DEEP RESEARCH · Nepes Ark

Nepes Ark: Exynos 2600 and the 2nm test bottleneck

PMIC cash flow, SoC test expansion, and HPB thermal testing as structural growth drivers

0. Bottom line first

Nepes Ark has lived with Exynos volatility, but PMIC stability, a larger SoC mix, and rising 2nm/HPB test difficulty could put it into a structural growth window from late 2025 into 2026.

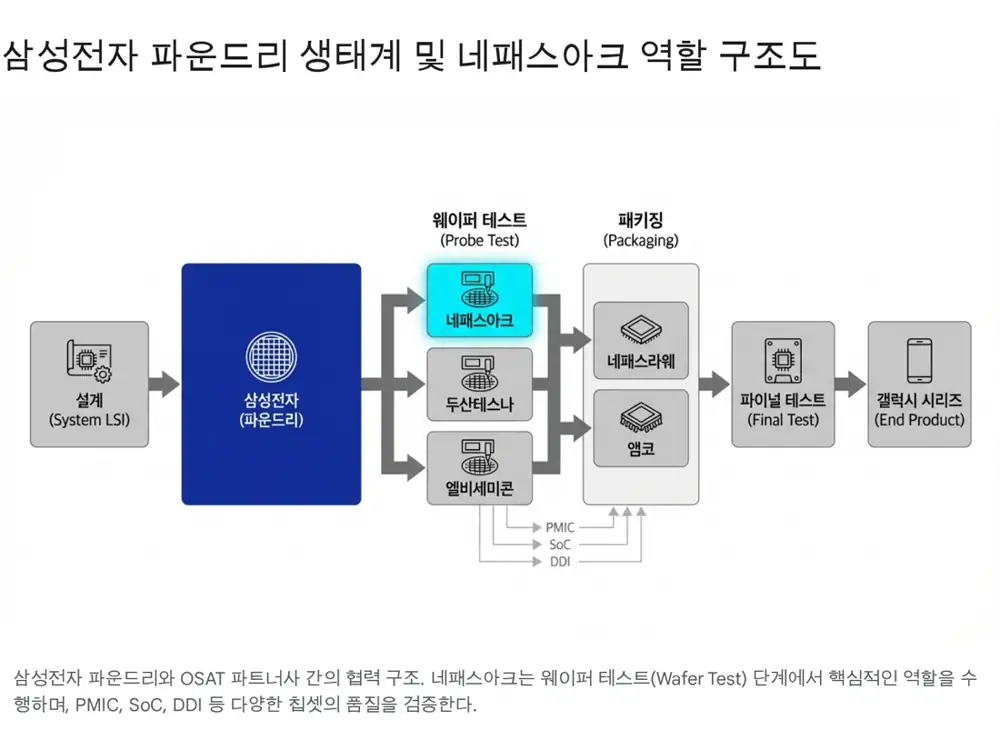

Official fact: Nepes Ark was established on April 1, 2019 through the physical spin-off of Nepes' semiconductor test division. The Nepes group built vertical integration across Nepes for WLP/FOWLP packaging and bumping, Nepes Ark for wafer/final test, and Nepes Lawe for FO-PLP.

Interpretation: Testing has moved from simple defect screening to a bottleneck for yield stabilization and performance assurance in advanced nodes.

60-70%

Estimated Samsung PMIC test share in 2021-2023.

