DEEP RESEARCH · SHIPBUILDING ENGINE INDUSTRY

Global Marine Engine Industry Deep-Dive: Competitive Landscape and Future Strategy of Hanwha Engine and HD Hyundai Marine Engine

Korea's two-pillar restructuring meets a green-fuel paradigm shift (methanol, ammonia, hydrogen) — diagnosing opportunities and threats for Korean engine makers.

0. Bottom line first

In 2025, global shipbuilding and shipping have entered a Dual Super-cycle — the traditional replacement super-cycle for aged vessels combined with IMO 2050 Net-Zero regulation forcing a technological transition to green propulsion. The engine is no longer a mere mechanical power source; it is the core solution that determines a vessel's asset value and operability.

Official fact: Korea's market has consolidated into two camps — HD Hyundai (HHI-EMD + HD Hyundai Marine Engine + HD Hyundai Engine) and Hanwha (Hanwha Engine). China's CSSC now 100% owns Swiss licensor WinGD. Japan, despite Mitsui E&S and J-ENG's technical prowess, faces a credibility crisis from KHI and Hitachi Zosen data-falsification scandals.

Interpretation: Korean firms benefit from Japan's fall and supply-tight super-cycle ASP gains, but face China's WinGD-backed catch-up and crankshaft-supply bottlenecks. The decisive battle: who first achieves stable mass-production of ammonia engines, and who can sustain a technology gap against China's relentless catch-up.

1. Introduction: A Dual Super-cycle and the Propulsion Paradigm Shift

As of 2025, the global shipbuilding and shipping industry faces a Great Transformation that transcends ordinary business cycles. It is a Dual Super-cycle — combining the conventional super-cycle of aged-vessel replacement demand with the regulatory imperative of the IMO's 2050 Net-Zero target, which forces a technological transition to green propulsion systems. Where engines were once mere mechanical power sources, in the decarbonization era they have been elevated to core solutions determining a vessel's asset value and operating viability, and to the technological bulwark for surmounting environmental regulation.

Korea's marine engine industry has completed a profound structural realignment. Hanwha Group acquired HSD Engine (formerly Doosan Engine) and launched Hanwha Engine, while HD Hyundai Group acquired STX Heavy Industries and reborn it as HD Hyundai Marine Engine — completing the final piece of its engine portfolio. The Korean market is now a proxy war between two giants: HD Hyundai and Hanwha. But the global picture is more complex.

China, leveraging engine makers under state-owned CSSC (China State Shipbuilding Corporation), is eroding market share with overwhelming capacity and price competitiveness, and has escaped licensing dependence by 100%-owning Switzerland's WinGD. Japan, with traditional powerhouse Mitsui E&S and J-ENG (the sole owner of an independent UE Engine brand), pursues differentiation in hydrogen and ammonia — but consecutive data-falsification scandals have triggered a credibility crisis. Meanwhile European licensors MAN Energy Solutions (Germany) and Wärtsilä (Finland) are evolving beyond licensing into direct system-integration solution providers, reshaping the market.

