DEEP RESEARCH · EXYNOS 2600 · SAMSUNG FOUNDRY

Strategic Inflection: Exynos 2600, Galaxy S26 and the Reshaping of Samsung's Foundry Ecosystem

How 2 nm GAA, HPB packaging and yield recovery rewire mobile AP economics and Korea's OSAT supply chain

0. Bottom line first

The Exynos 2600 is not just another AP — it is Samsung's bet to break a roughly KRW 11.7 tn annual dependence on Qualcomm and to prove the production credibility of its 2 nm (SF2) GAA process. If SF2 yields settle around 60–70% by year-end 2025 and HPB packaging tames the heat, the most direct winners are back-end suppliers like Hana Micron, LB Semicon and Nepes.

Interpretation: This note walks through (a) the cost bleed from Qualcomm dependence, (b) the technical reality of SF2 + HPB, (c) the DSP / OSAT / materials supplier lineup, and (d) the equity and ETF playbook.

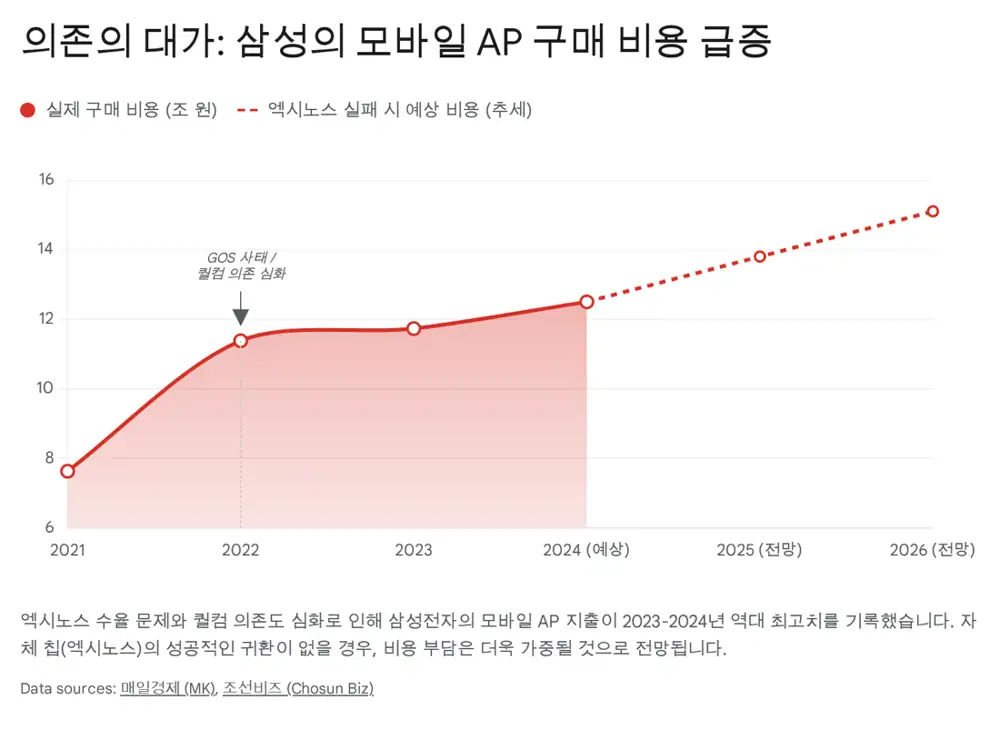

1. Strategic rationale: the KRW 11 tn dilemma

Official fact: Samsung's DX division spent KRW 11.732 tn on mobile AP procurement in 2023 — up more than 50% from KRW 7.629 tn in 2021. AP cost runs at roughly 20% of smartphone BOM.

Official fact: Each Exynos die is estimated to save USD 30–50 vs an equivalent Snapdragon. With ~30 m Galaxy S26 units a year and a 50% Exynos mix, that translates into trillion-won-scale savings.

Interpretation: The biggest value of Exynos is not the mix itself but the negotiating leverage that "an alternative exists" — that leverage tightens Qualcomm ASPs and defends Samsung's overall margin.

2. Technical architecture of Exynos 2600

SF2 — 2 nm GAA / MBCFET

~10–15% perf, +25–30% power efficiency vs SF3, density target >300 Mtr/mm².

