DEEP RESEARCH · SK HYNIX · CAPITAL STRUCTURE

SK Hynix — Answering the KRW 600 trn Bill with an SPC Model

Easing the 100% grandchild-subsidiary rule + permitting financial-leasing creates a Korean version of Intel-Brookfield SCIP — and it is fundamentally different from a battery JV.

0. Bottom line first

If the National Advanced Strategic Industries Act special exception passes, materials/parts/equipment suppliers benefit — but SK Hynix wins by a wide margin. It can raise massive capital with no equity dilution and almost no risk. The two key changes: (1) the mandatory grandchild-subsidiary ownership ratio drops from 100% to 50%, and (2) financial leasing is allowed at the great-grandchild level. Together they legalize an Intel-Brookfield SCIP-style SPC structure in Korea.

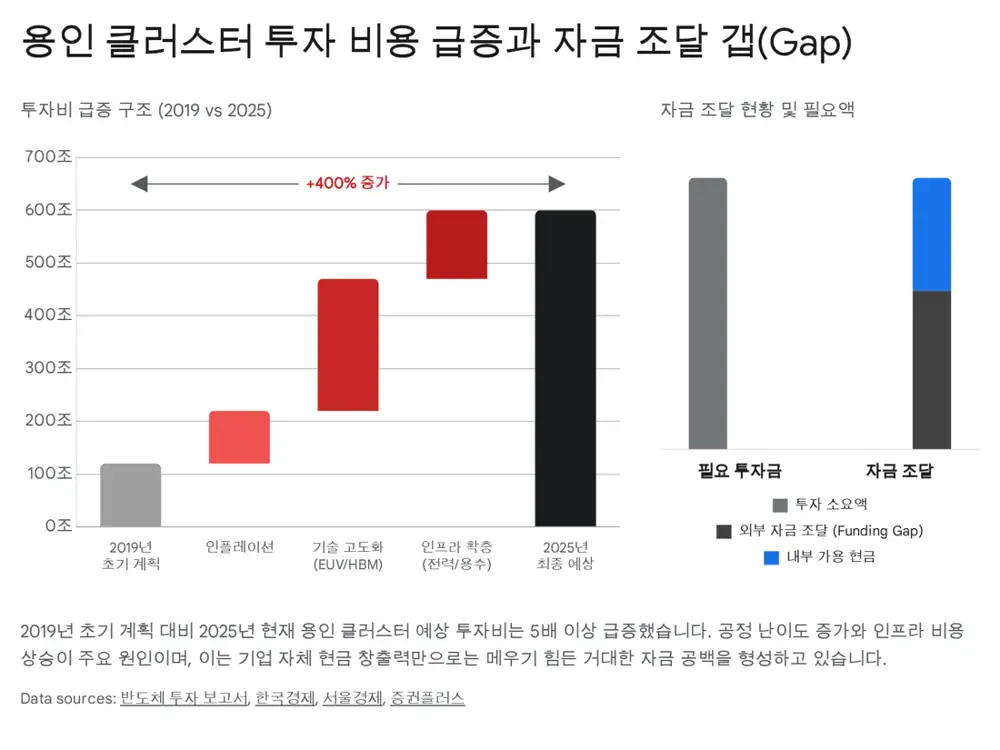

- Why now: Total Yongin cluster capex ballooned from KRW 120 trn (2019 estimate) to over KRW 600 trn — a 5x jump. Internal cash alone cannot fund it.

- Ownership barrier: SK Inc → SK Square → SK Hynix (grandchild) → any new great-grandchild has to be 100%-owned, blocking outside capital.

- Solution: An SPC owned 51% by SK Hynix (control) + 49% by FIs (National Growth Fund, NPS, PEFs) builds the fab and leases it to SK Hynix.

- vs. battery JVs: Battery JVs are a "marriage" (market access + joint operation). The semiconductor SPC is a "lease" (financing + single-operator control).

1. The KRW 600 trn bill — capital intensity explodes

Official fact: What was estimated at ~KRW 120 trn in 2019 for the Yongin semiconductor cluster has ballooned to over KRW 600 trn — a 5x+ jump driven by inflation, the necessity of EUV tooling for sub-10nm 6th-gen (1c) nodes, and the cost of TSV/Advanced Packaging lines for HBM.

In 2025 global semis are well into a "Capital Warfare" era. The AI super-cycle drove HBM demand to vertical, and successive nodes plus advanced packaging now cost exponentially more. Unlike Samsung, SK Hynix has relatively limited cash on hand, so external funding is inevitable — but Korea's holding-company rules under the Fair Trade Act have historically blocked exactly that.