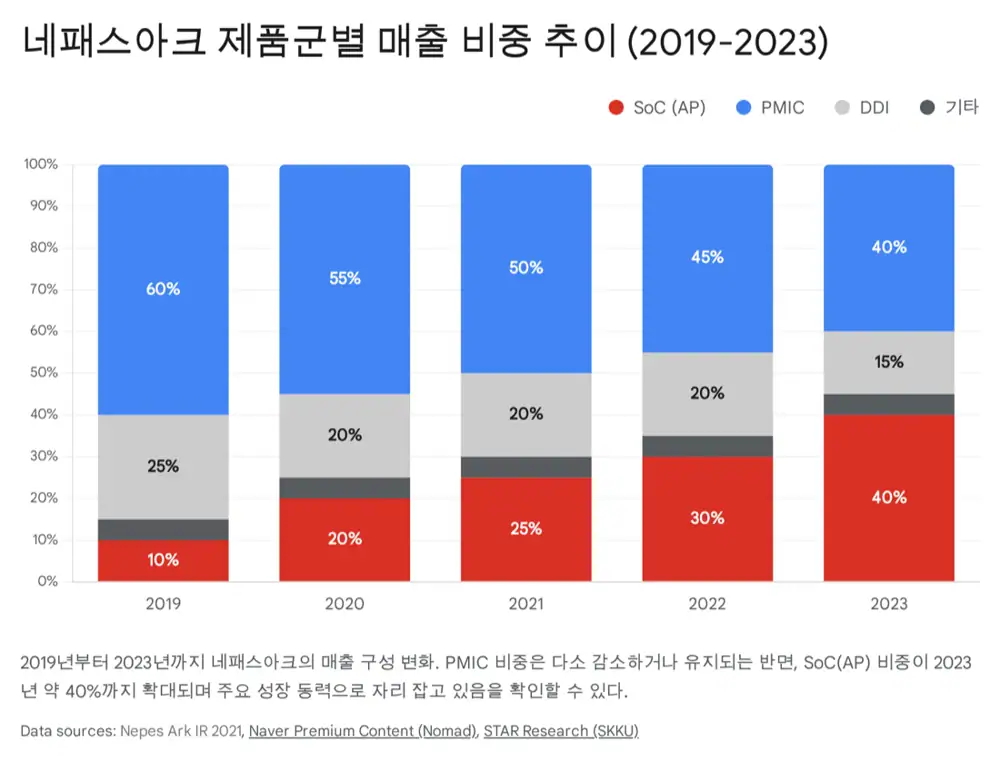

About 40%

Share of Nepes Ark revenue from SoC testing at end-2023.

About 65%

Samsung DDI test share cited in the source.

1. Role in the Exynos ecosystem

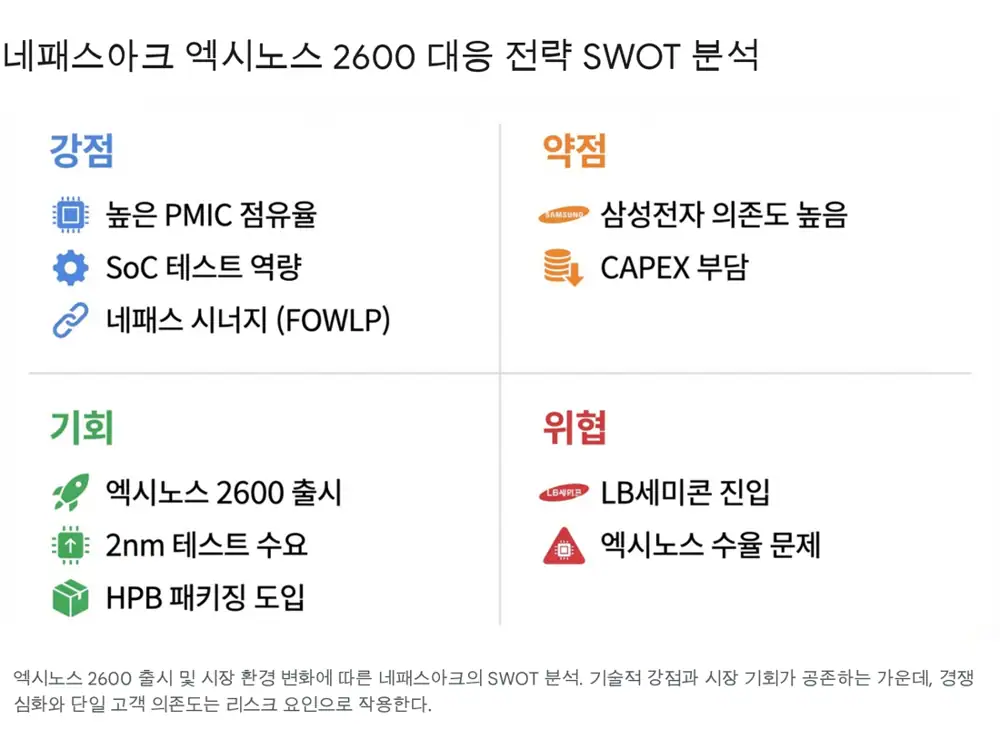

A smartphone contains 7-8 PMICs, which supply the right voltage and current to the AP, camera, display, and other parts. From its early days, Nepes Ark focused on wafer testing for Exynos PMICs, and PMIC demand tied to smartphone shipments acted as a cushion when Exynos AP share fluctuated.

