DEEP RESEARCH · TK Corporation

TK Corporation: the pipe-fitting leader connecting the energy-infrastructure supercycle

A review of industrial pipe fittings, vendor-list moats, and delayed shipbuilding and plant demand

0. Bottom line first

The way I read TK Corporation is through three lenses: fitting know-how accumulated since 1965, global oil-major vendor approvals, and the 12-18 month lag from shipbuilding and plant orders to equipment revenue.

Official fact: TK began as Taekwang Bend Industrial in May 1965, incorporated in 1982, and listed on KOSDAQ in September 1994. Its headquarters are at 117-12 Noksansaneop-daero, Gangseo-gu, Busan, with Hwajeon plants 2 and 3 nearby.

Interpretation: This is not just a steel processor. It supplies safety-critical components for power plants, petrochemical plants, refineries, gas facilities, nuclear plants, desalination, shipbuilding, and offshore structures.

45.02%

Daeshin International owns 27.30%; related-party ownership totals 45.02%.

50,000 tons

The large hydraulic press supports oversized seamless elbows and tees.

10.39%

Consolidated debt ratio at end-Q3 2025, close to a net-cash posture.

1. Business and product role

TK's core product is the butt-weld pipe fitting. The main families are elbows that change piping direction, tees that branch or merge flows, reducers that connect different diameters and control flow or pressure, and caps that close pipe ends.

Official fact: Materials include carbon steel, stainless steel, alloy steel, and non-ferrous metals. As of Q3 2025, stainless and alloy-steel products accounted for about 44.5% of sales.

Interpretation: LNG at minus 163 degrees Celsius and high-temperature, high-pressure nuclear or plant environments need special materials and quality certifications. A higher special-material mix supports pricing and margin defense.

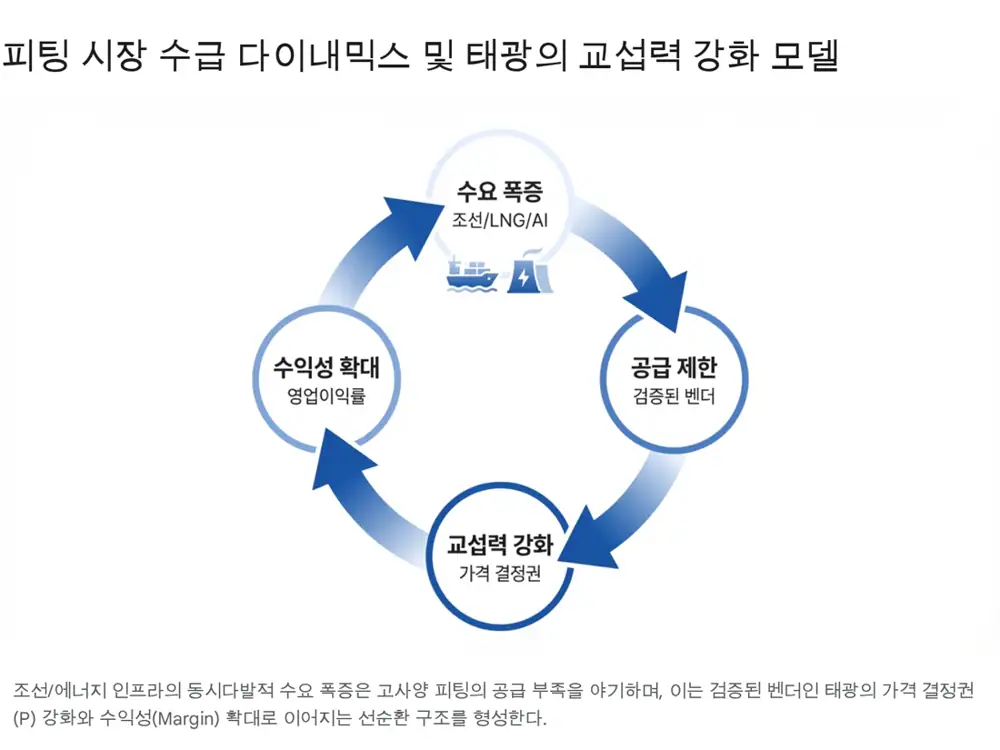

2. Three moats: relationships, technology, policy

The first moat is relationships. In plant equipment, the approved manufacturer list is a real barrier. TK has maintained approvals from global oil majors including Aramco, ExxonMobil, BP, Total, and Shell. Aramco 9COM inclusion directly matters for Middle East project tenders.

The second moat is technology. Certifications such as ASME N-Stamp, ISO 9001, API, DNV, LR, ABS, and KR require years of quality data and QC discipline. The 50,000-ton hydraulic press underpins oversized seamless products that are difficult for peers to match.

The third moat is policy. After the Russia-Ukraine war, energy-security demand supported LNG terminals and LNG carriers, while the nuclear renaissance and SMR development create opportunities for Q-Class nuclear fittings.

AML

EPCs and oil majors tend to stay with qualified vendors, creating lock-in.