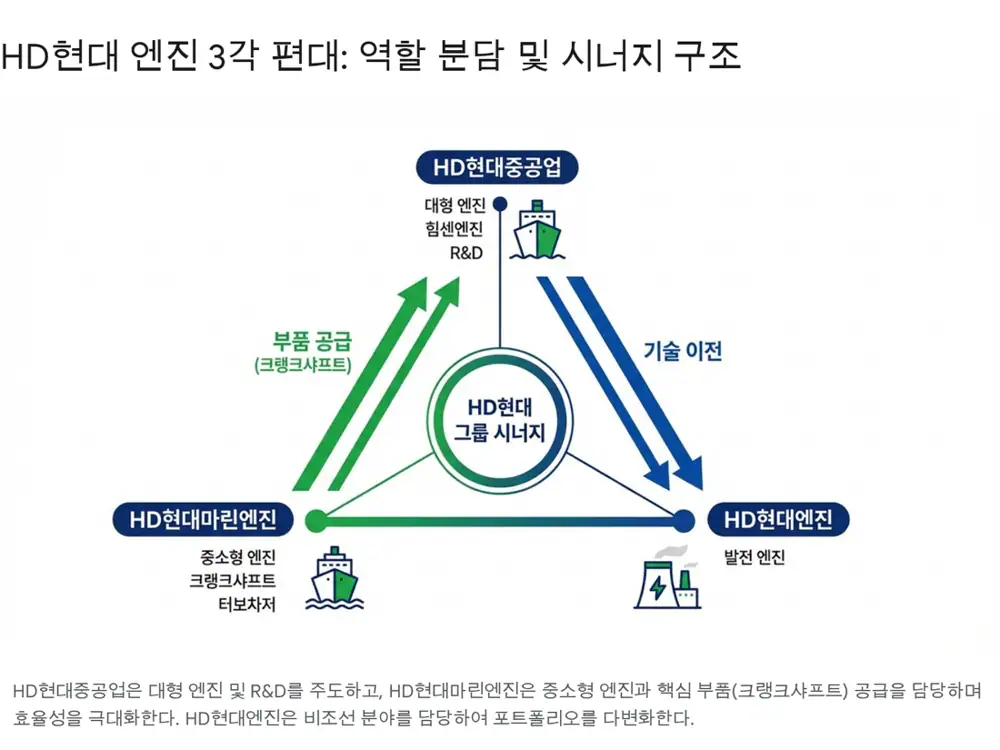

2. Korea's Engine Industry Realignment: Two-Pillar Structure and Niche Competition

From 2024 onward, Korea's marine engine market has converged into two giants — HD Hyundai and Hanwha — through vertical integration that consolidated the previously fragmented landscape (HHI-EMD, HSD Engine, STX Heavy Industries, STX Engine).

2.1. HD Hyundai Group: Vertical and Horizontal Integration Complete

Through the STX Heavy acquisition, HD Hyundai has become the world's only group covering large–medium–small engines plus engine components (crankshafts, turbochargers). This is not just capacity expansion — it is role specialization across engine affiliates for maximum efficiency and supply-chain stability.

HD Hyundai Heavy Industries · Global #1

Over 35% global share in large 2-stroke engines. Containers, LNG carriers, VLCCs. Proprietary 4-stroke brand 'HiMSEN'. R&D hub for methanol and ammonia.

ex-STX Heavy · Group 'core'

Mid-small 2-stroke and dual-fuel engines. In-house crankshafts and turbochargers. Post-acquisition, utilization surged via HD Hyundai Mipo etc. order flow.

Power generation & land plants

Formerly HHI's onshore power generation unit. Hedges marine-engine volatility; portfolio diversification.

2.2. Hanwha Engine: A Strong #2 Powered by Synergy with Hanwha Ocean

Hanwha Engine (formerly HSD Engine / Doosan Engine) is the world's #2 large marine engine maker. Since joining Hanwha Group, it has been generating strong captive synergy with Hanwha Ocean. Large 2-stroke low-speed engines account for over 90% of revenue. It holds the world-first commercialization record for LNG dual-fuel (DF) engines.

Investment had been constrained during the Doosan era; under Hanwha's deep capital, the company is aggressively upgrading green-engine facilities. Captive orders from Hanwha Ocean's high-value vessels (LNG carriers, VLCCs) sharply reduce the uncertainty inherent to order-based industries. It also acquired Norway's marine-electrification specialist SEAM, declaring its transformation from engine maker into a 'total propulsion solution provider'.

Interpretation: A potential risk: Hanwha Engine depends heavily on rival HD Hyundai Marine Engine and Doosan Enerbility for crankshafts — a supply-chain vulnerability worth monitoring.

2.3. STX Engine: The Hidden Champion in Defense and Special Vessels

Many market analyses confuse it, but STX Engine is a separate listed entity, completely distinct from HD Hyundai Marine Engine (formerly STX Heavy Industries). STX Engine does not produce large low-speed merchant marine engines; its focus is defense engines (tanks, self-propelled howitzers) and medium-speed (4-stroke) diesel engines.

