DEEP RESEARCH · Hanwha Engine

Hanwha Engine: the heart of the shipbuilding supercycle and green propulsion

A structural-growth review through backlog, dual-fuel engines, and the SEAM acquisition

0. Bottom line first

Hanwha Engine is a direct shipbuilding-cycle beneficiary with both Hanwha captive stability and external-customer growth.

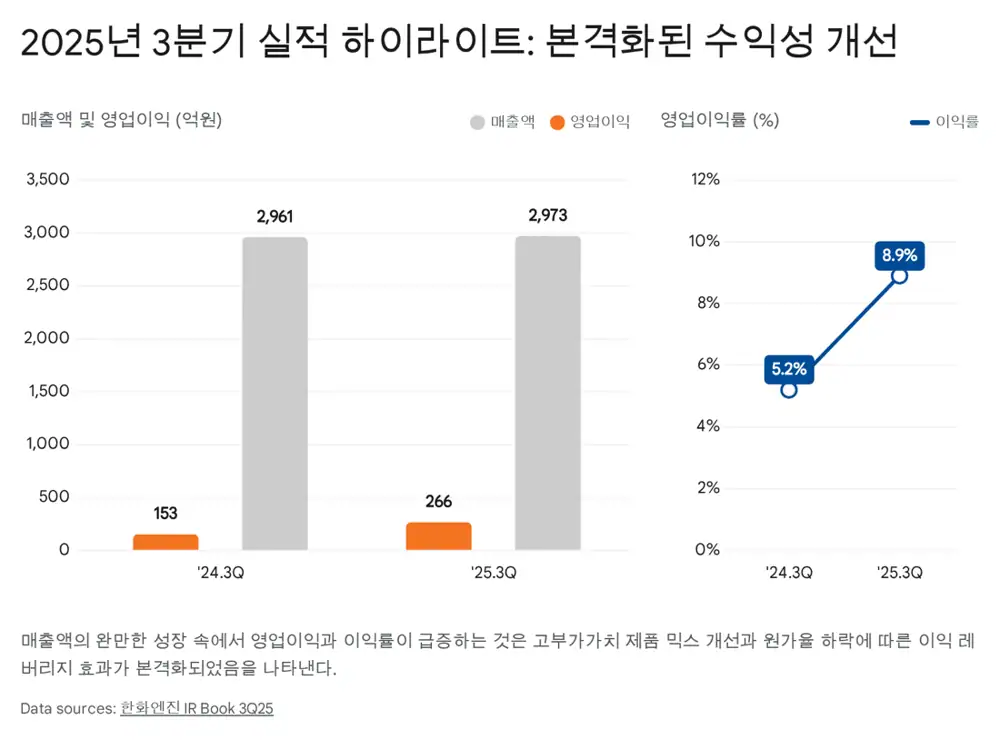

Official fact: The source cites Q3 2025 OPM of 8.9%, up 3.7 percentage points, and marine engine/SCR revenue of about KRW 891.6 billion, 88.9% of sales.

Interpretation: Low-priced backlog exhaustion and LNG/methanol dual-fuel engine revenue are driving the turnaround.