Q-Class

Nuclear, LNG, and deepwater projects require advanced metallurgy and heat treatment.

LNG·SMR

Energy security and decarbonization support premium fitting demand.

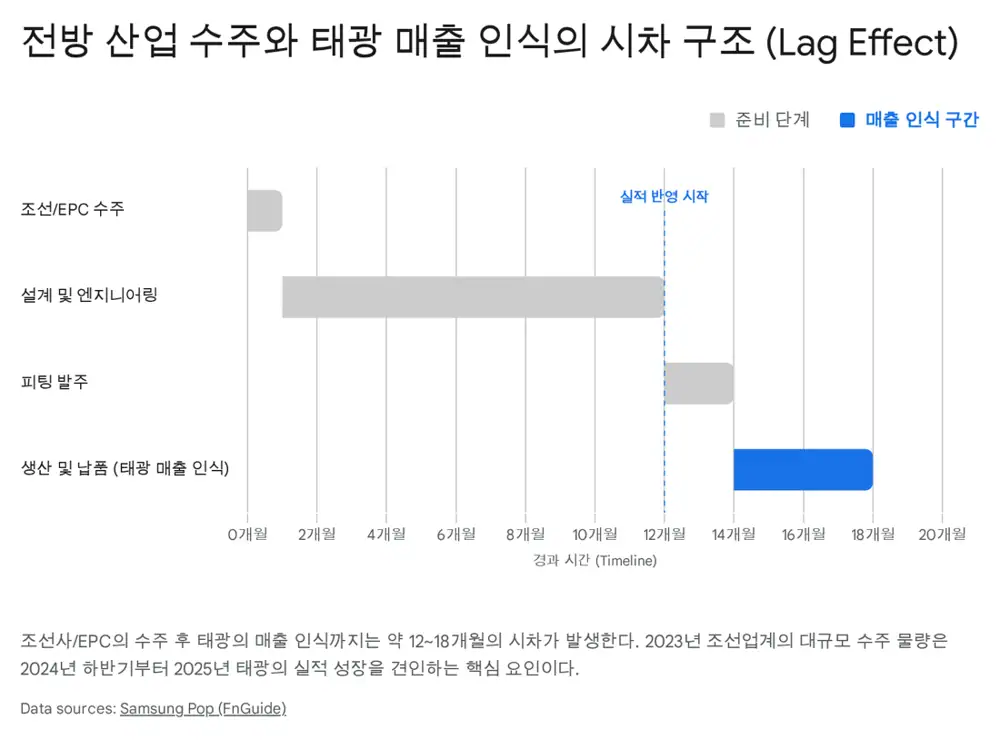

3. Order lag and production capacity

Official fact: After a shipyard or EPC wins a project, detailed engineering, procurement planning, and the purchase order to TK usually take 6 months to 1 year. Raw-material procurement, production, inspection, packing, delivery, and revenue recognition then take another 3-6 months.

Interpretation: The lead time from front-end order strength to TK's reported revenue is at least 12-18 months. Korean shipyard LNG and container-ship orders in 2022-2023, plus Middle East plant recovery from 2023, should be watched as they move into equipment procurement in late 2024-2025.

| Item | Number or detail | Investment read |

|---|---|---|

| Inventories | KRW 141.5bn in Q3 2025 | About 15% above KRW 123.1bn at end-2023, a possible preparation signal |

| Capacity | About 60,000 tons per year | Hwajeon expansion provides room for supercycle volumes |

| Export ratio | About 82.3% in Q3 2025 | Busan port and the Noksan/Hwajeon cluster matter for logistics |

4. Subsidiaries and financial safety net

HYTC is a secondary-battery equipment module and precision-parts company in which TK acquired a 50.81% stake in 2021. It produces slitting molds, knife units, and mandrels, serves battery cell makers including Samsung SDI and LG Energy Solution, and has expanded sites in Poland, China, the United States, and Indonesia.

Foundry Seoul is a real-estate leasing and exhibition subsidiary that owns high-value property in Hannam-dong, Yongsan-gu, Seoul. Tenants such as Gucci Gaok provide rental cash flow separate from manufacturing cycles.

Official fact: Q3 2025 consolidated revenue was KRW 216.4bn and operating profit was KRW 26.6bn. The end-Q3 2025 consolidated debt ratio was 10.39%.

Interpretation: Standalone CAPEX appears focused on maintenance, automation upgrades, and bottleneck removal rather than new mega-factories. If major asset investment is already done, incremental sales can flow through as operating leverage.

5. Risks and checkpoints

- A sharp oil-price drop or global slowdown can delay plant and shipbuilding orders.

- Nickel, molybdenum, and other raw-material prices can move margins.

- HYTC's overseas CAPEX in Poland, Ohio and Tennessee, Indonesia, and Nanjing can strengthen the supply chain over time but may burden near-term earnings.

- The indicators I would keep watching are backlog, inventory quality, stainless/alloy mix, export ratio, and debt ratio.