Through licenses with Germany's MTU (Rolls-Royce Power Systems) and MAN Energy Solutions, STX Engine supplies main engines and gensets for navy ships and coast guard patrol vessels. Riding the K-defense export boom (K9 self-propelled howitzer etc.), defense revenue is surging. It also has independent capability in electronics (radar, sonar). STX Engine should thus be classified as a niche-market champion — competing with HHI's HiMSEN in medium-speed engines and dominating the defense niche — rather than as a direct competitor of Hanwha Engine or HD Hyundai Marine Engine.

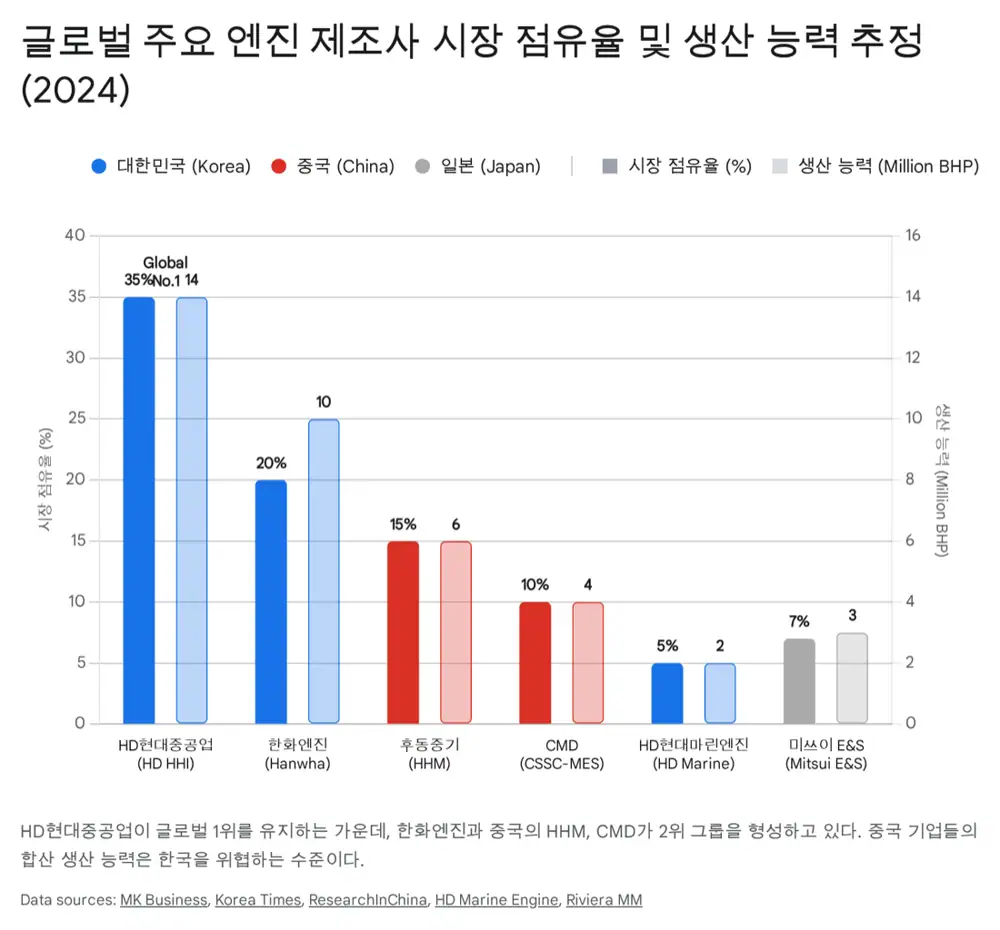

3. China: From Volume Offensive to Technological Self-Reliance

As the world's largest shipbuilding nation, China aggressively pursues a 'domestic-build, domestic-source' policy, sourcing engines for its yards from domestic makers. China's engine companies are vertically integrated under CSSC (China State Shipbuilding Corporation) and command vast capacity — the most threatening competitors to Korean firms.

3.1. CSSC's Big Three: HHM, CMD, DMD

Hudong Heavy Machinery

China's top marine engine maker. Core of CSSC Engine (CSE). 5+ million HP annual capacity. Development & testbed for WinGD engines.

