DEEP RESEARCH · Sejin Heavy Industries

Sejin Heavy Industries: shipbuilding supercycle and the mega-block value chain

A review of deck houses, LPG tanks, the Vietnam hub, and subsidiary integration

0. Bottom line first

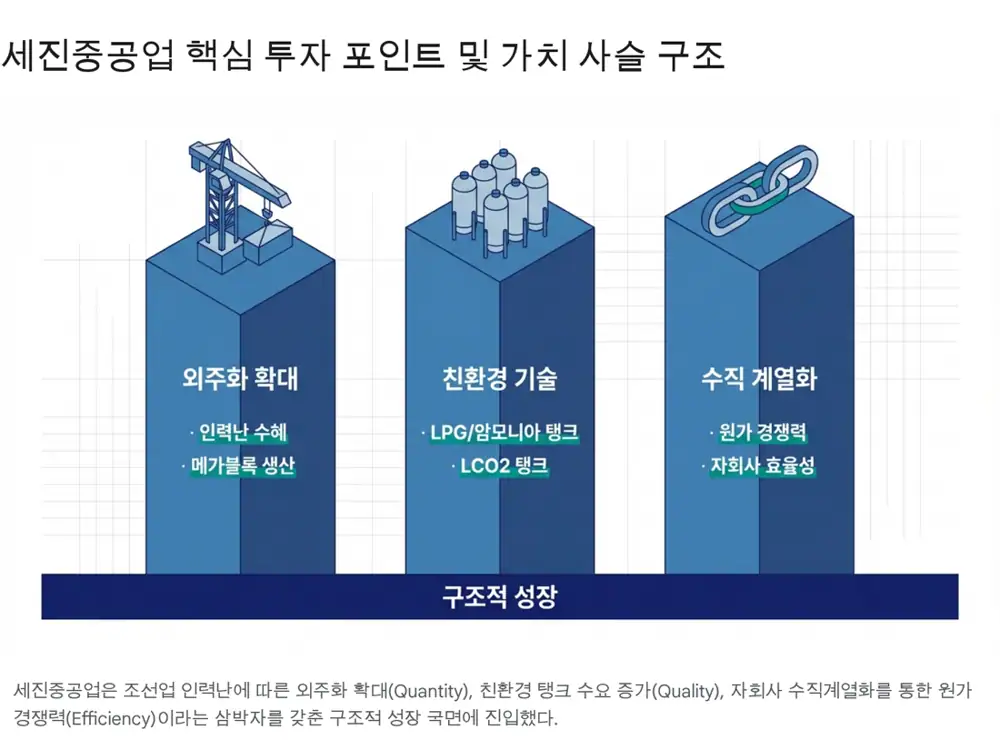

Sejin Heavy functions like an externalized production base that relieves shipyard bottlenecks.