2. The regulatory pivot — the 100% rule cracks

2.1 What the current rule does

SK ownership chain: Chairman Chey → SK Inc. (holdco) → SK Square (subsidiary) → SK Hynix (grandchild). The post-1997 Fair Trade Act forces grandchildren to own any new domestic great-grandchild 100% to curb conglomerate sprawl.

- No JVs: SK Hynix can't give even 1% to materials/equipment partners or fabless players.

- No FIs: Even an SPC for a fab can't take PEF/pension equity → SK Hynix carries the full debt and the credit-rating risk alone.

2.2 The key change: 100% → 50% + financial leasing

Official fact: The "National Advanced Strategic Industries Act" exception and FTC guideline revision do two things: (1) for designated strategic sectors (incl. semis), the grandchild → great-grandchild mandatory ownership ratio is cut from 100% to 50%, and (2) the "separation of finance and industry" doctrine is relaxed at the great-grandchild level to permit financial leasing of semiconductor equipment/fabs.

Interpretation: Together these legalize the Intel-Brookfield SCIP architecture in Korea: an SPC builds the fab, leases it to SK Hynix, and SK Hynix pays rent.

2.3 Safeguards — 5-year review

- Each case requires FTC pre-approval.

- FTC re-review every 5 years on business viability and equity-ratio compliance.

- Tied to regional (non-metro) investment to discourage Seoul-area concentration.

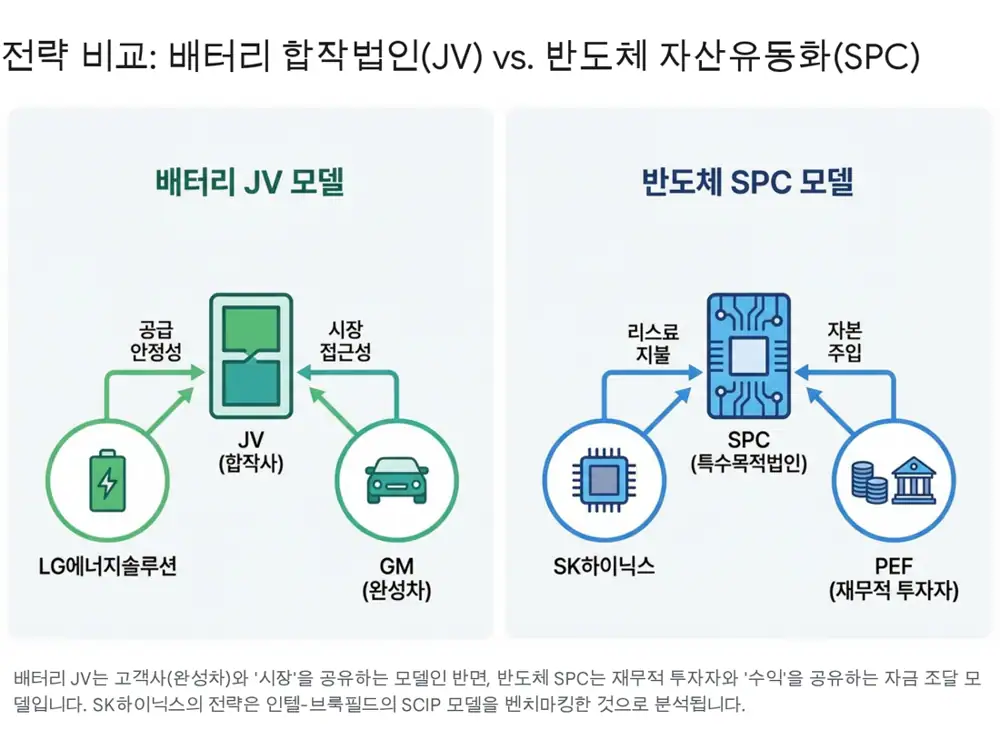

3. Comparison — SPC vs. battery JV

"Is this just like a battery maker setting up a JV plant with an automaker customer?" — No. They look alike on the surface but the purpose, partners, and economics differ fundamentally.

Marry and build a house together

Two parties (battery maker + automaker) pool funds to build a shared home (plant); the food (battery cells) is eaten by the spouse (automaker).

Pay rent to a landlord

The tenant (SK Hynix) has a wealthy landlord (investors) build a custom property (fab), then moves in and pays rent (lease fees). The landlord doesn't live in the house — i.e., no operational involvement.

3.1 Battery JV (LG ES × GM = Ultium Cells, etc.)

- Partner: A Strategic Investor (SI) and Customer.

- Purpose: Captive market access + supply-chain stability + shared IRA subsidy benefits.

- Operations: Both sides send engineers & capital pro rata; profits/losses split by stake.

