DEEP RESEARCH · Inhwa Precision (101930.KQ)

Inhwa Precision (101930) Deep Dive: Structural Beneficiary of the Shipbuilding Super-cycle & A Strategic Pivot in Capital Allocation

A marine-engine-parts cash cow stacked on top of a ~KRW 250B recovery from the Hanwha Engine stake — graduating from "manufacturer" to "capital allocator"

0. Bottom line first

Inhwa Precision is no longer just a marine-engine parts supplier. Operating leverage in the core business (3Q25 operating profit +309.2% YoY) and a ~KRW 250B+ recovery from the Hanwha Engine stake are firing simultaneously. Cash and liquid assets explain a large share of the KRW 434.8B market cap, and debt-to-equity is 39.5% — even after the US product-liability litigation discount, the downside looks well-cushioned.

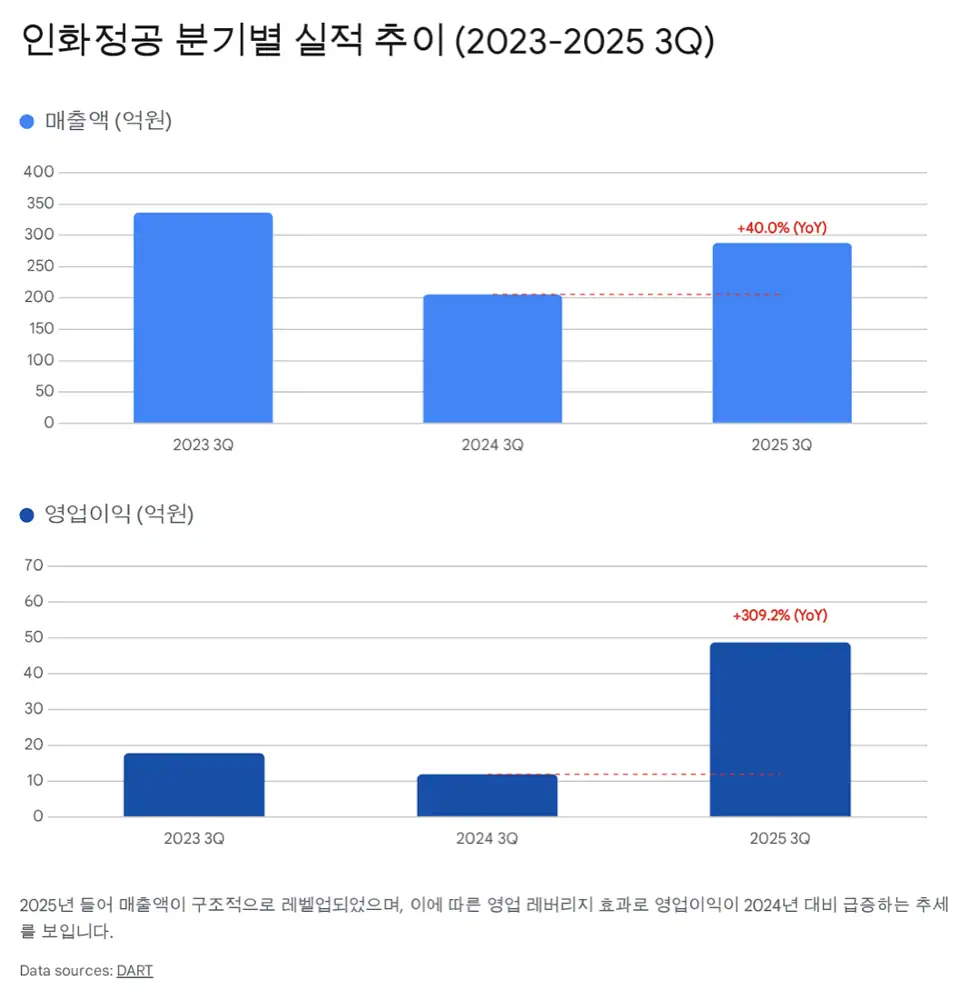

Official fact: 3Q25 revenue KRW 28.79B (+40.0% YoY), operating profit KRW 4.87B (+309.2% YoY), OPM 16.9%. 3Q YTD: revenue ~KRW 82.5B, operating profit ~KRW 11.9B, net income ~KRW 13.8B. Total assets KRW 463.2B, liabilities KRW 131.2B, equity KRW 331.9B, debt-to-equity 39.5%.

