DEEP RESEARCH · GLOBAL SHIPBUILDERS

Global Shipbuilding Power Struggle: Country-Level Competition and Korea’s Survival Strategy

A translated competitive map covering China, Japan, Korean mid-tier yards, and European technology strongholds.

0. Bottom line first

Korea's future in shipbuilding depends less on building more ships and more on building cleaner, smarter, and more trusted ships. China has secured quantitative dominance, Japan is targeting standards through alliances, and Europe is defending high-value technology niches.

Quantitative dominance

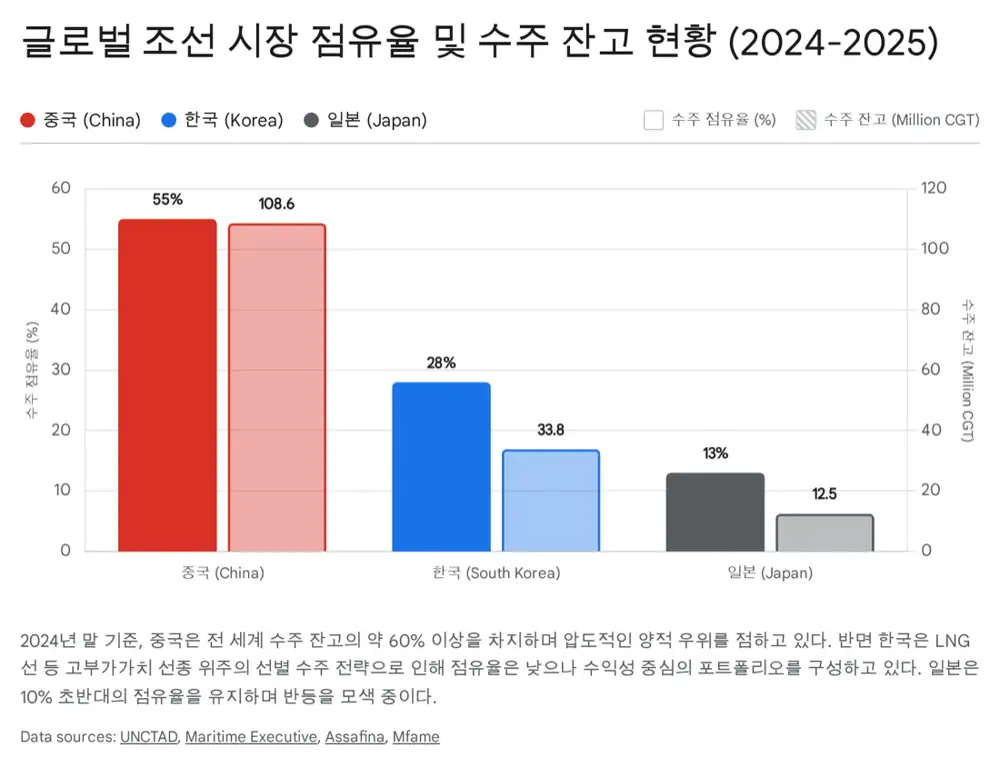

The source says China holds about 55-60% of global newbuilding orders and more than 108 million CGT of orderbook, over 60% of the world total.

Qualitative premium

Korea holds about 33.8 million CGT, roughly 20%, while selectively booking LNG, VLAC, and FLNG vessels.

Standards and technology

Japan pushes All Japan standardization; Europe defends through cruise, defense, and green systems.

1. Market dynamics: China in volume, Korea in quality

In 2024-2025, the shipbuilding supercycle is being reshaped by decarbonization, digitalization, and geopolitical security. The source says China accounts for about 55-60% of global newbuilding orders and more than 108 million CGT of orderbook, over 60% of the global total. Korea holds about 33.8 million CGT, around 20%.

Interpretation: The gap does not simply mean Korea is losing competitiveness. Korea's big three already have docks filled toward 2028 and are choosing high-value orders rather than low-margin vessels.