3.2 SK Hynix SPC (Intel SCIP benchmark)

- Partner: Financial Investors (NPS, PEFs, asset managers). Indifferent to chip tech — they want stable yield (interest/dividends).

- Purpose: Fund massive fab capex off-balance-sheet → protect debt ratio and credit rating.

- Operations: SK Hynix runs the fab 100%. Investors collect only the agreed yield.

3.3 Side-by-side

| Dimension | Battery JV | Semi SPC (SK Hynix model) |

|---|---|---|

| Core purpose | Secure market & stabilize supply | Raise capex funds & manage debt |

| Partner | Automaker (customer) | Pension/PE/AMs (investors) |

| Relationship | Business spouse (marriage) | Landlord & tenant (lease) |

| Profit split | By equity stake | Fixed lease fee + dividends |

| Control | Joint management | SK Hynix alone (investors hands-off) |

| Tech leakage | Possible during co-development | None (full IP control) |

4. Intel's SCIP — a deeper look at the blueprint

The clearest reference is the 2022 Intel × Brookfield Semiconductor Co-Investment Program (SCIP).

4.1 Deal structure

Official fact: Intel built 2 fabs in Chandler, Arizona at a total cost of USD 30 bn (~KRW 40 trn), in an SPC owned Intel 51% / Brookfield 49% — keeping Intel in operational control and consolidating the SPC. Capital was contributed 51:49 — Brookfield funded ~USD 15 bn.

- Cash flows: Once running, Intel takes 100% of wafers and pays a usage fee back to the SPC (the dividend source). Brookfield is reported to earn a yield in the ~4%–8.5% range.

4.2 Financial effect — "debt-free funding"

Interpretation: Had Intel raised USD 15 bn as debt, leverage and credit risk would have spiked. Equity-style funding avoids that. SK Hynix wants the same effect — and if half of the KRW 600 trn comes via this channel, that's roughly KRW 300 trn sourced externally without touching the debt ratio.

5. What comes next — capital flows and shareholder relations

5.1 Investor mix — the "National Growth Fund" arrives

Official fact: Korea's FSC is creating a KRW 150 trn "National Growth Fund" over the next 5 years from 2025, funneling capital into strategic sectors. Semiconductors alone are allocated KRW 4.2 trn in 2026.

- Senior tranche: Commercial banks, insurers — low yield, near principal-protected.

- Mezzanine/junior tranche: National Growth Fund, NPS, PEFs — accept risk for higher dividends. Public capital sits junior to absorb first losses.

- Citizen fund: A KRW 600 bn retail-accessible vehicle so individuals can share in semiconductor-industry returns.

5.2 Shareholder dynamics — "income share" vs. "expense pass-through"

For SK Hynix shareholders

- Pros: No massive rights issue → no dilution. Construction risk shared with outsiders.

- Cons: Fab profits aren't fully captured — lease (or preferred dividend) flows back to the SPC. In booms it looks like "profit leakage"; in busts the fixed lease becomes operating-leverage-amplifying overhead.

For SPC investors

- Financial partner, not operator. Tied to SK Hynix as "landlord / tenant" + holders of 49% of the SPC.

- Exit: Mostly through dividends; after 10–20 years, likely SK Hynix call option and/or investor put option.

5.3 The "fin-industry boundary" debate and oversight

- Critics (socialized losses): If it works, SK pockets the upside; if it fails, NPS/policy funds (i.e., taxpayers) absorb losses. Risk that the SPC becomes a channel for funneling work to in-house SK affiliates (SK E&C, etc.).

- Guardrails: FTC pre-approval + 5-year reviews; financial leasing is the only permitted financial activity. SK Hynix's official line: "The SPC is not a financial products vehicle — it's a single-purpose entity for building a fab."

5.4 Expected SPC structure (based on Intel)

| Item | Detail | Note |

|---|---|---|

| SPC name (tentative) | Yongin Infrastructure Investment Co. | SK Hynix's great-grandchild |

| Ownership | SK Hynix 51% (control) / external 49% (capital) | FTC exception (100% → 50%) |

| Outside investors | National Growth Fund, NPS, global PEFs, infra funds | Stable long-yield capital |

| Use of proceeds | Yongin cluster fab/cleanroom construction & equipment | ~KRW 120–600 trn order of magnitude |

| Revenue model | Lease fees paid by SK Hynix | Volume-linked or fixed |

| Risk sharing | Cost overruns/start-up delays split by stake | Intel-Brookfield reference |

| Exit | SK Hynix call option after 10–20 yrs | Aligned to fab depreciation horizon |

6. Conclusion — a Korean-style semiconductor finance model is born

For SK Hynix, this is "rain after a drought" — the only realistic way to clear a KRW 600 trn capex hurdle.