SoC testing has a higher barrier. At inception in 2019, SoC/AP testing was only about 10% of revenue. Using IPO proceeds from 2020, the company invested in SoC test equipment such as Teradyne UltraFLEX. The source says the SoC mix rose to the 20% range in 2020, 25% in 2021, and about 40% by end-2023.

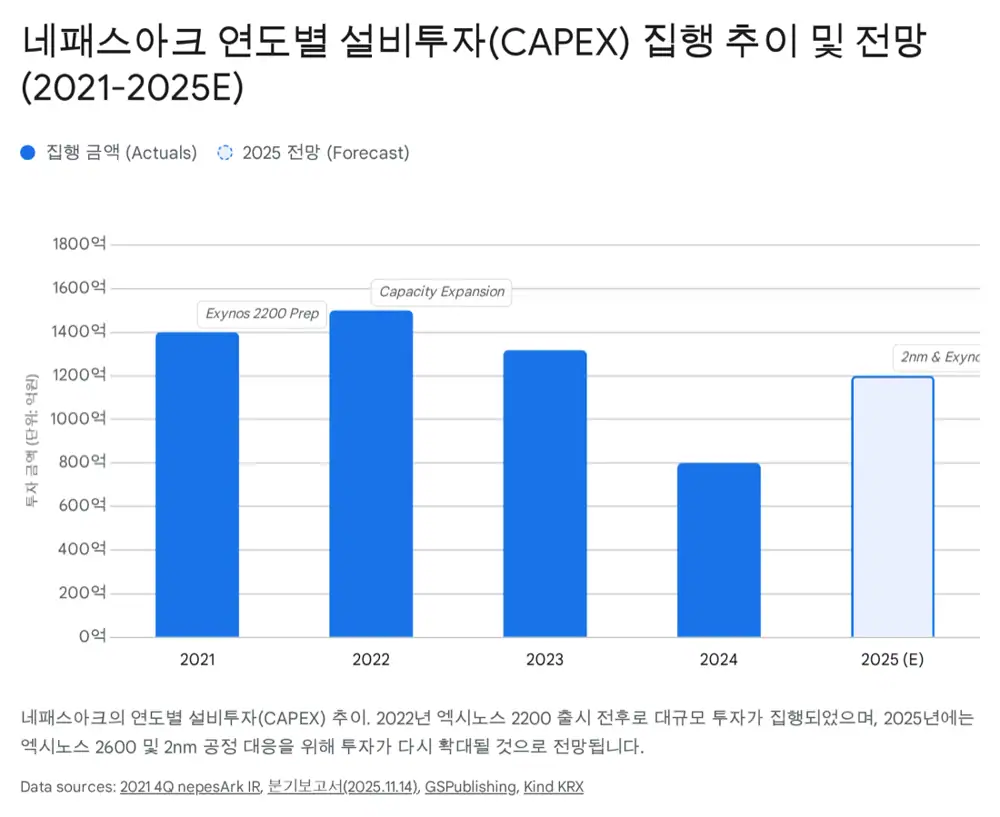

2. 2023-2025 CAPEX flow

| Year | CAPEX and direction | Meaning |

|---|---|---|

| 2023 | About KRW 131.7bn | Continued SoC tester, PMIC capacity, and probe-card investment despite S23 excluding Exynos 2300 |

| 2024 | About KRW 48.2bn of tangible-asset purchases through Q3 | Supported Exynos 2400's partial return while focusing on efficiency and supplemental investment |

| 2025 outlook | Could rise 30-50% YoY and exceed KRW 100bn | Prepares for 2nm SF2, Exynos 2600, and possible Tesla autonomous-driving chip or AI accelerator tests |

Official fact: For 2024, the source mentions replacement of aging equipment, software upgrades, automation, and interface board/test socket investment for Exynos 2400's 10-core CPU and AMD GPU architecture.

