DEEP RESEARCH · Asterasys

Asterasys: aesthetic-device technology moat and profitability leverage

A review of Liftera, Coolfase, CoolSoniq, FDA approval, and consumables revenue

0. Bottom line first

The key is recurring consumables revenue after the installed base expands, not just device sales.

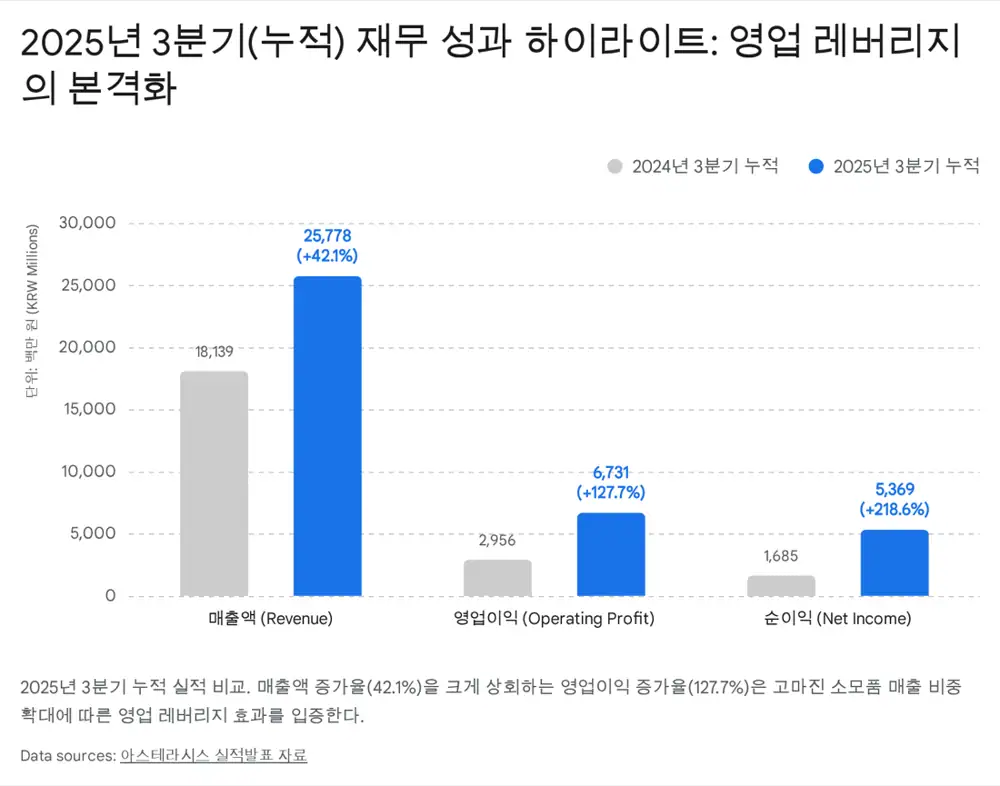

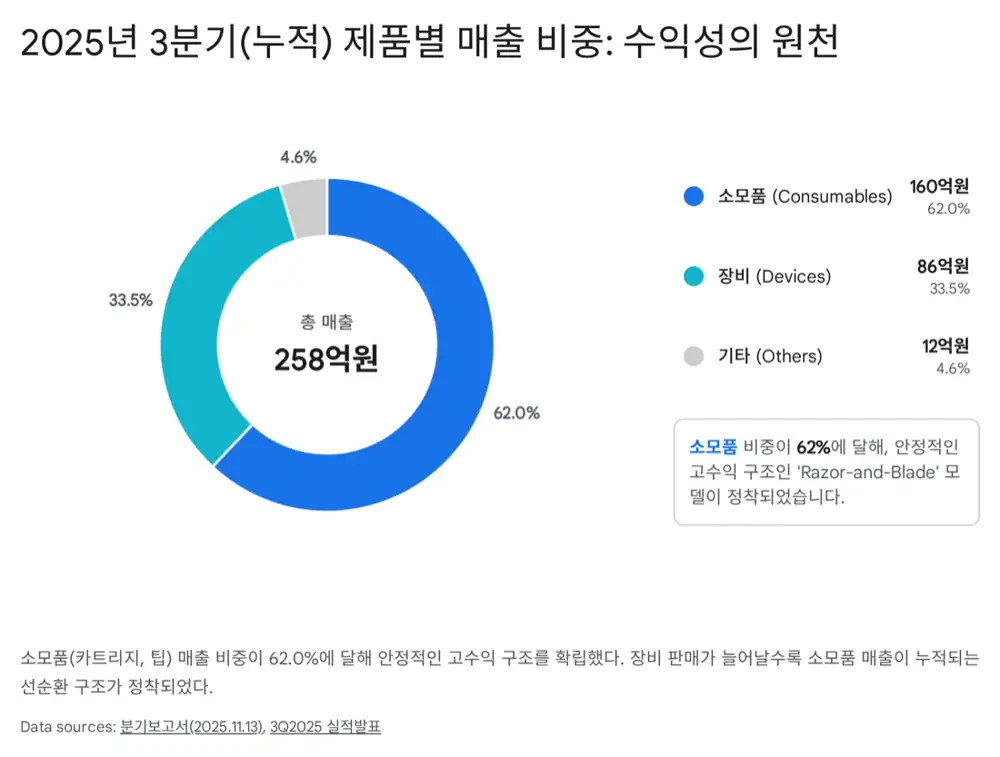

Official fact: The source cites the January 24, 2025 KOSDAQ listing, October 2025 U.S. FDA 510(k) approval for Coolfase, cumulative Q3 2025 revenue of KRW 25.8 billion, up 42.1%, and operating profit of KRW 6.7 billion, up 127.7%. Consumables were about 62.0% of revenue.

Interpretation: High-margin consumables and new-product mix are creating operating leverage.

62.0%

Recurring cartridge and tip sales

KRW 25.8bn

YoY +42.1%

KRW 6.7bn

YoY +127.7%

1. Growth path

Founded in July 2015 as Daehan Biomedical, Asterasys internalized HIFU technology and launched Liftera with the world’s first pen-type applicator. From 2020 to 2024 it secured approvals such as CE, ANVISA, and Russia MOH, and won the USD 7 million Export Tower in 2022.

2. Ownership

As of September 30, 2025, CEO Eun-taek Seo held 34.53%, CTO Jong-seok Kim 6.40%, and CFO In-ho Lee 3.88%. Management ownership aligns incentives with shareholder value.

3. Products and technology