- Evolution of investment: From "earn-then-build" to "build with others' money and lease." Not like battery JVs ("share customers and markets") — it's a higher-finance version that "shares the capital burden with financial investors."

- Shareholder relationship: Future investors are not "business partners" but "premium landlords" or "long-dated creditors." They focus on SK Hynix's ability to pay the lease (credit) more than chip-cycle home runs.

- National mandate: Because pension money and tax dollars are flowing in, transparent governance and fair profit-sharing must come first. Ongoing oversight and stronger guardrails are required.

Ultimately this is the compromise Korea has struck between "speed to secure tech sovereignty" and "fairness via anti-concentration" — an unavoidable survival strategy in the global chip war.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224122269432

- Hankyung — SK Hynix: outside capital is essential for 600 trn investment: https://www.hankyung.com/article/2025122438761

- Seoul Economic Daily — SK Hynix on strategic-industry deregulation: https://sedaily.com/NewsView/2H1USXMNDC

- The Elec — "600 trn capex: old model has limits": https://www.thelec.kr/news/articleView.html?idxno=50201

- Chosun — Easing holding-company rules for chips: https://www.chosun.com/economy/economy_general/2025/12/12/24YGWWLNTNA77HIEXMBKB72BAA/

- Yonhap Infomax — FTC 50% rule briefing: https://news.einfomax.co.kr/news/articleView.html?idxno=4389815

- Dong-A Ilbo (EN) — Korea to ease ownership rules: https://www.donga.com/en/article/all/20251212/6008065/1

- Yonhap News — SK Hynix calls reform a "golden-time" measure: https://www.yna.co.kr/view/AKR20251224089300003

- ChosunBiz EN — Government eases finance-industry split: https://biz.chosun.com/en/en-policy/2025/12/11/S35SJ6V6Z5BRBL7PUHFO7EOEDM/

- Edaily — 5-yr FTC re-review for the exception: https://marketin.edaily.co.kr/News/ReadE?newsId=04237766642400160

- Intel Newsroom — SCIP PDF: https://download.intel.com/newsroom/archive/2025/en-us-2022-08-23-intel-introduces-firstofitskind-semiconductor-coinvestment-program.pdf

- Intel IR — Smart Capital announcement: https://www.intc.com/news-events/press-releases/detail/1568/intel-advances-smart-capital-introduces-first-of-its-kind

- Brookfield Press — Definitive agreement with Intel: https://bip.brookfield.com/press-releases/bip/brookfield-infrastructure-signs-definitive-agreement-intel

- S&P Global — Intel-Apollo JV rating: https://www.spglobal.com/ratings/en/regulatory/article/-/view/type/HTML/id/3191329

- Data Center Knowledge — bankers looking for similar deals: https://www.datacenterknowledge.com/data-center-chips/intel-s-planned-us-chip-plant-has-bankers-looking-for-similar-deals

- Yonhap — 150 trn National Growth Fund, 1st projects: https://www.yna.co.kr/view/AKR20251219089300002

- G-enews — National Growth Fund / semis: https://www.g-enews.com/article/Finance/2025/12/202512191539323683a6e8311f64_1

- Business Korea — Fund to invest 30 trn next year: https://www.businesskorea.co.kr/news/articleView.html?idxno=258942

- Munhwa Ilbo — 150 trn seed fund 10 Q&As: https://www.munhwa.com/article/11556058

- Investing.com KR — SK Hynix public statement: https://kr.investing.com/news/economy-news/article-1766386

- Daum video — SK Hynix unusual public statement: https://v.daum.net/v/20251224173208624

- Intel 8-K (08/23/2022): https://www.intc.com/filings-reports/all-sec-filings/content/0001193125-22-226986/0001193125-22-226986.pdf

- MK EN — SK Hynix vs LG Energy Solution context: https://www.mk.co.kr/en/stock/11005774

- Jones Day — LG-SK Battery patent resolution: https://www.jonesday.com/en/practices/experience/2021/06/sk-innovation-resolves-global-patent-dispute-with-lg-chem--lg-energy-solution-over-lithiumion-battery-technology

- Business Wire — LG-SK settlement: https://www.businesswire.com/news/home/20210411005029/en/LG-Energy-Solution-and-SK-Innovation-Reach-Agreement-to-End-USITC-Trade-Secret-Dispute-and-End-Litigation

- Butzel Long — Trade secret dispute takeaways: https://www.butzel.com/alert-Takeaways-from-the-Resolution-of-a-Trade-Secret-Dispute-Competitors-Resolve-Battery-Technology-Trade-Secret-Dispute-After-ITC-Ruling

- Stockplus newsroom — 600 trn cluster needs outside capital: https://newsroom.stockplus.com/breaking-news/5597