2. China: CSSC plus efficient private yards

The 2019 CSIC-CSSC merger created the world's largest shipbuilding group by capacity. The source separates Hudong-Zhonghua as the LNG challenger, Jiangnan as the VLAC and gas-carrier yard, and Yangzijiang as an efficient private container-ship specialist.

| Company/yard | Source position | Pressure on Korea |

|---|---|---|

| Hudong-Zhonghua | China's LNG technology flagship | Qatar Q-Max 271,000 cbm orders and 24 LNG carrier orders in 2024 |

| Jiangnan | VLAC and next-generation gas carriers | 93,000 cbm VLAC orders from ADNOC L&S |

| Yangzijiang | Private-yard efficiency | 16,800 TEU methanol container ships and early-slot alternatives |

Interpretation: The China threat is not only state-owned giants. CSSC's policy support and Yangzijiang's private efficiency both pressure Korea's price and delivery premium.

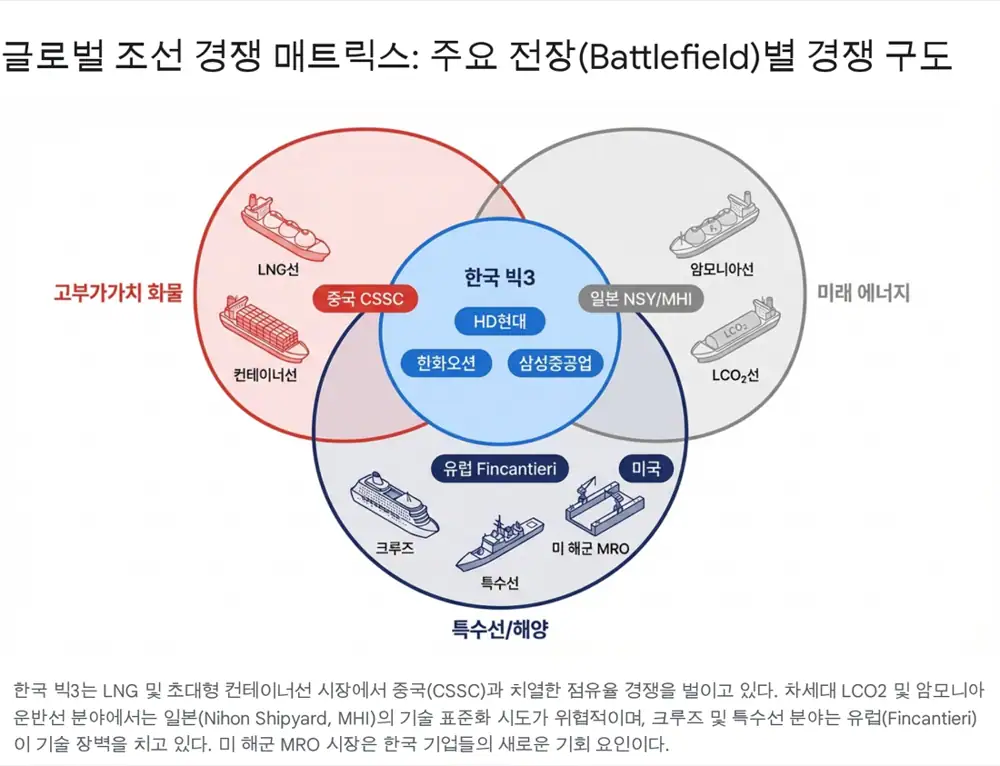

3. Japan and Europe: standards and technology fortresses

Japan is not trying to match Korea and China in raw capacity. It is pursuing All Japan alliances and standardization. Imabari/JMU restructuring and MHI/Imabari LNG/LCO2 cooperation point to a national-technology-standard strategy.

Europe defends high-value niches rather than mass commercial ships. Fincantieri and Meyer Werft compete in cruise, defense, green systems, and concepts such as ZEUS, where engineering and system integration matter more than volume.