TDT™ delivers ultrasound energy at more than 10Hz to diffuse heat broadly and evenly. CoolSoniq received MFDS approval in February 2025, and Coolfase FDA approval creates a bridgehead into North America.

4. Financials

| Item | Q3 2024 cumulative | Q3 2025 cumulative | YoY |

|---|---|---|---|

| Revenue | 18,139 | 25,778 | +42.1% |

| Cost of sales | 5,267 | 5,616 | +6.6% |

| Gross profit | 12,872 | 20,162 | +56.6% |

| SG&A | 9,916 | 13,431 | +35.5% |

| Operating profit | 2,956 | 6,731 | +127.7% |

| Net income | 1,685 | 5,369 | +218.6% |

| OPM | 16.3% | 26.1% | +9.8%p |

5. Valuation and risks

The source cites about 15-20x 2025E PER for Asterasys, versus Classys at about 25-30x and Viol around 20x. Risks are competition, the speed of revenue conversion after FDA approval, and volatility if expectations are priced in early.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224122397411

- Daum FDA 승인: https://v.daum.net/v/Xt0uueBWOt?f=p

- Investing.com: https://www.investing.com/equities/asterasys-consensus-estimates

- Mordor Intelligence: https://www.mordorintelligence.com/industry-reports/high-intensity-focused-ultrasound-hifu-market

- Precedence Research: https://www.precedenceresearch.com/radiofrequency-based-aesthetic-devices-market

- ChosunBiz: https://biz.chosun.com/stock/market_trend/2025/10/20/BUPQCSXV6VEIBFIFTSLFQNKEDU/