Interpretation: Revenue +40% but operating profit +309% — a textbook operating-leverage moment after crossing breakeven in a high-fixed-cost business. Stack the Hanwha Engine monetization (~KRW 137.4B in 2024 + ~KRW 121.2B in 2025 vs. ~KRW 100B initial investment) on top, and you get a dual-engine "core business + investment" model. The US litigation exposure (~KRW 35B, lost at first instance) is absorbable from cash.

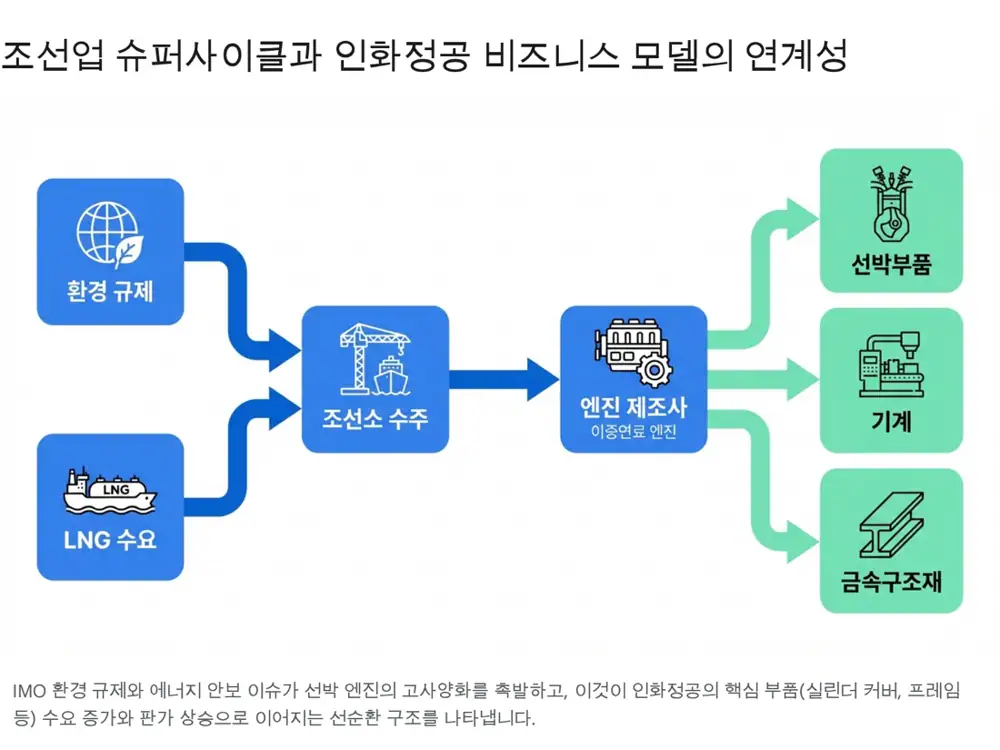

1. Industry context — paradigm shift in marine equipment

1.1 The super-cycle's true engines — forced replacement + energy security

The mid-2020s shipbuilding boom is structurally different from the early-2000s cycle. IMO environmental rules (EEXI / CII) are driving a "forced replacement" wave, while the Russia–Ukraine war and Middle East risk are spurring LNG/LPG carrier orders under the "energy security" thesis. The marine engine market is transitioning from diesel to methanol / ammonia / hydrogen dual-fuel engines — which means higher-spec parts and higher unit prices.

1.2 Inhwa's strategic position

Founded in 1999, Inhwa produces marine-engine core parts — cylinder cover, cylinder frame, bed plate — and is a key partner to Korea's three engine builders: Hanwha Engine, HD Hyundai Heavy Industries, and HD Hyundai Marine Engine. Aggressive M&A and equity investments have transformed it from a pure manufacturer into a composite enterprise with strong capital-allocation skills. The Hanwha Engine (formerly HSD Engine) trade — investment returns dwarfing core operating profit — is the proof point.

2. Governance and corporate structure

2.1 From a job-shop to a diversified manufacturing group

Founded January 8, 1999, in Changwon, South Gyeongsang. The company began as a simple machining shop, then registered as a vendor to Hyundai Heavy (1999), Doosan Heavy (now Doosan Enerbility, 2000), and Hanwha Engine (formerly HSD Engine, 2001). The October 2010 KOSDAQ listing was the inflection point — the proceeds funded an M&A strategy that culminated in the 2012 Haedong Industries acquisition (metal forming machinery) and the 2013 Samhwan General Machinery acquisition (metal structures), building a hedge portfolio against shipbuilding cyclicality.

2.2 Board — a deliberately slim decision body

- CEO Yi In (Inside Director): b. 1970, BA Psychology Seoul National University. 26+ years at the helm and largest shareholder. Led founding, listing, and major M&A.

