DEEP RESEARCH · Hanla IMS

Hanla IMS (092460.KQ): A Marine Solutions Company Combining Manufacturing and Service

Analysis of a shipbuilding-equipment company expanding from level measurement and valve control into MRO and green retrofits

0. Bottom line first

The core question is whether Hanla IMS can be re-rated from a traditional equipment maker into an integrated marine-industry solutions company. The source combines its level-measurement and valve-control moat, regulatory upside from BWTS, AMPS, and green fuel systems, and MRO expansion through Gwangyang and Yeongdo yards.

IMO 2013 / USCG 2019

The source says EcoGuardian BWTS received IMO final approval and USCG type approval.

36+ years

Since its 1989 founding, the company has maintained long relationships with HD Hyundai Heavy, Hanwha Ocean, and Samsung Heavy.

About KRW 52bn

The amount invested in the 2020-2021 acquisition of the Orient Shipyard Gwangyang site, interpreted as a strategic service expansion.

1. Economic moat: technology, relationships, policy

Official fact: The source states that Hanla IMS’s EcoGuardian ballast-water treatment system received IMO final approval in 2013 and USCG type approval in 2019, and that its level monitoring system was selected as a World Class Product by Korea’s Ministry of Trade, Industry and Energy in 2014. It also cites more than 70 patents.

Interpretation: In marine equipment, certification and class approval are entry barriers. Conservative purchasing by yards and shipowners, long-term Maker List effects, and tightening environmental regulation make entry hard for latecomers.

2. Value chain and revenue lag

| Stage | Content |

|---|---|

| Upstream | Procures SUS304/316L, castings, sensors, PCBs, and copper, managing costs through annual contracts and supplier diversification. |

| Midstream | Busan facilities manufacture and integrate sensors, housings, PCBs, and the HX-CONTROL integrated control system. |

| Downstream | Systems are installed during outfitting, followed by A/S and replacement-parts demand across the vessel lifecycle. |

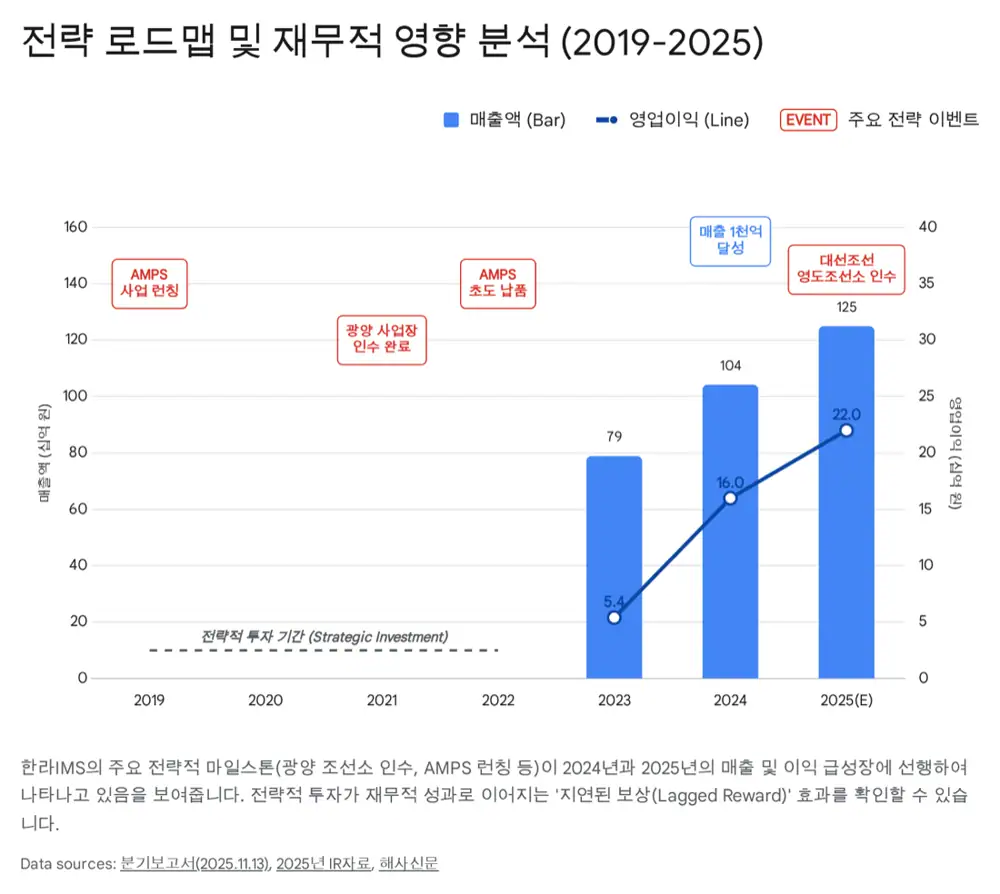

Official fact: The source explains that shipbuilding usually takes 2-3 years from order to delivery; equipment orders arrive about 6 months to 1 year after ship orders, while delivery happens about 1.5-2 years after the yard’s order.

Interpretation: Orders won by global shipyards in the 2022-2023 supercycle begin to appear in equipment revenue from 2025.

3. Production bases and service expansion

R&D and high-tech manufacturing

The headquarters and Plants 1-3 produce level monitoring, valve remote-control, and electronic-control core modules. The third plant completed in 2019 expanded capacity.

Large service hub

Acquired in 2021, it has a 500-meter quay and a 7,000 TLC floating dock that began full operation in 2024.

Urban repair yard

The Daesun Shipbuilding Yeongdo yard acquisition gives access to Busan North Port and the medium-vessel repair market.

Global outpost

The Jiangsu production entity targets China, the world’s largest shipbuilding market, while supporting price competitiveness.

4. CAPEX and financial implications

- 2018-2019: Land purchase in the Busan Gangseo logistics complex and construction of Plant 3 expanded manufacturing capacity.

- 2020-2021: About KRW 52 billion was invested to acquire the Orient Shipyard Gwangyang site, extending the business from manufacturing into services.

- 2024-2025: Gwangyang floating dock operations and Yeongdo yard acquisition completed the ship-repair footprint.

- 3Q25: Total assets rose to about KRW 230.2 billion, and operating profit increased 70.5% year over year, according to the source.

5. Customers and order portfolio

HD Hyundai Heavy Industries, Samsung Heavy Industries, and Hanwha Ocean are core customers, with Hanla IMS systems installed on high-value vessels such as LNG carriers and ultra-large container ships. Networks with European, Japanese, Chinese, and Southeast Asian owners and yards buffer domestic-cycle volatility.

Interpretation: The order book is improving in quality as low-priced orders are depleted, LNG and green equipment share rises, and repair work can become recurring revenue.

6. Investment view

- The source sees a performance quantum jump as 2022-2023 shipbuilding orders are recognized in 2025 revenue.

- Gwangyang plus Yeongdo repair, AMPS, and BWTS can become new cash cows.

- Technology certifications, customer network, and production infrastructure form the three-part entry barrier.

- The source argues that a PER around 11.8x does not fully reflect the changed business quality and future growth potential.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224122607152

- 아시아경제 CORE 한라IMS 기사: https://core.asiae.co.kr/article/2025072208112988219

- LS증권 Value & Growth PDF: https://drive.google.com/open?id=1Gm9LjtmxUj41ofpzmgS04_nrwBh6l4xC

- 해사신문 영도조선소 인수 기사: http://www.haesanews.com/news/articleView.html?idxno=144074