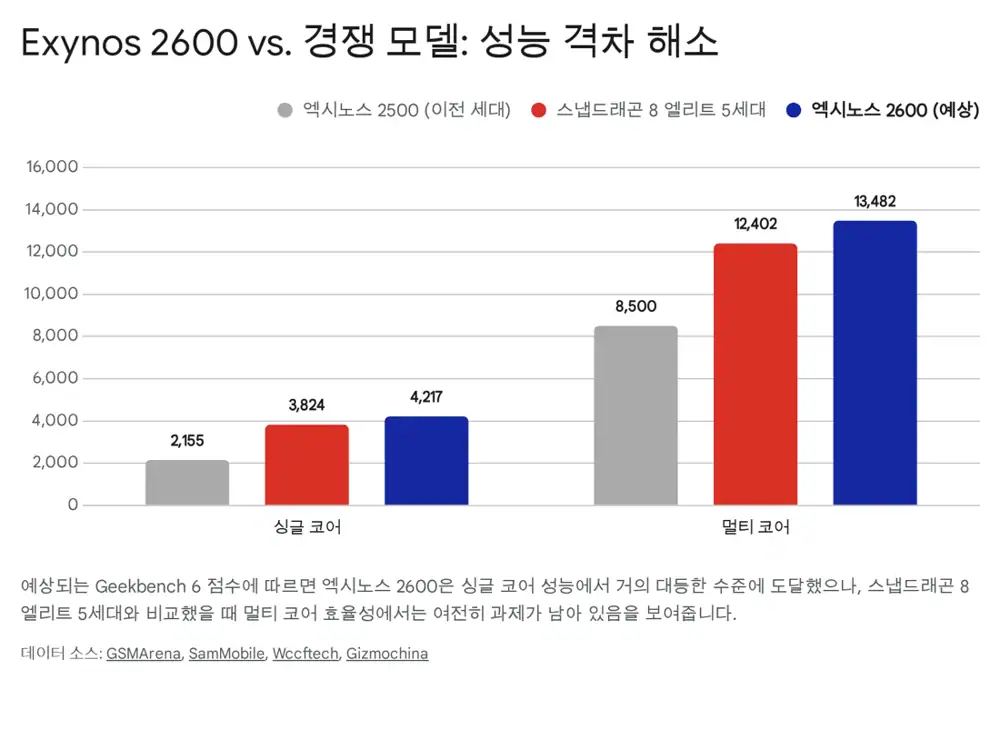

Deca-core with Cortex-X-class prime

Geekbench 6 single ~4,217 (+37% YoY), multi ~13,482 — head-to-head with Snapdragon 8 Elite Gen 5.

Xclipse 960 (AMD RDNA)

Ray-tracing performance +50% vs predecessor.

+113% AI throughput

Runs Galaxy AI features (live translate, generative edit) fully on-device.

3. The yield Valley of Death — and recovery

Official fact: SF2 yields sat at 10–20% in early-mid 2024, climbed to ~30% in Q1 2025 and 50–60% by November 2025. Samsung targets ~70% by year-end 2025.

Official fact: Root causes include overlay error in EUV double patterning and inconsistent nanosheet etch. New EUV photoresists (Dongjin Semichem) and high-selectivity etch gases drove the recovery.

Interpretation: 60% is the empirical inflection where OSAT and materials revenue visibility steps up. A stall at 40–50% would shrink the addressable footprint of Exynos to Korea/Europe and cap supplier upside.

4. Game changer: Heat Path Block (HPB) packaging

Interpretation: HPB is not Exynos-only — Samsung Foundry can offer it as a turnkey to Qualcomm and Apple. If Snapdragon 8 Elite continues to struggle with heat, HPB tilts the foundry-share game.

5. Galaxy S26 launch and price defense

Official fact: Galaxy S26 is expected to debut late January – early February 2026. Memory and wafer cost inflation is squeezing BOM; Snapdragon 8 Elite Gen 5 pricing is expected to rise on TSMC N3P costs.

Interpretation: If Exynos captures 50–60% of global volume, Samsung can freeze ASPs (~$799+) and out-price rivals. Some Street estimates put 2026 Samsung operating profit as high as KRW 73 tn under a memory-supercycle + Exynos success scenario.