8.9%

Q3 2025 margin improvement

KRW 3.988tn

Up 17.8% from year-end 2024

-KRW 297.1bn

Near net-cash profile

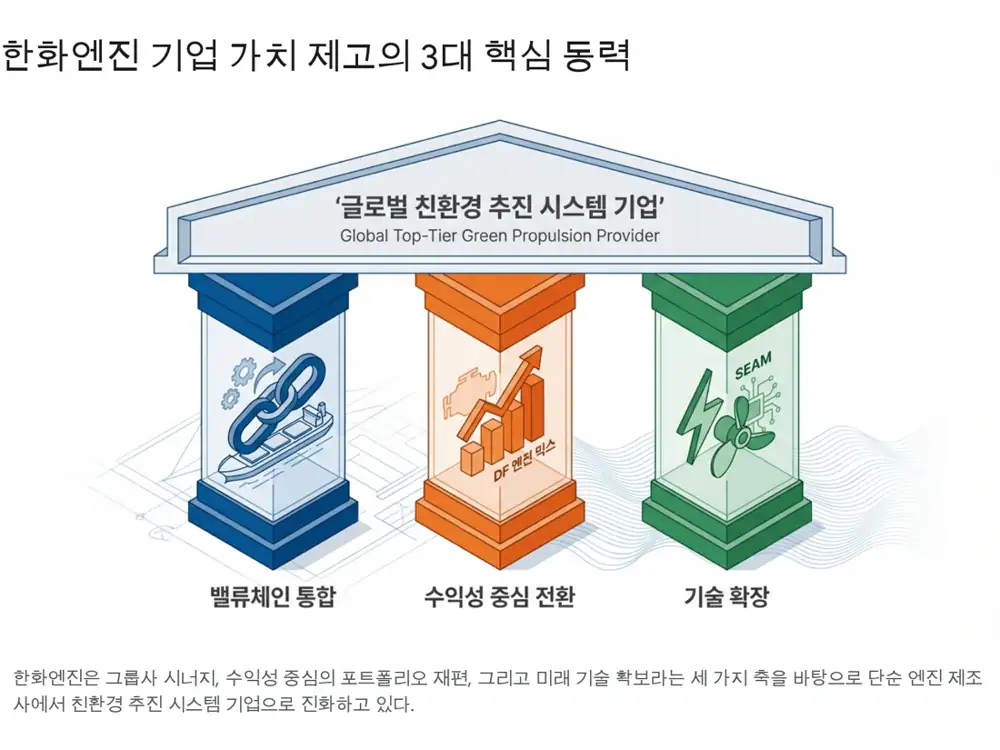

1. Growth structure

2. History and ownership

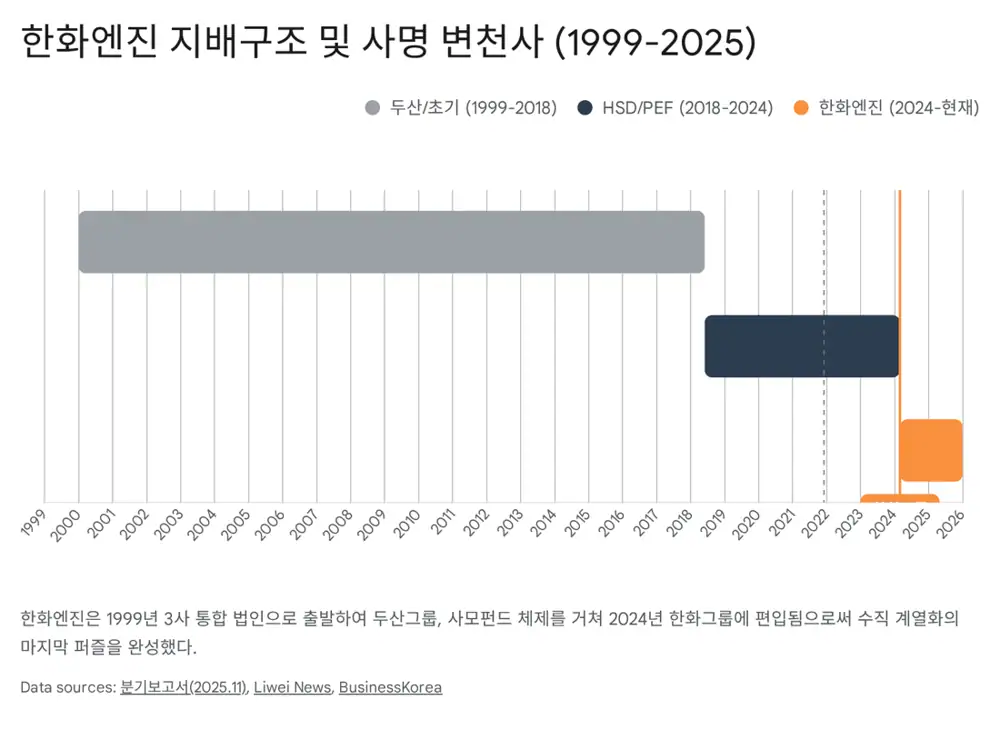

The company traces back to marine-engine localization around 1983. On December 30, 1999, Samsung Heavy and Korea Heavy Industries engine divisions formed the HSD Engine structure. After the 2018 PEF period, Hanwha Impact acquired 32.77% in 2024 and relaunched it as Hanwha Engine.

3. Technology and orders

The source highlights the world’s first commercialization of a marine dual-fuel low-speed engine in 2013 and LP-SCR development in 2014. End-Q3 2025 backlog was KRW 3.988 trillion, and cumulative new orders were KRW 1.4959 trillion, up 118% year on year.

4. SEAM acquisition

Norway’s SEAM has e-SEAMatic, more than 1,000 project references, a 2016 battery-powered PSV, and a 2021 liquid-hydrogen ferry reference. The acquisition expands the portfolio from large combustion engines to electric and hybrid propulsion.

5. Risks and view

Risks are the shipbuilding cycle, raw materials, and hydrogen/ammonia standard competition. I would watch whether roughly KRW 4 trillion of backlog and SEAM synergies support a re-rating after 2027.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224121620772

- CN Liwei: https://www.cn-liwei.com/news_detail/845.html

- BusinessKorea: https://www.businesskorea.co.kr/news/articleView.html?idxno=212147

- Ship Technology: https://www.ship-technology.com/news/hanwha-engine-first-vcr-equipped-dual-fuel-engine-lng-carriers/