CSSC-MES Diesel

CSSC × Mitsui E&S JV in Shanghai Lingang. Mega-bore engines (90~98 bore). Recently delivered the world's most powerful MAN B&W 12G95ME-C10.5-LGIM methanol engine to OOCL.

Dalian Marine Diesel

Dalian, partnered with DSIC. 'Big 3' in large low-speed engines. Independently built and delivered the world's first methanol dual-fuel low-speed engine.

3.2. WinGD: China's 'Master Stroke' — Owning the Licensor

Official fact: The global large-engine market is split between Germany's MAN Energy Solutions and Switzerland's WinGD (Winterthur Gas & Diesel). CSSC owns WinGD 100%.

Interpretation: Korean and Japanese firms pay 5~10% of revenue as royalties; China internalizes the same technology via owned WinGD with no royalty burden. WinGD's Shanghai Global Technical Centre (GTC) conducts joint R&D with Chinese makers — a structural advantage in the next-generation engine race.

3.3. Threats and Limits Against Korean Firms

As Chinese yards raise local-content requirements, Korean engine exports to China are squeezed. Commodity vessel segments (bulkers, mid-small tankers) are already dominated by Chinese engines. However, in high-difficulty dual-fuel (DF) control and methane slip mitigation, China still trails Korea in reliability — a key reason global shipowners continue to prefer Korean engines.

4. Japan: Technical Pride Meets a Credibility Crisis

Once the world's top shipbuilder, Japan now survives on tech-led niches and captive volume from domestic carriers (NYK, MOL, K-Line). But the recent wave of quality data-falsification scandals has shaken 'Made in Japan' engine credibility at the root.

4.1. Mitsui E&S: The Technology Leader

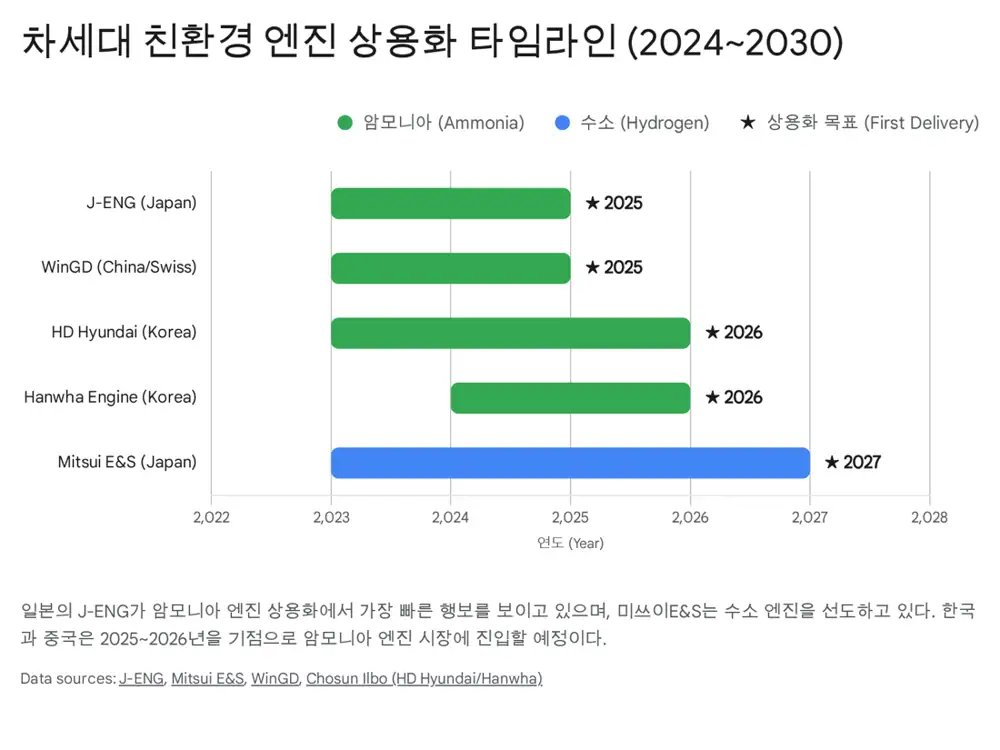

Japan's largest marine engine maker, Mitsui E&S has held world-class technology since its 1926 B&W (now MAN ES) partnership, reaching 120 million HP cumulative production. It acquired IHI's engine division (formerly Diesel United) to launch Mitsui E&S DU, gaining both MAN ES and WinGD licenses. It is the world leader in hydrogen engines — in March 2024, it successfully ran the world's first hydrogen combustion test on a 50cm-bore large 2-stroke engine, leapfrogging Korea and China (who focus on ammonia/methanol) into the next-next-generation fuel.