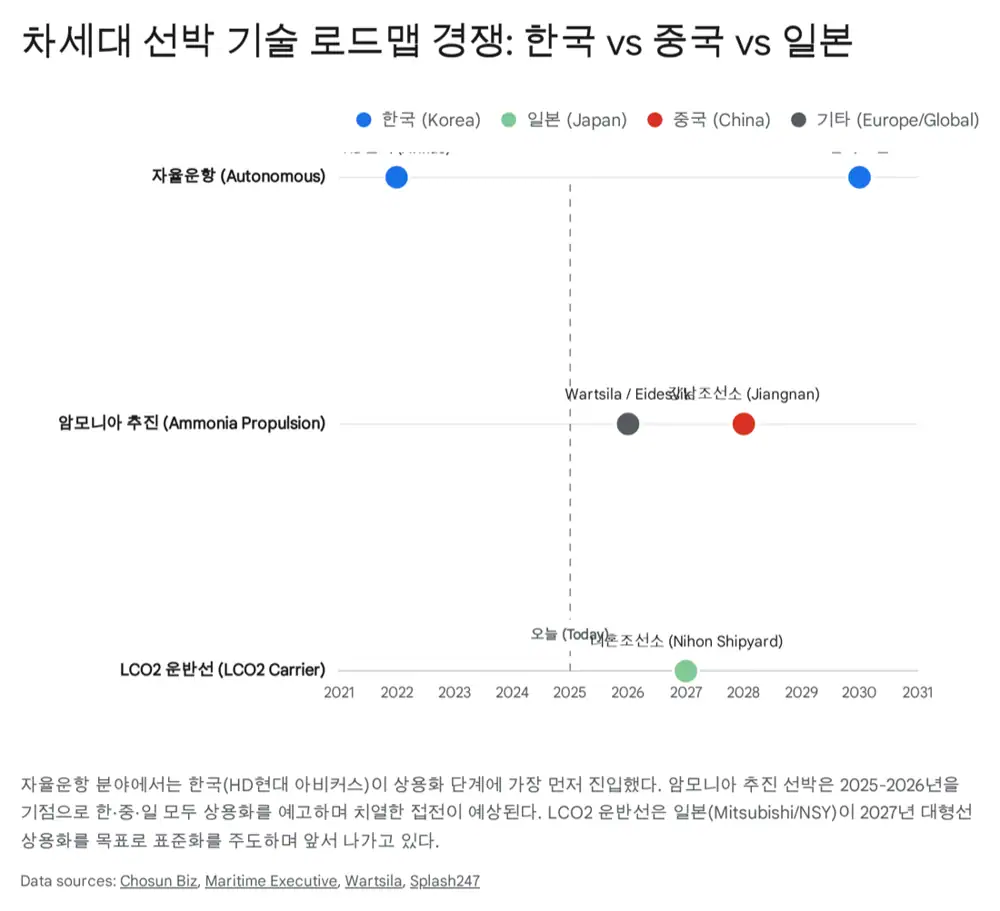

4. Future technology battleground: autonomy and next fuels

HD Hyundai Avikus

The source highlights the world's first autonomous ocean crossing by a large merchant vessel and HiNAS 2.0 commercialization.

Samsung Heavy SAS

Samsung installed SAS on Evergreen's 15,000 TEU container ship and completed a 10,000 km Pacific trial.

Smart Ship

CSSC is accumulating data through ships such as Great Intelligence, but commercial trust is still viewed as below Korea's leaders.

Ammonia and LCO2 are the key next fuels. The source says Hanwha Ocean is developing a gas-turbine ammonia propulsion system with Hanwha Power Systems, while HD Hyundai and Samsung Heavy are building VLACs with ammonia engines in cooperation with MAN ES, Wartsila, and others for 2025-2026 delivery targets. In LCO2, Mitsubishi Heavy Industries and Nihon Shipyard target large LCO2 carrier commercialization by 2027.

5. Geopolitics: Section 301 and MASGA

USTR's Section 301 investigation into Chinese shipbuilding and possible port fees on Chinese-built vessels make owners more sensitive to political risk. The source argues that for high-value LNG and container ships operated for more than 20 years, owners may increasingly prefer politically lower-risk Korean yards.

MASGA, or Make American Shipbuilding Great Again, can become a new revenue source for Korean shipbuilders. Hanwha Ocean and HJ Shipbuilding's U.S. Navy MRO wins are described as early steps; if Seventh Fleet maintenance flows into Korea, a stable long-term market may open.

6. Strategic implications for Korea

- Against China: Prove reliability with data on operating records, resale values, and quality issues in Chinese LNG vessels.

- Against Japan: Participate actively in LCO2 and ammonia standard setting to avoid isolation.

- Market expansion: Use U.S. Navy MRO as a bridgehead toward special vessels and module supply.

- Business model: Evolve from hardware ship sales to software-like models around autonomous navigation and lifecycle services.