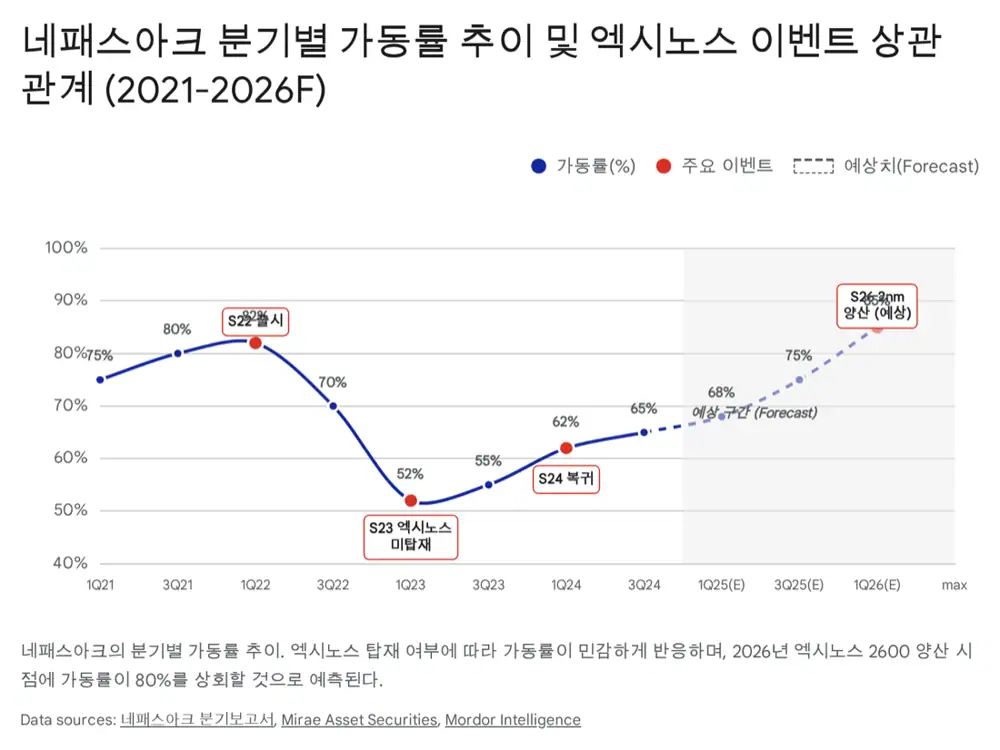

3. Exynos 2600 and utilization model

The source views Exynos 2600 adoption in the 2026 Galaxy S26 as likely, but frames three scenarios because yield and market trust remain variables.

| Scenario | Adoption share | Read |

|---|---|---|

| Aggressive | More than 50% of global volume | Coverage expands beyond Korea and Europe to Southeast Asia and South America |

| Strategic split | About 30-40% | Korea and parts of Europe, with North America and China mainly Snapdragon 8 Gen 5 |

| Limited | Only select models or countries | 2nm yield misses expectations |

Official fact: Past utilization is cited as 70-80% during Exynos 2200 production in 2021-early 2022, low-50% after the Exynos 2300 was excluded in 2023, and mid-60% after the partial Exynos 2400 return in 2024.

Interpretation: The source assumes 2nm test time per wafer can rise about 20-30% versus 4nm. Even if chip volume is similar, longer equipment occupancy can lift both unit revenue and utilization.

75%

Potential utilization entry point in the source.

85%+

Near full capacity and an operating-leverage zone.

+20-30%

Assumed equipment occupancy increase from 2nm complexity.

4. Competition: is LB Semicon zero-sum?

Samsung's addition of LB Semicon as an Exynos 2600 wafer-test partner raises near-term share concerns. The source says Doosan Tesna and Nepes Ark previously split Exynos test volume at roughly 40-50% each.

Interpretation: But if 2nm test time rises 20-30%, the total test demand pool itself grows. LB Semicon's entry may be not only share loss, but Samsung's capacity and pricing-risk management.

5. 2nm GAA, HPB, and thermal test

2nm GAA uses an MBCFET structure in which the gate surrounds all four sides of the channel. It improves power efficiency and performance, but makes tiny defects in stacked nanosheets harder to detect. That requires more precise probe cards, higher-resolution test equipment, and longer test time.

