DEEP RESEARCH · DAEYANG ELECTRIC

Daeyang Electric: Sensor Re-Rating on Shipbuilding and Defense Cash Cows

A Season II review of marine lighting, special batteries, and MEMS sensors

0. Bottom line first

My conclusion is that Daeyang Electric has entered a possible re-rating phase from a simple shipbuilding-equipment maker into a technology-solution company by adding MEMS sensor growth to shipbuilding and defense cash cows.

Official fact: The source gives 3Q25 cumulative revenue as KRW 156.7bn in the introduction and KRW 156.8bn in the table. Operating profit appears as KRW 18.1bn in the introduction and KRW 19.2bn in the table. The table-based OPM is 12.3%.

Interpretation: The core is not the small rounding difference; it is structural margin improvement. OPM rose from 2.4% in 2023 to 12.3% in cumulative 3Q25, which anchors the re-rating argument.

Marine lighting

IECEx, ATEX, and more than about 2,500 certifications create entry barriers.

Defense and batteries

ICS, WIRAS, and submarine batteries provide secure planned-production cash flow.

MEMS sensors

Localized ESC pressure sensors are the Season II growth engine.

1. Corporate roots and governance

Daeyang Electric began in May 1977 as Daeyang Electric Manufacturing, incorporated in 1988, was designated a defense company in 1990, listed on KOSDAQ in 2011, acquired Korea Special Battery in 2012, and completed the Magok Central R&BD Centre in Seoul in 2022. The source frames this as 48 years of accumulated manufacturing trust.

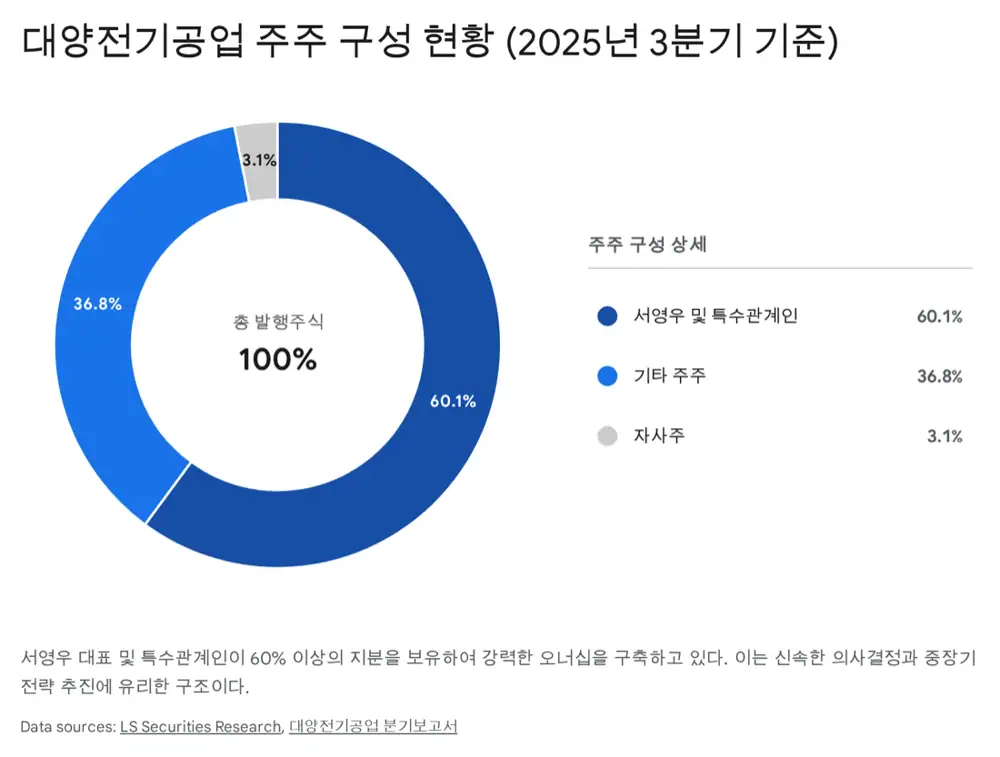

Official fact: As of September 30, 2025, CEO Seo Young-woo owns 5,677,527 shares, or about 59.3%. Including related parties, the controlling shareholder group owns 60.1%. The free float is about 36.8%.

High ownership can support long-term R&D and new-business investment, but it can also create low trading volume and a liquidity discount. The board is described as two inside directors, one outside director, and one full-time auditor. Seo Young-woo holds a master's degree in electronic engineering from Imperial College London, which the source links to technology-led management.

2. Core businesses: shipbuilding, defense, sensors

| Business | Source scale | Core moat | Growth logic |

|---|---|---|---|

| Shipbuilding | 45.5% of 2024 revenue; KRW 65.3bn in cumulative 3Q25 | Explosion-proof lights, IECEx/ATEX, about 2,500 certifications | EEXI/CII rules lift LED and smart-lighting ASP |

| Defense | 30.2% of 2024 revenue; KRW 46.4bn in cumulative 3Q25 | ICS, WIRAS, security requirements, defense standards | Naval communication systems and submarine-battery MRO |

| Sensors | KRW 27.9bn in cumulative 3Q25 | Localized MEMS ESC pressure sensor | Expansion into EV iEB, hydrogen vehicles, and rail |

The shipbuilding segment is the oldest cash cow. Marine lighting must withstand salt, humidity, vibration, electrical compatibility, fire prevention, and explosion-proof requirements, so entry barriers differ sharply from ordinary lighting. Lighting backlog was KRW 60.1bn at the end of 3Q25, and the 1.5-2 year lag from vessel order to equipment delivery supports visibility for the next two to three years.