Sources

- 1. https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224121652331

- 2. https://unctad.org/system/files/official-document/rmt2025ch2_en.pdf

- 3. https://maritime-executive.com/article/korea-claws-back-market-share-as-global-shipbuilding-market-cools

- 4. https://think.ing.com/articles/asia-shipbuilding-renaissance/

- 5. https://en.portnews.ru/news/386171/

- 6. https://www.clarksons.net/wfr/fleet

- 7. https://www.assafinaonline.com/en/article/China-Expands-Shipbuilding-Dominance-with-Record-Orderbook-in-2024?id=23620

- 8. https://www.ship-technology.com/news/china-csic-cssc-merger/

- 9. https://english.shanghai.gov.cn/en-Latest-WhatsNew/20250107/7313b7b7f198472dab052737e2eaf578.html

- 10. https://www.hellenicshippingnews.com/korean-shipbuilders-sweep-lng-orders-as-chinese-ship-contracts-drop-to-zero/

- 11. https://www.chosun.com/english/industry-en/2025/08/05/6UQZEDOGYJGFZLFPXXOXK32ERQ/

- 12. https://www.lloydslist.com/LL1153535/Hudong-Zhonghua-inks-new-orders-with-Seaspan-and-Ibaizabal

- 13. https://www.mol.co.jp/en/pr/2017/17002.html

- 14. https://www.adnocls.ae/en/news-and-media/press-releases/2024/adnoc_ls-joint-venture-awards-vlec-and-vlac

- 15. https://www.xindemarinenews.com/m/view.php?aid=56691

- 16. https://www.marinelink.com/news/new-alternativefueled-vessel-orders-531919

- 17. https://ammoniaenergy.org/articles/order-book-grows-for-ammonia-powered-engines-vessels/

- 18. https://www.rivieramm.com/news-content-hub/news-content-hub/cssc-group-adds-extra-capacity-offers-early-slots-for-container-ships-81760

- 19. https://www.offshore-energy.biz/japans-top-shipbuilder-restructures-imabari-gains-upper-hand-in-jmu/

- 20. https://www.mhi.com/news/24121901.html

- 21. https://www.mhi.com/news/23052201.html

- 22. https://www.turbomachinerymag.com/view/mitsubishi-shipbuilding-joint-venture-partners-to-establish-supply-chain-design-for-lco2-carriers

- 23. https://www.kedglobal.com/shipping-shipbuilding/newsView/ked202505130005

- 24. https://www.navalnews.com/naval-news/2025/12/hj-shipbuilding-construction-secures-first-u-s-navy-mro-contract/

- 25. https://www.chosun.com/english/industry-en/2025/08/08/RR5CE25FWFFBZNHZCIF7PCM4XA/

- 26. https://container-news.com/daehan-shipbuilding-secures-contract-for-two-8800-teu-container-ships/

- 27. https://shippingtelegraph.com/container-news/daehan-shipbuilding-scores-two-boxship-newbuilding-orders-for-232-1m/

- 28. https://www.fincantieri.com/en/innovation/beyond-innovation/

- 29. https://www.fincantierisi.it/innovation

- 30. https://today.rtl.lu/news/business-and-tech/german-shipyard-rescued-by-the-state-gets-mega-deal-210608554

- 31. https://maritime-executive.com/article/german-government-and-banks-complete-financial-rescue-of-meyer-werft

- 32. https://biz.chosun.com/en/en-industry/2025/12/24/6KFP3XGDUFGNJL6AZ2JYCYPOSY/

- 33. https://avikus.ai/en-us/press/hd-hyundais-avikus-supplies-autonomous-navigation-solutions-to-a-large-fleet-of-30-vessels

- 34. https://www.brookesbell.com/news-and-knowledge/article/samsung-and-evergreen-complete-10-000-km-ai-navigation-trial-on-ever-max-159610/

- 35. https://maritime-executive.com/article/ai-based-autonomous-navigation-guides-boxship-during-pacific-crossing

- 36. https://maritime-executive.com/article/chinese-shipbuilders-pursue-vessel-autonomy

- 37. https://www.lr.org/en/knowledge/press-room/press-listing/press-release/2017/smart-shipping-moving-forward/

- 38. https://maritime-executive.com/index.php/article/japanese-shipbuilders-target-2027-for-lco2-carrier-introduction