DEEP RESEARCH · Samyung ENC

Samyung ENC (065570): Governance Collapse and the Paradox of Rehabilitation

A restructuring report on how a marine-electronics specialist reached a 2026 delisting decision point

0. Bottom line first

The core issue is governance, not the product base. The company still has technical assets including roughly 70% domestic share in distress communication equipment, AIS, and radar, plus an agency network in more than 80 countries. But family disputes, outside investment associations, embezzlement and breach-of-duty accusations, and withdrawal from rehabilitation have disrupted the path to normalization.

Marine-electronics moat

GMDSS, AIS, radar, defense HF communication supply records, and type-approval barriers remain key assets.

Governance failure

Family conflict in 2018-2021, minority-shareholder pushback in 2023, and outside association involvement damaged trust.

Delisting risk

The source sees high risk of market exit around April 2026 unless audit issues and capital needs are resolved.

1. Business substance: what remains

Official fact: The source describes Samyung ENC as founded in 1978, a localizer of marine communication equipment, and a company with about 70% domestic share in GMDSS, AIS, and radar-related core equipment.

Interpretation: Civilian products face pressure between Garmin/Furuno at the high end and low-cost Chinese competitors, while naval and coast-guard communication systems and defense MRO remain the last support pillar.

2. Three acts of governance collapse

- 2018-2021: After Chairman Hwang Won stepped back, control disputes involved Hwang Jae-woo, Hwang Hye-kyung, and Lee Sun-ki. Frequent management changes made strategy inconsistent.

- 2023: Minority shareholders criticized unrelated metaverse, crypto, and entertainment initiatives and questioned the use of KRW 20 billion raised through 2022 convertible bonds. The April 2023 extraordinary meeting failed to remove management, but trust was damaged.

- Since 2023: Investment associations including Big Brothers No. 1 and Goldstone No. 1 entered the picture. After Kim Jung-cheol became CEO in February 2024, he accused former CEO Hwang Jae-woo of KRW 24.8 billion embezzlement and breach of duty, while the opposing side challenged board resolutions and sought an injunction.

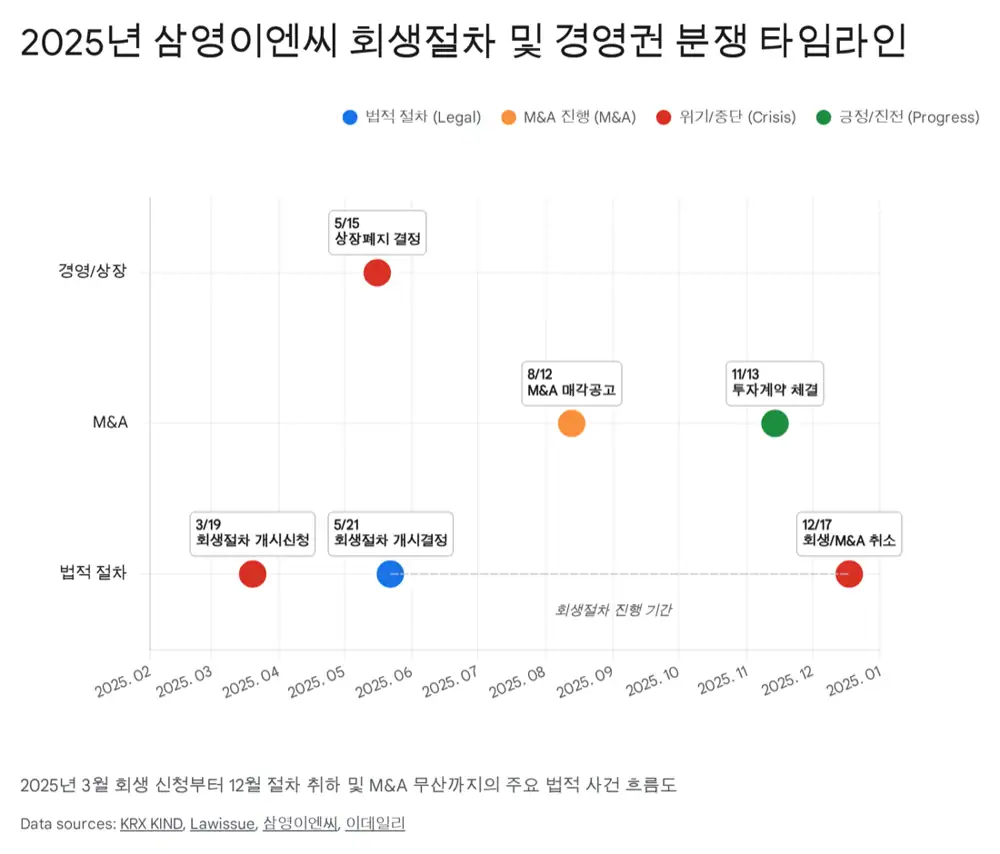

3. 2025 rehabilitation and collapse

Official fact: On March 20, 2025, Samyung ENC applied for rehabilitation proceedings with the Busan Rehabilitation Court. The source frames this as a response to liquidity stress, audit-opinion refusal, and the need for an improvement period from the exchange.