- Director Lee Jae-gu (Inside Director): b. 1961, BA Accounting Changwon University. Former Head of Management Planning at SKEM. Heads administration and disclosure (18+ years on board).

- Director Jang Jik-su (Other non-executive): b. 1961, ex-CEO of a tax/accounting firm — provides financial advice.

- Director Kim Yeong-mok (Outside Director): b. 1956, former branch manager at Kyongnam Bank. Appointed March 2023 — regional finance network.

The company runs a single full-time auditor (Hwang Sang-sun, former Kyongnam Bank branch manager, reappointed December 2023) instead of an audit committee.

2.3 Subsidiaries — a three-arm formation that hedges cycles

Inhwa Precision — Shipbuilding

Marine engine parts (cylinder cover/frame, bed plate). 85.86% of consolidated revenue.

Haedong Industries — Machinery

Gimhae. Metal forming machines — dry-drawing machines etc. Acquired 2012.

Samhwan General Machinery — Plant

Changwon. Heat exchangers / pressure vessels / HRSG for power plants. Partners with Doosan Enerbility and other EPCs.

Interpretation: The "shipbuilding–machinery–plant" three-arm formation cushions corporate survival during a single-sector downturn — evidence management consciously addresses concentration risk.

3. Segment-level analysis

3.1 Marine engine parts — dominant cash cow (85.86% of revenue)

The flagship segment. Inhwa specializes in large metal-machined and fabricated parts that form the case and skeleton of marine engines.

3.1.1 Key products and technical character

- Cylinder Cover: sits at the top of the combustion chamber, withstands explosion pressure and extreme heat. Accounts for ~26.4% of revenue.

- Cylinder Frame: a large casting that supports upper/lower engine and serves as the coolant channel.

- Bed Plate: an outsized structure at the engine base, supporting the crankshaft — requires advanced welding + machining.

- Frame Box: sealed structure between bed plate and cylinder frame, providing the connecting-rod stroke space.

3.1.2 Capacity (CAPA) and utilization (3Q 2025)

| Product | Capacity | Output | Utilization | Reading |

|---|---|---|---|---|

| Cylinder Cover | 19,952 units | 7,650 units | 38.34% | Shift to higher-value mix / line rearrangement — room to run higher |

| Bed Plate | — | — | 62.59% | Solid demand for large welded fabrications |

| Frame Box | — | — | 76.00% | Engine assembly lines busy — super-cycle in motion |

Cylinder cover capacity moved from 22,192 units (2023) to 19,952 units (2025), most likely reflecting old-equipment replacement or a line reconfiguration for larger-spec components — implying room to scale as orders grow.

3.1.3 Raw materials and cost structure

Forged steel, cast steel, cast iron, and steel plate. Recent Chinese steel oversupply has stabilized plate prices, supporting margin. A meaningful portion of materials is supplied free or for fee by engine-maker customers — partially hedging raw-material volatility.

3.2 Metal forming machinery — Haedong Industries (7.26% of revenue)

- Market: sensitive to capex cycles in auto tire (steel cord), construction (wire rope), and electronics (ultrafine wire).

- Tech: top-class domestic wire-drawing machine tech; export track record in Japan and Southeast Asia.

3.3 Metal structures — Samhwan General Machinery (6.88% of revenue)

- AI data centers drive electricity demand, lifting power-equipment capex → expected pickup in heat exchanger / pressure vessel orders.

- Also produces Bogie Frame components for rail vehicles — potential trickle-down from partnerships with Hyundai Rotem (defense / rail).

4. 3Q 2025 financials — a quantum leap

4.1 Results — operating leverage detonates

| Item | 3Q25 | 3Q24 | YoY | Note |

|---|---|---|---|---|

| Revenue | KRW 28.79B | KRW 20.57B | +40.0% | Shipbuilding super-cycle in earnings |

| Operating profit | KRW 4.87B | KRW 1.19B | +309.2% | Operating leverage maximized |

| OPM | 16.9% | 5.8% | +11.1pp | Profitability inflects |

Official fact: Higher-priced orders from 2H 2023–early 2024 are flowing into revenue starting 3Q 2025. The order-to-revenue lead time is 12–18 months for marine-engine parts.

Interpretation: Profit growth 7–8x revenue growth — once revenue clears breakeven in a high-fixed-cost business, incremental margins explode. Stabilized steel plate and FX tailwinds also helped.

4.2 9-month YTD performance & balance sheet

- 9M YTD: revenue ~KRW 82.5B, operating profit KRW 11.9B, net income KRW 13.8B (net > operating = equity-method income / disposal gains).