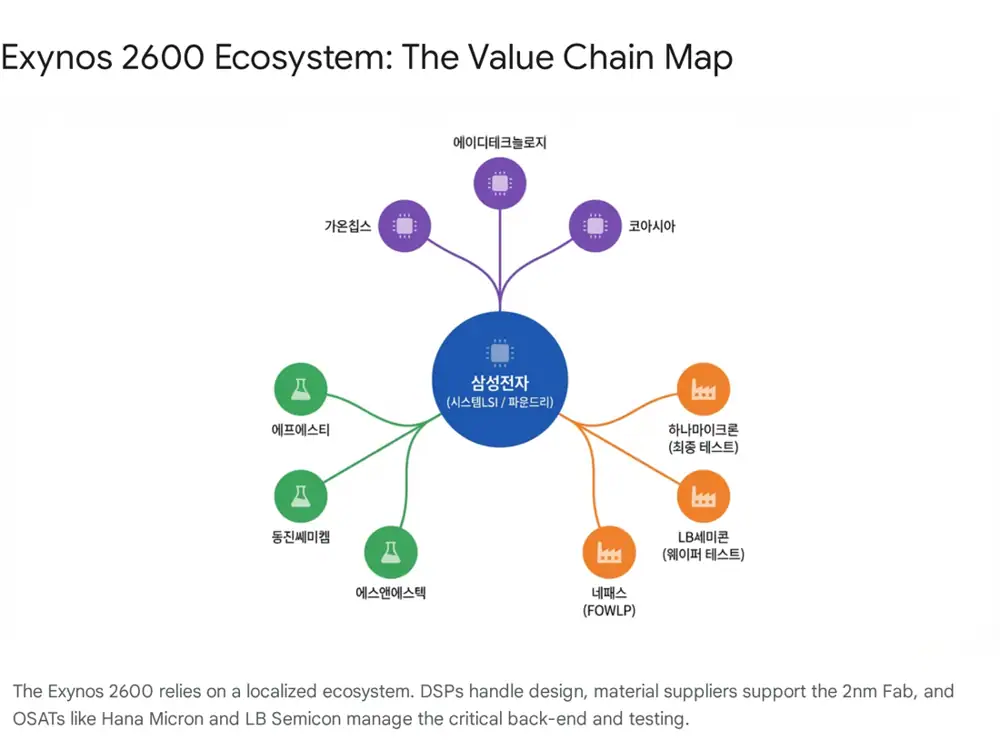

6. Supply-chain winners

6.1 Design Solution Partners (DSPs)

- ADTechnology: Migrated from the TSMC ecosystem to Samsung, strong in advanced nodes ≤ 8 nm; well positioned for 2 nm design wins.

- Gaonchips: Tightest DSP relationship with Samsung Foundry; landed Japan PFN's 2 nm AI accelerator project. Likely deep involvement in Exynos derivatives and automotive variants.

6.2 OSAT — the volume gatekeepers

Hana Micron

Turnkey packaging/test partner for Exynos; rents Samsung's Cheonan/Onyang lines. Utilization keys directly off Exynos volume; Vietnam capacity cuts should unwind as production ramps.

LB Semicon

Pivoting from DDI test to high-margin SoC wafer test for Exynos 2600; capex funded by the LB Lusem merger.

Nepes

FOWLP / RDL specialist needed for HPB enablement. Nepes Laweh capex weighs on near-term financials but capability is essential.

6.3 Materials & components

- FST: Core EUV pellicle supplier; demand scales with EUV exposures. Strategic partner with Samsung minority stake.

- Dongjin Semichem: Localized EUV photoresist — secular volume tailwind from sub-3 nm scaling.

7. Investment strategy & ETF angle

| Approach | Profile | Best fit |

|---|---|---|

| Single names (Hana Micron, LB Semicon) | Highest correlation to Exynos volume, high beta | High-conviction, high-volatility investors |

| Sector ETFs (back-end / materials) | Diversifies single-name risk, smooths exposure | Diversified investors |

8. Conclusion & risks

Bottom line: "Cautiously Bullish." 2 nm GAA + HPB packaging has the potential to crack the performance/heat trade-off, but the catalyst path runs through 70% yield, real-world S26 benchmarks (avoiding a GOS 2.0), and HPB ramp execution.

- Upside triggers: SF2 yields reach 70%, S26 reviews praise thermals/sustained performance, NVIDIA / Tesla-grade external customer wins.

- Downside triggers: Yields stall in the 50s, Exynos mix gets cut, HPB ramp issues.

Sources

- Original Naver blog post

- Exynos Galaxy S26 beneficiaries / ETF deck: drive.google.com/...

- MK — Samsung AP procurement at KRW 11 tn: mk.co.kr

- ChosunBiz — Samsung AP procurement: biz.chosun.com

- Exynos 2600 tech / stocks deck: drive.google.com/...

- KED Global — Exynos 2600 unveil: kedglobal.com

- TechInsights — 2 nm GAA leap: techinsights.com

- Rapidus — 2 nm challenges: rapidus.inc

- SamMobile — Exynos 2600 vs Snapdragon 8 Elite Gen 5: sammobile.com

- Gizmochina — Geekbench comparison: gizmochina.com

- Wccftech — Geekbench 6 results: wccftech.com

- GSMArena — Exynos 2600 launch: gsmarena.com

- Design Reuse — 2 nm yield ≤ 20%: design-reuse.com

- Reddit — 2 nm yield 10–20%: reddit.com

- TrendForce — 55–60% 2 nm yield: trendforce.com

- The Economy — 2 nm mass-production progress: economy.ac

- Wccftech — Exynos 2600 30% yield run: wccftech.com

- Samsung Foundry cooling tech deck: drive.google.com/...

- PhoneArena — Exynos 2600 stays cool: phonearena.com

- TechPowerUp — HPB adoption potential: techpowerup.com

- Gizmochina — HPB explained: gizmochina.com

- Towards Packaging — HPB outlook: towardspackaging.com

- Fone4U — Galaxy S26 specs / pricing: fone4u.ie

- India TV — S26 February 2026 launch: indiatvnews.com

- Chosun — Korea memory supercycle: chosun.com

- Samsung News — 2 nm GAA + 2.5D turnkey for PFN: news.samsung.com

- Vietcetera — Hana Micron Vietnam investment: vietcetera.com

- TrendForce — Hana Micron Vietnam capacity cut: trendforce.com

- Nepes / LB Semicon Exynos deck: drive.google.com/...

- RCR Tech — LB Semicon tapped for Exynos: rcrtech.com

- TheLec — LB Semicon Samsung AP/sensor tests: thelec.net

- Nepes IR — PMIC AI orders: nepes.co.kr