4.2. Japan Engine Corporation (J-ENG): Pride of Proprietary Tech

J-ENG (formerly Mitsubishi Heavy Industries' engine division) is the world's only licensor/maker with its own brand 'UE Engine' — not licensed from MAN or WinGD. With strong Japanese government support, it leads ammonia engine development: in 2025, it completed the world's first commercial ammonia-fueled engine (7UEC50LSJA-HPSCR) and entered demonstration — roughly a year ahead of Korean firms. Weakness: heavy domestic dependence and a thinner global service network than MAN/WinGD. To offset this, it licenses Chinese makers (GDF etc.) to expand its ecosystem.

4.3. Kawasaki Heavy Industries (KHI) & Hitachi Zosen: The Scandal Shock

Official fact: Since 2024, IHI, Hitachi Zosen, and KHI have admitted decades of falsified fuel-consumption and NOx emission data. KHI alone admitted falsifying data on 673+ engines since 2000. Hitachi Zosen spun off its engine business, formed Hitachi Zosen Marine Engine JV with Imabari Shipbuilding, and renamed itself Kanadevia.

Interpretation: Global shipowner avoidance of Japanese engines is materializing. In a trust-driven shipping industry, recovery will be slow — a clear windfall for Korean engine makers.

5. Global Licensors and Western Competitors

Korean engine makers mostly produce under license; the original-technology licensors hold a dual status as partner and competitor. U.S. and European firms also wield strong influence in medium-speed and special-purpose engines.

MAN Energy Solutions

About 80% of global large 2-stroke market. HHI-EMD, Hanwha Engine, STX Engine all license MAN. Rebranded as Everllence; packaging FGSS, SCR/EGR etc. for higher value capture.

Wärtsilä

After selling 2-stroke (WinGD) to CSSC, focuses on 4-stroke medium-speed, integrated propulsion, and digital solutions. Direct competitor to HiMSEN. Benchmark for the 'total solutions' model.

Caterpillar & Cummins

High-speed / medium-speed strength. Coastal vessels, tugs, OSVs, naval auxiliaries. Caterpillar's MaK is a key HiMSEN competitor.

6. Next-Gen Green Fuel Engine War: Ammonia vs Methanol vs Hydrogen

Future market leadership hinges on who can stably commercialize green-fuel engines first.

6.1. Methanol Engine: Today's Battleground

HD Hyundai Heavy Industries and Hanwha Engine lead in methanol-engine maturity. HHI successfully delivered engines for Maersk's 16,000 TEU methanol-powered container ships, capturing the market. Hanwha Engine also won HMM's methanol container vessel order. CSSC was initially behind, but CMD and HHM have recently produced mega methanol engines, narrowing the gap. China's WinGD partnership enables remarkably fast technology absorption.

6.2. Ammonia Engine: The 2025~2026 Decisive Battle

Ammonia poses high technical barriers due to toxicity and poor combustibility. HHI and Hanwha Engine are in final development for 2025~2026 deliveries. However, J-ENG (Japan) is sprinting for the world-first commercialization title — viewed as Japan's last card for shipbuilding revival. China, leveraging WinGD, also plans ammonia-engine vessel deliveries from 2025. The three-nation race is at peak intensity.

6.3. Hydrogen Engine: The Future Grail

In hydrogen engines, Japan dominates. Mitsui E&S succeeded in large marine hydrogen-engine combustion testing — far ahead. Korea is still in basic research or focused on small engines. Japan's hydrogen leadership is a long-term wildcard that could restore its dominance in the zero-carbon ship era.