In defense, integrated communication systems (ICS) and wireless communication systems (WIRAS) are described as key equipment for network-centric warfare. Korea Special Battery, a 100% subsidiary, exclusively supplies lead-acid batteries for Korean Navy submarines, with 3Q25 revenue of KRW 16.9bn. A 6,000m-class unmanned underwater vehicle and mine disposal vehicle connect the company to future naval systems.

3. Sensor business: the core of Season II

The sensor business accelerated after the 2021 Season II declaration. Daeyang applies MEMS technology derived from semiconductor processes to produce automotive pressure sensors. These sensors measure hydraulic pressure in ESC systems and control vehicle posture during hard braking or slipping. Localizing a previously imported sensing element gives the company both cost competitiveness and supply stability.

| Year | Sensor revenue | Meaning |

|---|---|---|

| 2020 | KRW 4.7bn | Early stage |

| 2021 | KRW 9.1bn | Season II starts |

| 2022 | KRW 16.9bn | Customer expansion |

| 2023 | KRW 20.1bn | Continued growth |

| 2024 | KRW 23.6bn | Part of a 37.1% CAGR path |

| Cumulative 3Q25 | KRW 27.9bn | Up 89.4% from KRW 14.8bn a year earlier |

The expansion path is EVs and hydrogen. The source cites electric brake systems (iEB), high- and low-pressure sensors for hydrogen tanks and stacks in fuel-cell vehicles, special sensors and explosion-proof equipment for hydrogen stations and hydrogen transport ships, and cooperation with Japan's HITACHI in rail markets.

4. Financials: operating leverage and near-net-cash structure

| Item | 2023 | 2024 | Cumulative 3Q25 | 2025E |

|---|---|---|---|---|

| Revenue | KRW 154.3bn | KRW 196.3bn | KRW 156.8bn | KRW 233.8bn |

| Operating profit | KRW 3.7bn | KRW 15.7bn | KRW 19.2bn | KRW 25.8bn |

| OPM | 2.4% | 8.0% | 12.3% | 11.0% |

| Net income | KRW 8.4bn | KRW 19.6bn | KRW 18.2bn | KRW 23.7bn |

Official fact: The source says 2024 revenue rose 27.2% year over year, and cumulative 3Q25 revenue rose about 37% year over year. Operating profit rose 324% from KRW 3.7bn in 2023 to KRW 15.7bn in 2024, and cumulative 3Q25 operating profit already exceeded full-year 2024.

The balance sheet is conservative. At the end of 3Q25, assets totaled KRW 319.9bn, liabilities KRW 57.4bn, equity KRW 262.6bn, debt-to-equity was 21.8%, and the current ratio was 367.8%. Cash and cash equivalents of KRW 38.1bn plus short-term financial assets exceeded borrowings, creating a near-net-cash structure, and retained earnings of KRW 226.7bn imply dividend capacity.

On cash flow, cumulative 3Q25 operating cash flow was an inflow of KRW 3.37bn. It was lower than net income of KRW 18.2bn because working capital increased through receivables and inventory, which the source interprets as natural during rapid revenue growth.

5. R&D, risks, and valuation

Daeyang keeps R&D spending at around 3-4% of revenue. Cumulative 3Q25 R&D was about KRW 4.7bn, or 3.0% of revenue. The Magok Central R&BD Centre, completed in February 2022, researches sensors, unmanned underwater vehicles, and next-generation communication systems. The source also emphasizes 25-30% annual headcount growth for sensor specialists.

- End-market cyclicality: shipbuilding orders can fall during global downturns or oil-price weakness, although the current supercycle is tied to replacement demand from environmental regulation.

- Raw-material risk: 3Q25 raw-material purchases were KRW 96.7bn, with exposure to copper, aluminum, semiconductor devices, imports, and FX.

- Liquidity risk: high insider ownership means fewer freely traded shares, which can lead to low volume and higher price volatility.

Official fact: The source gives 2025E PER at about 12.2x and PBR at 1.1x. It argues the company is still trapped in shipbuilding-equipment valuation despite Korean defense peers trading at 20-30x PER and automotive sensor/electronics peers at 15-20x.

Interpretation: The most important re-rating variable is sensor revenue share. The source expects sensor revenue share to expand from 12% in 2024 to 21.8% in 2027, arguing that rising sensor profit contribution could justify a tech-component multiple above 15x PER rather than a ship-equipment multiple around 10x.

6. My conclusion

Daeyang Electric is a company where sensor growth is beginning to run on top of stable shipbuilding and defense demand. A near-net-cash balance sheet, high ownership, an R&D center, and sensor hiring all fit the longer Season II strategy.

Rather than treating the source's strong-buy framing as a direct recommendation, I would verify sustained sensor revenue growth, conversion of shipbuilding backlog into revenue, stability of defense batteries and communication systems, and the liquidity risk from low free float.

Sources

- 원문 / Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224122545235

- LS증권 Value & Growth 대양전기공업 리포트: https://drive.google.com/open?id=1Gm9LjtmxUj41ofpzmgS04_nrwBh6l4xC

- 뉴스토마토 대양전기공업 자동차용 센서소자 기사: https://www.newstomato.com/ReadNews.aspx?no=280685