DEEP RESEARCH · HD HYUNDAI MARINE ENGINE

HD Hyundai Marine Engine: Structural Growth in the Shipbuilding Supercycle

A translated report on the former STX Heavy turnaround, HD Hyundai integration, and eco-engine demand.

0. Bottom line first

My core view is that HD Hyundai Marine Engine is being re-rated from a component supplier into an engine platform exposed to the shipbuilding supercycle, environmental regulation, and HD Hyundai group synergy. The 18.6% 3Q25 operating margin is the source's strongest number.

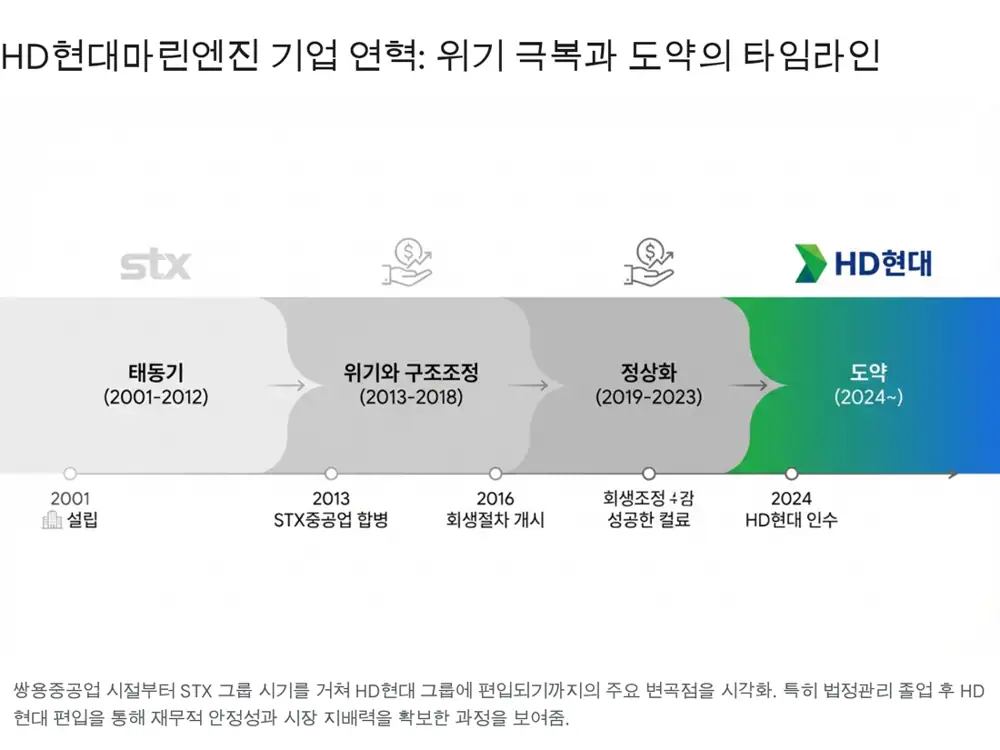

From STX to HD Hyundai

After court receivership and restructuring, the company entered HD Hyundai in July 2024 with a lean fixed-cost base.

DF engine ASP

The source says LNG, LPG, and methanol dual-fuel engines carry higher technical difficulty and ASPs more than 15-20% above diesel engines.

Utilization ramp

Marine-engine utilization is expected to rise from 64.6% in 2024 to more than 90% in 2025.

1. History and the meaning of group integration

The company's roots go back to Ssangyong Heavy Industries in 1976, while the current legal entity began as Enpaco, spun out from STX's materials business on June 15, 2001. It absorbed old STX Heavy Industries in 2010, then went through a creditor workout in 2013 and rehabilitation in 2016 after the STX liquidity crisis.

Official fact: The source says HD Korea Shipbuilding & Offshore Engineering signed the main agreement in July 2023, completed merger review, brought the company into HD Hyundai in July 2024, and secured 35.05% ownership with about KRW 81.3 billion.

Interpretation: Cost cuts during restructuring were survival measures then, but today they create operating leverage as revenue recovers.

2. Three moats: policy, relationship, technology

Policy moat

IMO regulation, carbon costs, EEXI, and CII effectively push shipowners toward low-carbon propulsion. The source says eco-friendly DF engines can command ASPs more than 15-20% above diesel engines, and highlights the 2019 world-first ship-propulsion LPG dual-fuel engine trial as evidence of early technology positioning.

Relational moat

Ship engines represent about 10% of vessel construction cost, and shipowners/yards prefer qualified AML suppliers. Orders such as KRW 103.4 billion from HD Hyundai Mipo and KRW 29.5 billion from HD KSOE support payment stability and planned production.

Technical moat

The source views crankshaft and turbocharger know-how, mid-small engine competitiveness, and eco-engine development as defenses against Chinese entrants.

3. Earnings structure and production efficiency

| Item | Source number/content | Investment read |

|---|---|---|

| 3Q25 operating margin | 18.6% | Evidence of high-price backlog and supply-chain efficiency |

| 2024 utilization | 64.6% | Unused capacity remained |

| 2025 utilization outlook | More than 90% | Leverage without major new CAPEX |

| Chinese customer reliance | Xiamen Xiangyu etc. about 28.74% in 2023 | Past collection risk and low-price pressure |

Interpretation: For manufacturers, the best margin phase often comes when utilization rises without new plants. The 2025 numbers point to that phase.

4. Customer mix and bargaining power

HD Hyundai group

Orders from HD Hyundai Mipo and HD KSOE form a stable revenue base.

External customers

KRW 117.4 billion from Samsung Heavy and KRW 35.7 billion from Qidong Xiangyu show it is not only a captive supplier.

Aftermarket

Engines generate replacement parts and service demand across a 20-30 year ship life.

5. Conclusion and risks

Upside

- HD Hyundai group synergy can improve both utilization and earnings quality.

- Low-price backlog runoff and higher DF-engine mix could support mid-to-high-teens operating margins.

- The AM business can become a cumulative cash generator as more vessels are delivered.

Risks

- Chinese engine makers' local-content policies and low-price competition are medium-term threats.

- If shipbuilding orders peak out, engine orders may slow with roughly a 1.5-year lag.

- High export exposure means sharp KRW appreciation can reduce profits.

Sources

- 1. https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224121620004

- 2. https://www.hd.com/kr/newsroom/media-hub/press/view?detailsKey=3168

- 3. https://namu.wiki/w/HD%ED%98%84%EB%8C%80%EB%A7%88%EB%A6%B0%EC%97%94%EC%A7%84?uuid=0b96cc2d-a947-4958-bf1e-03d101d3b092

- 4. https://m.ceoscoredaily.com/page/view/2025120215275966614

- 5. https://www.dailian.co.kr/news/view/1390004

- 6. https://zdnet.co.kr/view/?no=20240730180221

- 7. http://www.hd-marineengine.com/core/fileDown.do?ATTACH_SEQ=3854&ATTACH_SERL=1

- 8. https://v.daum.net/v/yHl0C5Eopm?f=m

- 9. https://www.bloter.net/news/articleView.html?idxno=647989