7. Conclusion: Opportunities, Threats, and Strategic Recommendations for Korean Firms

Bull · Opportunities

- Collapse of Japanese rivals: The Japanese data-falsification fallout accelerates order rotation toward Korean makers (Hanwha Engine, HD Hyundai Marine Engine)

- Sustained super-cycle: Strong LNG and container ship orders sustain a supply-tight market for 3~4 years — engine ASP rising, margins improving

- Group synergy: Both HD Hyundai and Hanwha secured stable captive volume through shipbuilding-engine vertical integration — shock-absorption strength

Bear · Threats

- China's technical catch-up: WinGD ownership + government backing rapidly narrows the gap with Korea. Commodity engine markets already pressured

- Supply-chain bottleneck: Crankshaft and other critical-component shortages can disrupt production. Hanwha Engine carries the latent risk of sourcing key parts from rival HD Hyundai affiliates

Base · Strategic Recommendations

For investors, HD Hyundai Marine Engine is a structural growth play — utilization rising on group integration, margins improving on parts internalization. Hanwha Engine is more of a value name — dominating large engines and generating stable cash flow via Hanwha Ocean synergy. Ultimately, the battle hinges on 'who first achieves stable mass-production of ammonia engines' and 'who can sustain a technology gap against China's catch-up'. Korean firms must expand R&D and diversify component supply to defend their global leadership.

Sources

- Global and China Marine Diesel Engine Industry Report — ResearchInChina: researchinchina.com

- CSSC takes full ownership of WinGD — Marine Log: marinelog.com

- Misconduct in Testing of Marine Diesel Engines — Kawasaki Heavy Industries: global.kawasaki.com

- Kawasaki Heavy in growing Japanese engine scandal — Splash247: splash247.com

- STX Heavy Industries acquired — MK: mk.co.kr

- HD HYUNDAI ENGINE & MACHINERY — CIMAC Congress 2025: cimaccongress.com

- HD Hyundai vs Hanwha ship engine market — Korea Times: koreatimes.co.kr

- STX Heavy rebranded as HD Hyundai Marine Engine — Korea Herald: koreaherald.com

- STX ENGINE — Komachine: komachine.com

- STX Engine at MADEX 2025: stxserviceamericas.com

- WinGD Research & Testing Facilities: wingd.com

- Licensed to slake the power thirst — Riviera: rivieramm.com

- World's Most Powerful Methanol Engine — Everllence: man-es.com

- Everllence licensees: everllence.com

- China Classification Society — methanol engine: container-news.com

- China's first methanol DF engine — Offshore-Energy: offshore-energy.biz

- WinGD Shanghai centre — Seatrade-Maritime: seatrade-maritime.com

- South Korea engine exports surge — CHOSUNBIZ: biz.chosun.com

- Mitsui E&S Marine Propulsion: mes.co.jp

- MITSUI-MAN B&W 120M HP: mes.co.jp/news

- MITSUI Hydrogen Test — Everllence: man-es.com

- Japan Engine Corporation: j-eng.co.jp

- J-ENG ammonia engine — RINA: rina.org.uk

- J-ENG LSJA / LSGH product: j-eng.co.jp

- J-ENG China licensee — Power Progress: powerprogress.com

- Hitachi Zosen 25-year falsification — DieselNet: dieselnet.com

- KHI NOx Scandal — Marine Insight: marineinsight.com

- Kanadevia — Wikipedia: en.wikipedia.org

- Hitachi Zosen × Imabari basic agreement: kanadevia.com

- Everllence — Ammonia Energy Association: ammoniaenergy.org

- Everllence × Hyundai ammonia gas carrier: offshore-energy.biz

- Wärtsilä — Wikipedia: en.wikipedia.org

- Wärtsilä × CSSC 2-stroke JV: wartsila.com

- Marine Engines — MarketsandMarkets: marketsandmarkets.com

- Marine Propulsion Engine Companies — Mordor: mordorintelligence.com

- Methanol Engines Major Order — Everllence: man-es.com

- Korean Shipbuilders Ammonia Propulsion — Chosun: chosun.com

- WinGD ammonia engine on EXMAR vessels: wingd.com

- Original Naver Blog: m.blog.naver.com