Interpretation: Rehabilitation and stalking-horse M&A offered a possible ordered recovery, but the December 2025 withdrawal and failed M&A reduced the chance of a court-controlled solution.

4. Competition and shareholder structure

| Item | Source content |

|---|---|

| Market shift | IMO GMDSS modernization and e-Navigation move the market from analog to digital. |

| Competitors | Garmin, Furuno, and JRC lead high-end integrated systems, while HD Hyundai Marine Solution and other large players internalize smart-ship solutions. |

| Shareholders | Chairman Hwang’s family about 19.54%, hostile associations such as Goldstone No. 1 more than about 5%, and minority shareholders about 67%. |

5. 2026 scenarios

Workout and renewed third-party sale

- A creditor-led workout could adjust debt and seek a strategic investor interested in defense licenses and the Busan Yeongdo site.

Renewed control dispute

- Without rehabilitation, the Hwang Jae-woo side and Kim Jung-cheol side may return to shareholder meetings and court fights, consuming resources.

Delisting risk

- The source sees high risk because the 2024 audit-opinion refusal issues, including embezzlement and going-concern uncertainty, were unresolved; without major capital injection, April 2026 market exit is viewed as likely.

- Existing shareholders cannot sell while trading is suspended and may face painful restructuring such as capital reduction followed by a paid-in capital increase.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224122572194

- PitchBook company profile: https://pitchbook.com/profiles/company/165172-15

- 삼영이엔씨 리포트 PDF: https://ssl.pstatic.net/imgstock/upload/research/company/1628130808715.pdf

- Marine Electronics Market: https://www.skyquestt.com/report/marine-electronics-market

- 뉴스워커 경영권 분쟁 기사: http://www.newsworker.co.kr/news/articleView.html?idxno=373616

- KRX 회생절차개시신청: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250520000525&rcpno=20250520000372&orgid=F&tran=Y&langTpCd=0

- 로이슈 회생절차 개시 결정: https://www.lawissue.co.kr/view.php?ud=2025052219074531429a8c8bf58f_12

- 마켓인 조건부 투자계약: https://marketin.edaily.co.kr/News/ReadE?newsId=04910166642365720

- 삼영이엔씨 공시정보: https://www.samyungenc.com/kor/view.do?no=103

- Daum 거래정지 공시: https://m.finance.daum.net/quotes/A065570/news/disclosure/20250804065264

- KRX 거래정지 기간변경: https://kind.krx.co.kr/external/2025/04/07/000752/20250407001580/70798.htm

- KRX 반기보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250814003812&docno=&viewerhost=&

- 이데일리TV 기사: https://tvm.edaily.co.kr/News/NewsRead?NewsId=04093446642106928&Kind=

- KRX 정정 사업보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=searchInitInfo&acptNo=20250407001144&docno=

- 세종기업데이터 수주잔고: https://sejongdata.co.kr/archives/69357

- SAR-9 제품 페이지: https://www.samyungenc.com/eng/view.do?no=134&bunryuSeq=13&prdSeq=89&pageIndex=1&pgMode=show

- HD현대중공업 환율 분석: https://drive.google.com/open?id=1Y_lJUKdxKN-FYJ9lby56NGZ06GiUkrNzCIMuRf_DlzQ

- WiseReport 지분현황: https://comp.wisereport.co.kr/company/c1070001.aspx?cmp_cd=065570&cn=

- 이데일리 기사: https://www.edaily.co.kr/News/Read?newsId=04093446642106928&mediaCodeNo=257

- KRX 기타 경영사항: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20251114002421&docno=&viewerhost=&

- 블로터 조건부 투자계약: https://www.bloter.net/news/articleView.html?idxno=647589

- KRX 사업보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20240320001358&rcpno=20240320001112&orgid=F&tran=Y&langTpCd=0

- 이데일리TV 상폐 심의 기사: https://tvm.edaily.co.kr/News/NewsRead?NewsId=02079526642108568&Kind=

- 키움 모바일 공시: https://invest.kiwoom.com/inv/disclosure_detail?date=2025.08.04&seq=00065264&type=02&code=02&keyword=%EC%82%BC%EC%98%81&stockCode=&tp=