DEEP RESEARCH · Dongbang Ship Machinery

Dongbang Ship Machinery: ship-equipment turnaround and environmental-equipment mix shift

A review of PIPE SPOOL stability and environmental-equipment growth

0. Bottom line first

Dongbang is moving from a pipe supplier to a broader equipment company with environmental products.

Official fact: Cumulative Q3 2025 PIPE SPOOL sales were KRW 21.143 billion, 73.3% of sales, while environmental-equipment sales were KRW 6.359 billion, 22.0%. Environmental equipment rose 6.4 percentage points from 15.6% in 2024.

Interpretation: A rising finished-equipment mix is the key to margin improvement.

73.3%

Stable cash generator

22.0%

Higher-margin growth pillar

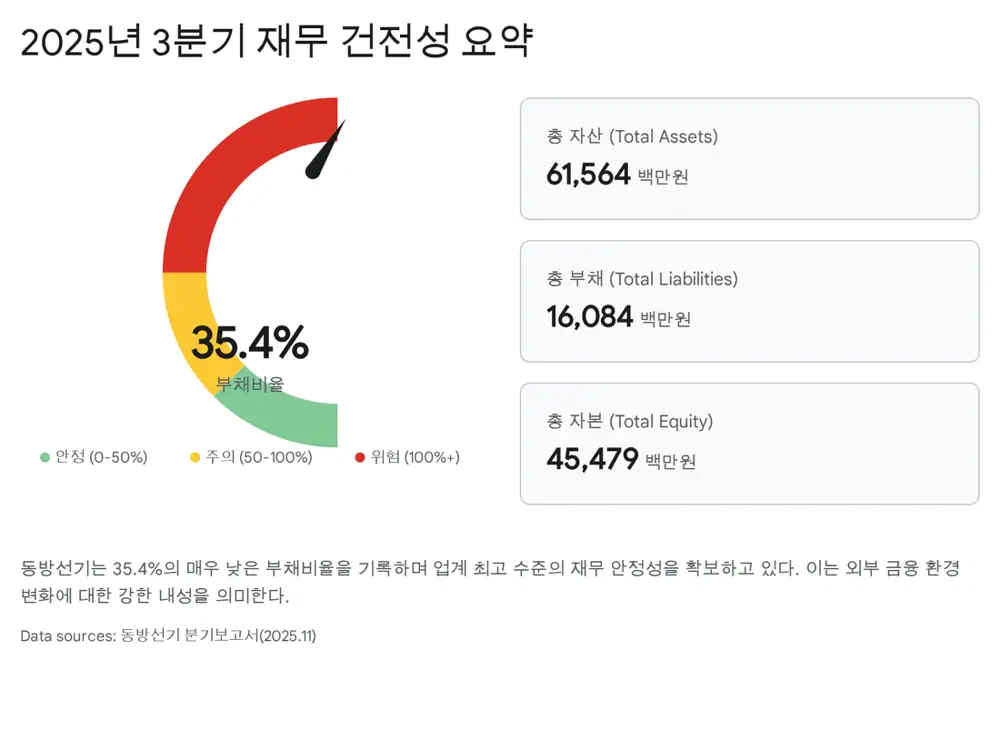

35.4%

Low financial burden

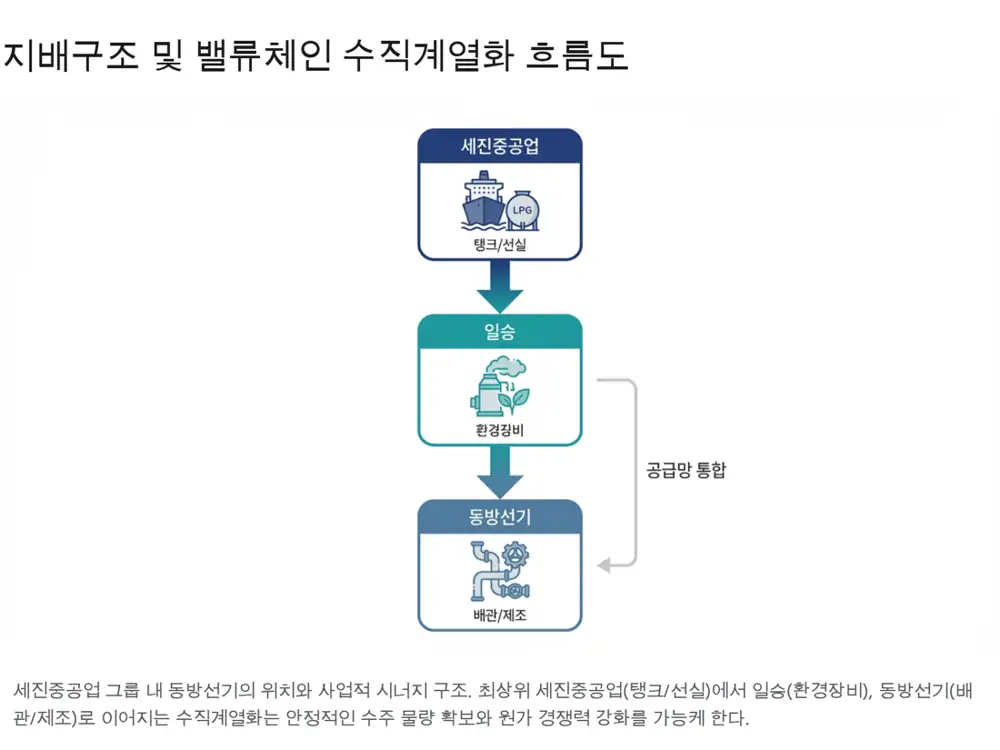

1. Ownership and business

Ilsung owns 20.00%, and Sejin Heavy owns 7.79%. Founded in 1994 and listed on KOSDAQ in 2009, Dongbang supplies major yards including Hyundai Heavy, Samsung Heavy, and Hanwha Ocean.

2. Segment analysis

| Segment | Number | Meaning |

|---|---|---|

| PIPE SPOOL | KRW 21.143bn | Benefits from piping outsourcing |

| Environmental equipment | KRW 6.359bn | STP/FWG mix improvement |

| Utilization | 100,507 EA / 144,000 EA, about 70% | Stable production level |

3. Financials and CAPEX

Liabilities were KRW 16.08482 billion and equity was KRW 45.47968 billion. Q3 2025 tangible-asset investment was KRW 164.76 million: buildings/structures KRW 71.48 million, machinery KRW 52.19 million, vehicles KRW 25.39 million, and other KRW 15.70 million.

4. Industry and risks

The shipbuilding supercycle and IMO regulation support demand for both pipe spools and STP/FWG. Risks are steel prices and shipbuilding dependence, buffered by group purchasing and escalation clauses.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224122538809

- 데일리인베스트: http://www.dailyinvest.kr/news/articleView.html?idxno=43015

- 네이버 리서치 PDF: https://ssl.pstatic.net/imgstock/upload/research/company/1648691299594.pdf

- Uniasen: https://uniasen.com/ko/blog/%ED%8C%8C%EC%9D%B4%ED%94%84-%EC%8A%A4%ED%92%80%EC%9D%B4%EB%9E%80-%EB%AC%B4%EC%97%87%EC%9D%B8%EA%B0%80%EC%9A%94/

- 기후솔루션: https://forourclimate.org/ko/newsroom/1066

- Stock research PDF: https://stock.pstatic.net/stock-research/company/74/20241004_company_736154000.pdf