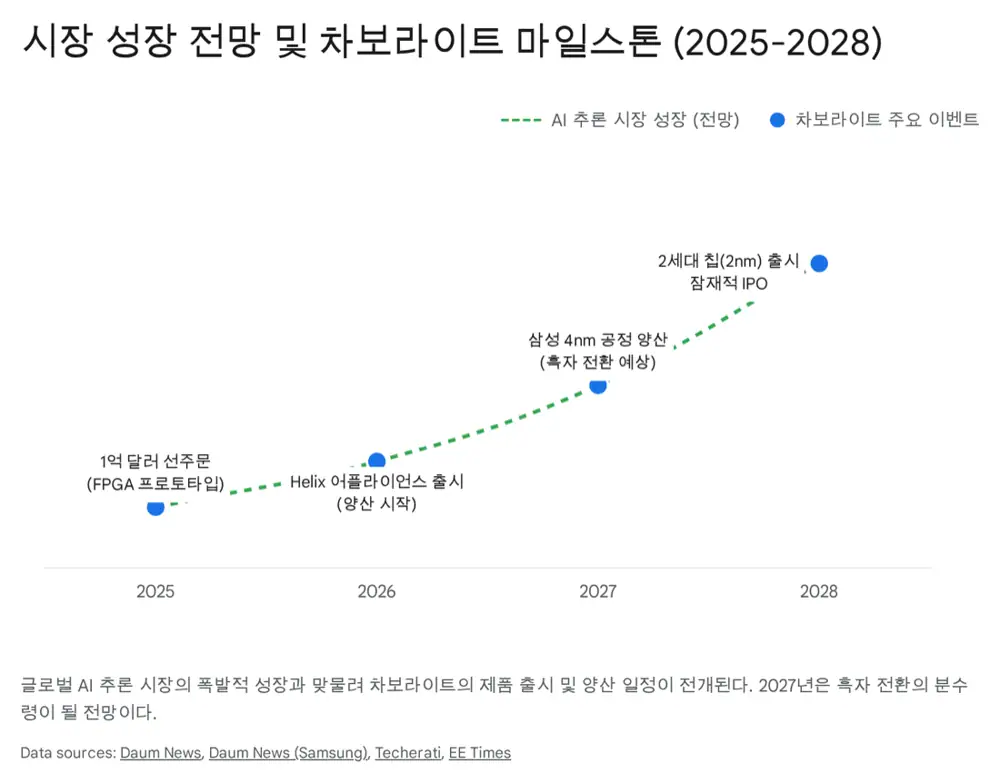

- The source cites 2023 founding, no public financial statements, about $17.9 million raised, and more than $100 million in pre-orders.

1. AI infrastructure inflection and TSI's position

The source's premise is that 2023~2024 was about training-GPU scarcity, while 2025 onward is about inference and agentic-AI efficiency. As TCO and power consumption rise, workload-specific architectures become more attractive.

Interpretation: TSI's OPU narrative is less “build the biggest chip” and more “combine the right functions for efficiency.”

2. Business model and customers

OPU chipset sales

The source describes T0~T3 scalable SoC accelerators from edge to data centers.

Helix AI appliance

A turnkey rack solution linking thousands of OPUs through high-speed fabric.

TAOS licensing

A subscription-style software model for performance optimization and support.

Target customers are sovereign cloud and AI service providers, on-device AI and robotics companies, and large enterprises in finance, pharma, and other sectors that need private data centers.

3. Cash flow and funding history

Official fact: The source explicitly says TSI is a private startup founded in 2023 with no disclosed financial statements.

Interpretation: Its cash-flow section should therefore be treated as simulated analysis. The source frames 2023 as R&D and hiring, 2024 as FPGA prototypes and Samsung SF4X MPW work, and 2025 as pre-orders plus production preparation.

| Item | Source figure/detail | Meaning |

|---|---|---|

| Total funding | About $17.9 million, roughly KRW 24 billion | Small for chip development, implying future funding need |

| Series A | About $14.16 million in February 2025 | Post-money valuation cited around $260 million |