HPB mitigates the heat trap of conventional PoP structures by placing memory beside the AP or using FOWLP, then attaching a copper heat sink on the chip to dissipate heat directly.

Official fact: The source says thermal-characteristic tests become more important for HPB chips and that Nepes Ark could add advanced Thermal Test processes to raise test pricing. It also names AI-compute test algorithms for stronger NPUs, RFIC/5G testing, and FOWLP/PLP-linked test as roadmap items.

6. Checkpoints and risks

- Exynos 2600's 2nm yield must actually stabilize.

- Nepes Ark's AP test share defense after LB Semicon's entry matters.

- High PMIC share and AP+PMIC turnkey experience support the defense case, but Samsung's pricing pressure remains a variable.

- Key KPIs are utilization, test time, CAPEX pace, Thermal Test pricing, and Samsung vendor allocation.

Sources

- Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224123604297

- 엑시노스 2600 기술 분석 및 관련주: https://drive.google.com/open?id=12eZw1s0FO0HeGHIhbActmOmVkplvY3Ao5c66E7SqRGQ

- 네패스아크 (KQ.330860) - 성균관대학교 금융투자학회 S.T.A.R: https://www.starskku.com/fileRequest/download?file=%2Fboard%2Fresearch%2F20240311172036_7317.pdf&save=STAR_%E1%84%82%E1%85%A6%E1%84%91%E1%85%A2%E1%84%89%E1%85%B3%E1%84%8B%E1%85%A1%E1%84%8F%E1%85%B3.pdf

- 2024.03.21.(목) 증권사리포트 "네패스아크, AP 수요 증가로 양호한 매출 실적 유지 중": https://contents.premium.naver.com/nomadand/nomad/contents/240321044222793um

- NEPC's 2025 Market Themes: https://www.nepc.com/nepcs-2025-market-themes/

- 2025 Capex Outlook: A Gradual Rebound After the Factory-Building Boom (Peng) - Goldman Sachs Research: https://www.gspublishing.com/content/research/en/reports/2024/11/11/82636d37-ea1f-4897-880d-8172bce83bae.html

- Samsung's 2nm Breakthrough! Exynos 2600 & Tesla Chips Are Changing Everything: https://www.youtube.com/watch?v=upkdb0vRsms

- Samsung's improvement in yield bodes well for the Exynos 2600 AP to power the Galaxy S26, S26+ - PhoneArena: https://www.phonearena.com/news/samsung-foundry-yield-rises_id175817

- Samsung turns to LG partner to test upcoming Galaxy S26 Exynos chips - Notebookcheck: https://www.notebookcheck.net/Samsung-turns-to-LG-partner-to-test-upcoming-Galaxy-S26-Exynos-chips.1169544.0.html

- [News] Samsung Exynos 2600 May Cover Just 30% of Galaxy S26 Production Amid Reported Yield Issues - TrendForce: https://www.trendforce.com/news/2025/10/24/news-samsungs-exynos-2600-may-cover-just-30-of-galaxy-s26-production-as-2nm-yield-issues-persist/

- Samsung Expands Chip Testing as Exynos 2600 Prepares for Galaxy S26 Series: https://sammyguru.com/samsung-expands-chip-testing-as-exynos-2600-prepares-for-galaxy-s26-series/

- LB세미콘, 삼성전자 '엑시노스 2600' 테스트 맡는다: https://www.etnews.com/20251121000092

- Challenges And Outlook Of ATE Testing For 2nm SoCs - Semiconductor Engineering: https://semiengineering.com/challenges-and-outlook-of-ate-testing-for-2nm-socs/

- Samsung's Heat Path Block Technology May Power Cooler Qualcomm and Apple Chips: https://www.towardspackaging.com/news/samsung-heat-path-block-technology-qualcomm-apple

- Exynos 2600 has a new innovation that's attracting Apple and Qualcomm - Reddit: https://www.reddit.com/r/hardware/comments/1pmnzdp/exynos_2600_has_a_new_innovation_thats_attracting/

- Samsung Exynos 2600 introduces a heat-cutting tech no mobile chip used before: https://www.sammyfans.com/2025/12/18/samsung-exynos-2600-chip-heat-path-block/