- Total assets KRW 463.2B, liabilities KRW 131.2B, equity KRW 331.9B, debt-to-equity 39.5% — well below the ~100% manufacturing average.

- Cash & equivalents + short-term financial instruments explain a large share of the ~KRW 434.8B market cap — effectively debt-free.

4.3 Valuation

As of December 2025, market cap ~KRW 434.8B, P/E ~45x, P/B ~1.3x. The headline P/E looks rich, but:

- Earnings recognition lag: Once Hanwha Engine sale gains are booked into FY2024 and FY2025, P/E falls sharply.

- Embedded asset value: Cash + investments make a 1.3x P/B reasonable.

- Sell-side view: Currently digesting a rally — buy zone cited at KRW 35,000–40,000; long-term target upward of KRW 60,000.

5. The crown jewel of capital allocation — the Hanwha Engine deal

The real differentiator is capital allocation. The Hanwha Engine (formerly HSD Engine) trade is a landmark case of a parts maker acting as a sophisticated financial investor.

5.1 Entry, partial exit, and final exit

~KRW 100B

During the shipbuilding downturn, acquired a stake in Hanwha Engine from Socius Well2C Investment — securing supply-chain stability and strategic partnership.

~KRW 137.4B

Hanwha Group's acquisition of Daewoo Shipbuilding (now Hanwha Ocean) led to engine-business vertical integration → partial sale to Hanwha Impact. Already exceeded principal at this point.

~KRW 121.2B

Decision disclosed to dispose of remaining 5.3M shares via block deal. Cumulative recovery ~KRW 250B+.

5.2 What happens to the ~KRW 250B

- Stronger shareholder returns: A record-date filing for an interim dividend was disclosed in August 2025. Already cancelled ~380K treasury shares in July 2025 — expect a special dividend and structural payout uplift.

- New growth via M&A: Targets likely include robotics, defense, aerospace — areas needing precision machining — or smart-yard automation companies.

- Balance-sheet fortress: Some debt paydown could push interest expense to near zero, making the balance sheet shock-proof.

6. Industry environment & risk checks

6.1 Sustainability of the super-cycle

Korean shipyard docks are effectively full through 2027. Koreans are pursuing a profit-oriented selective ordering strategy, which lifts ship prices that pass through to component ASPs. IMO-driven replacement demand looks set to persist through 2030.

6.2 Lead-time effect — high revenue visibility

Order-to-revenue lead time of 12–18 months means 2023–2024 orders flow predictably into 2025–2026 revenue — giving Inhwa strong earnings visibility.

6.3 Risks — US litigation + raw-material volatility

Official fact: Inhwa Precision and Haedong Industries lost the first-instance ruling in a Georgia product-liability lawsuit (Christina Michelle case) — judgment amount ~USD 25.7M (~KRW 35B). The company believes enforceability in Korea is uncertain.

Interpretation: Absorbable given cash on hand, but reputational risk and a contingent-liability discount remain — this is one source of multiple compression today. Raw-material monitoring (steel plate, structural steel) is also warranted.

7. Conclusion & outlook

Inhwa Precision combines "structural growth in the core business" with "successful exit on the strategic investment" — a rare double moment.

- Earnings outlook: FY2025 revenue likely to top KRW 100B with double-digit OPM stable. Earnings rise sustainably through 2026 as the backlog rolls through.

- Valuation re-rating: As the use of Hanwha Engine proceeds (shareholder returns / new business) becomes visible, the market should re-rate Inhwa from a "parts vendor" into a "capital-efficient quality manufacturer".

- Overall view: Among the most undervalued asset-rich + earnings-active names in marine equipment. With cash-heavy balance sheet absorbing the US-litigation overhang, downside support is robust. A longer-duration approach focused on 2026 earnings momentum and the use of cash is appropriate.

Disclaimer: this report is a personal study note based on publicly available information; it cannot be cited as evidence of legal responsibility for any investment decision. Always consult the latest disclosures and qualified advisors before investing.

Sources

- Naver blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224122667361

- Shipyard competitive intelligence: Google Drive

- Marine engine competitive analysis: Google Drive

- "Inhwa Precision diversifies via Haedong acquisition" — Newspim: article

- Inhwa Precision Sept-2025 confirmed earnings disclosure — Toss Invest: disclosure

- Shipbuilding-equipment theme strong, Inhwa +13.74%, Hanwha Engine +7.96% — StockPlus: article

- Inhwa Precision Investment Analysis 2025.12.24 — Judal: report