| Series A-1 | About $3.74 million | Additional funding at the same valuation |

| Pre-orders | More than $100 million | Potential customer-advance leverage |

4. Moat and competition

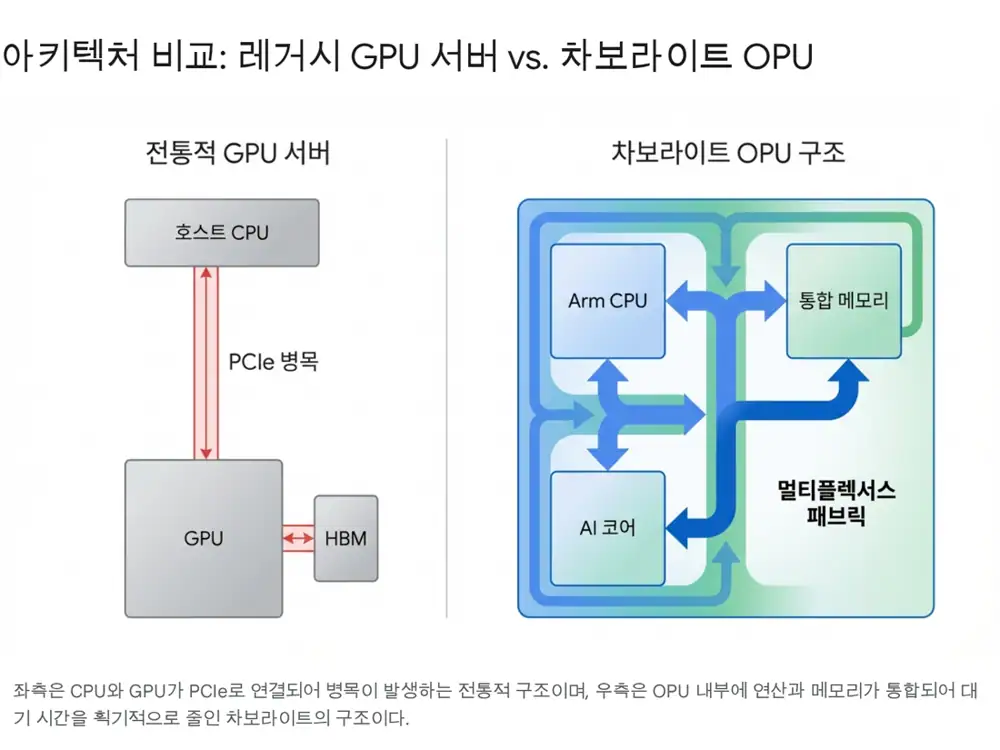

The source's core moat is MultiPlexus Fabric and unified memory. It claims TSI reduces PCIe bottlenecks in GPU-CPU systems and lets thousands of cores act like one processor through chiplet-to-chiplet links.

| Competitor | Source view | TSI difference |

|---|---|---|

| NVIDIA | Dominant, but expensive and power-hungry | TSI emphasizes efficiency and composability |

| AMD | Chasing with MI300, but ROCm maturity remains an issue | TSI claims a hardware-software integrated approach |

| Tenstorrent | RISC-V, chiplets, and IP licensing create a similar model | The most direct comparison group |

| Rebellions/FuriosaAI | Korean NPU startups focused on domain efficiency | TSI claims a broader CPU-inclusive platform |

5. Growth roadmap and risks

- 2025: stabilize Samsung 4nm production and secure early customer references.

- 2026: pursue U.S. CHIPS Act support and public-sector entry, with Made-in-USA messaging linked to the Taylor fab.

- 2027: expand into automotive and robotics, and review Samsung 2nm SF2 adoption.

The risks are clear: dilution in Series B/C rounds, possible venture debt or mezzanine financing, production yield, software ecosystem maturity, and real customer validation. I would treat TSI as a high-risk, high-return deep-tech candidate while separating narrative from verifiable facts.

Sources

- Source 1: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224123844383

- Source 2: https://www.techerati.com/news-hub/ai-startup-tsavorite-achieves-100-million-in-advanced-ai-chip-pre-orders/

- Source 3: https://tsavoritesi.com/

- Source 4: https://www.technetbooks.com/2025/12/samsung-foundry-secures-major-ai-chip.html

- Source 5: https://medium.com/@aayushbhatnagar_10462/nvidia-blackwell-vs-google-tpu-trillium-the-battle-for-ai-compute-in-2025-23de5ea41a80

- Source 6: https://xpu.pub/2025/04/16/google-ironwood/

- Source 7: https://groq.com/blog/the-groq-lpu-explained

- Source 8: https://aiixx.ai/blog/groq-ai-chips-vs-nvidia?ref=odinhalvorson.com

- Source 9: https://patents.google.com/patent/US5822602A

- Source 10: https://utilizingtech.com/category/podcast/season-4/

- Source 11: https://www.eetimes.com/raza-named-new-president-at-amd/

- Source 12: https://www.eetimes.com/the-creators/

- Source 13: https://forgeglobal.com/tsavorite-scalable-intelligence_ipo/

- Source 14: https://pitchbook.com/profiles/company/636013-27