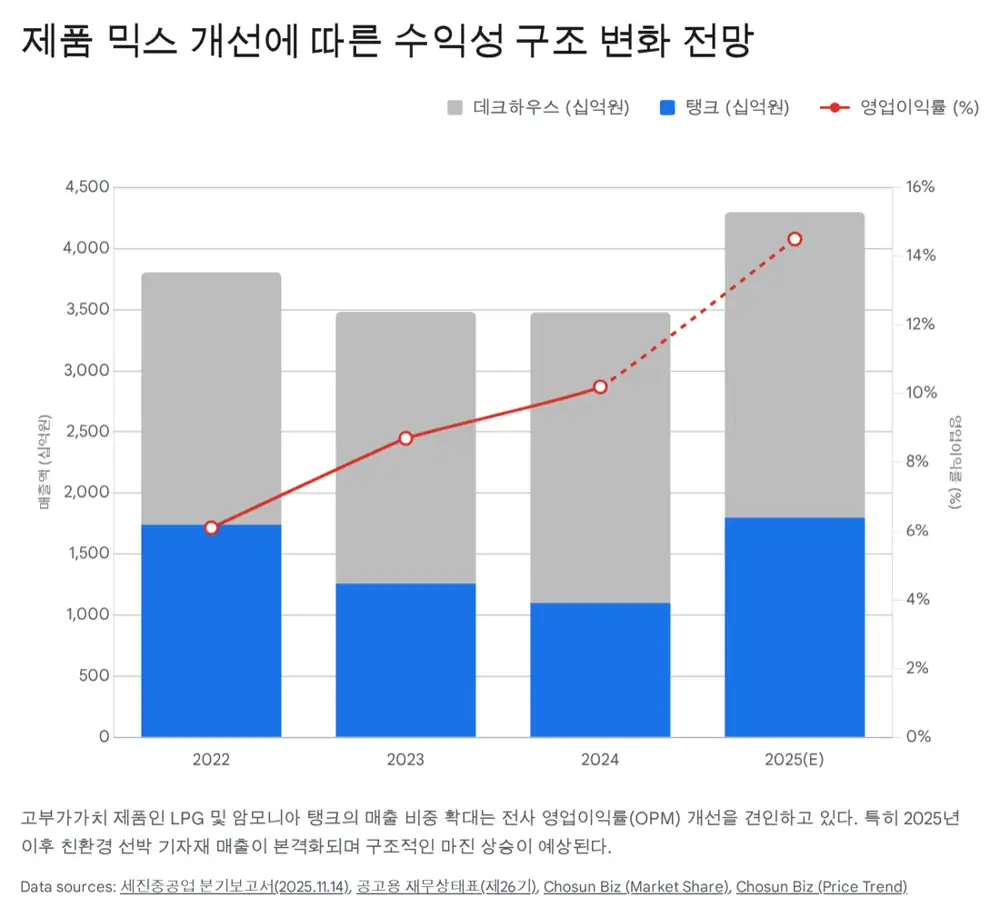

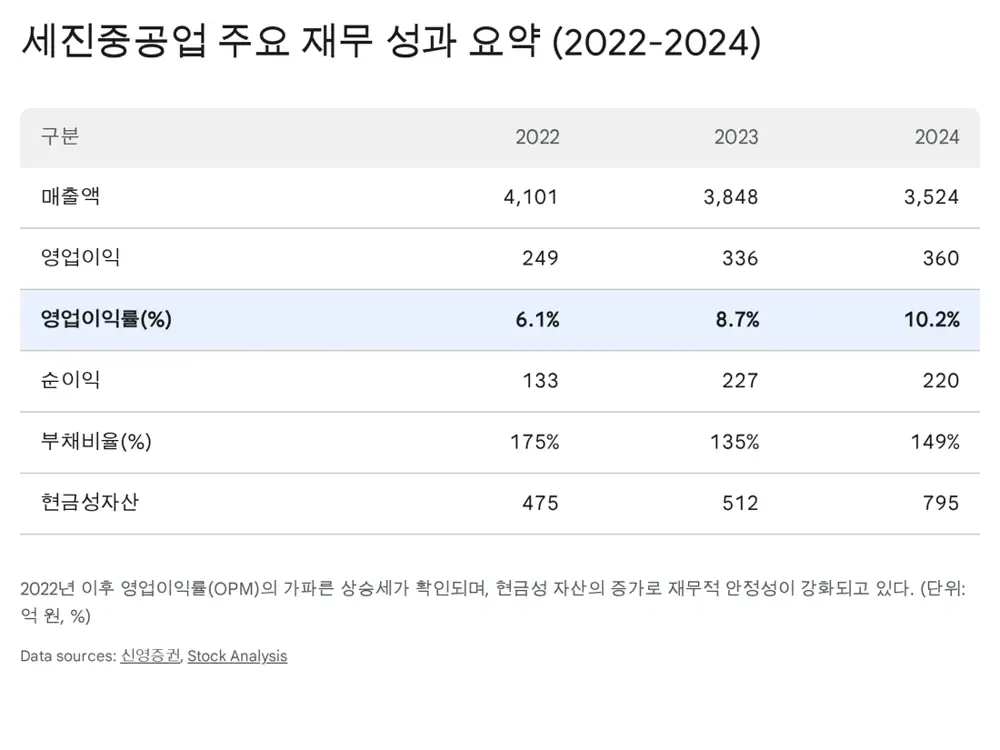

Official fact: 2024 consolidated revenue was KRW 352.4 billion, operating profit was KRW 36.0 billion, and OPM was 10.2%. OPM rose from 0.4% in 2020, 1.5% in 2021, and 6.1% in 2022.

Interpretation: Deck house and LPG tank capability, the long HD Hyundai relationship, and customer diversification are the core.

200,000 pyeong

Large Onsan production site

10.2%

2024 turnaround confirmation

More than 3x

Capacity expansion target

1. Industry and outsourcing

2. Customers and moat

For more than 20 years, Sejin effectively captured deck house and LPG tank orders from HD Hyundai Heavy and HD Hyundai Mipo. Recently it has diversified toward Hanwha Ocean and Samsung Heavy, with potential Chinese yard orders also mentioned in the source.

Official fact: The source cites annual deck house capacity of 100 to more than 130 vessels.

3. Financials

| Item | Number | Read |

|---|---|---|

| 2024 revenue | KRW 352.4bn | Down about 8.4% YoY |

| Operating profit | KRW 36.0bn | 10.2% OPM |

| Total assets | KRW 620.9bn | Large-equipment base |

| Liabilities/equity | KRW 371.5bn / KRW 249.4bn | Debt ratio around 149% |

| Cash | KRW 79.5bn | Up about 56% YoY |

4. Vietnam strategy and risks

In December 2024 Sejin signed a site-entry contract for a new factory in Ninh Thuy Industrial Park, Khanh Hoa, Vietnam. The site is near HD Hyundai Vietnam Shipbuilding, and the source states a goal to more than triple Vietnam capacity. Risks are steel prices, post-2027/2028 peak-out, and early Vietnam stabilization costs.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224122582440

- BusinessKorea: https://www.businesskorea.co.kr/news/articleView.html?idxno=230963

- Sejin Heavy: http://www.sejinheavy.com/eng_sub0_0_1.asp

- 아시아경제: https://cm.asiae.co.kr/article/in-depth/2025090210582437689

- Daum Finance: https://m.finance.daum.net/quotes/A075580/news/stock/20251214165619418

- 해사신문: http://www.haesanews.com/news/articleView.html?idxno=144212

- Inside Vina: https://www.insidevina.com/news/articleView.html?idxno=41890

- 비즈니스포스트: https://www.businesspost.co.kr/BP?command=article_view&num=353743

- Marketin: https://marketin.edaily.co.kr/News/ReadE?newsId=03014326642271912

- ChosunBiz: https://biz.chosun.com/en/en-industry/2025/06/16/5THDCERGZJAXRK2GEQMCQU2BBE/

- 동방선기 보고서: https://drive.google.com/open?id=1BQxp7Vfx57n7471PsvfurIacGPnwDAhCK9lZfepqFqo

- 세진중공업 보고서: https://drive.google.com/open?id=1f89ssaj6KzRflzKFyKy7OkWFNeHoAu_0

- StockAnalysis: https://stockanalysis.com/quote/krx/075580/revenue/

- FMJ Law: http://www.fmjlaw.com/price-escalation-clause-manufacturing-supply-chain/