DEEP RESEARCH · Samsung Heavy Industries (010140)

Samsung Heavy Industries (010140) Deep Dive: FLNG Hegemony and the Asymmetry Created by a 100% FX Hedge

3Q25 results, FLNG dominance, and the KRW 1,480 to 1,250 FX scenario — research note reformatted from a Gemini-authored draft.

0. Bottom line first

Samsung Heavy is a rare shipbuilder that holds two asymmetric weapons simultaneously: FLNG global hegemony, and a 100% full FX hedge. Even in a sharp KRW 1,480 to 1,250 scenario, operating-income damage stays limited while non-operating items book large derivative valuation gains — net income and the debt ratio improve at the same time.

- 3Q25 cumulative revenue KRW 7.8121T (+8% YoY), operating profit KRW 566B, already 90% of the full-year 630B guidance reached in just three quarters. 3Q OPM 9.0% vs. 7.6% prior quarter (+1.4pp).

- Of the world's 5 large FLNG units ever ordered, 4 were won by Samsung Heavy (Prelude, Petronas 1 and 2, Coral) — it effectively defines the market standard.

- 3Q25 cumulative derivative trading gains KRW 523.6B, valuation gains KRW 392.1B — the 100% hedge actually showing up in the P&L.

- 2026 catalysts: US LNG project FIDs restart (CP2 Ph.1, Rio Grande T4/T5) plus Clarksons forecast of 100 100K+ cbm LNG carrier orders (2x the 50 of 2025) — the growth slope accelerates.

1. Setup: Korean shipbuilding at an inflection point

Official fact: The global shipbuilding industry is past a simple cyclical rebound and into the opening innings of a structural super-cycle. The two dominant 2025 themes are decarbonization and energy security. IMO regulation and the EU ETS are forcing the retirement of old vessels and the switch to dual-fuel propulsion. Energy supply-chain reshuffling post Russia-Ukraine sustains demand for LNG carriers and offshore production facilities.

Official fact: Samsung Heavy was founded in 1974, headquartered in Seongnam (Gyeonggi-do), and operates its shipbuilding/marine and civil construction businesses centered on the Geoje shipyard. After the offshore plant losses and restructuring of the mid-2010s, it has completed its transition into a "technology-centric, high-margin business structure."

Interpretation: The company's value volatility is essentially driven by global shipping cycles, energy prices, and FX. This report is therefore organized around four axes: (1) portfolio and earnings, (2) structural moats including FLNG and the smart yard, (3) CEO Choi Sung-ahn's philosophy, and (4) the KRW 1,480 to 1,250 FX scenario.

2. 3Q25 results and financial structure

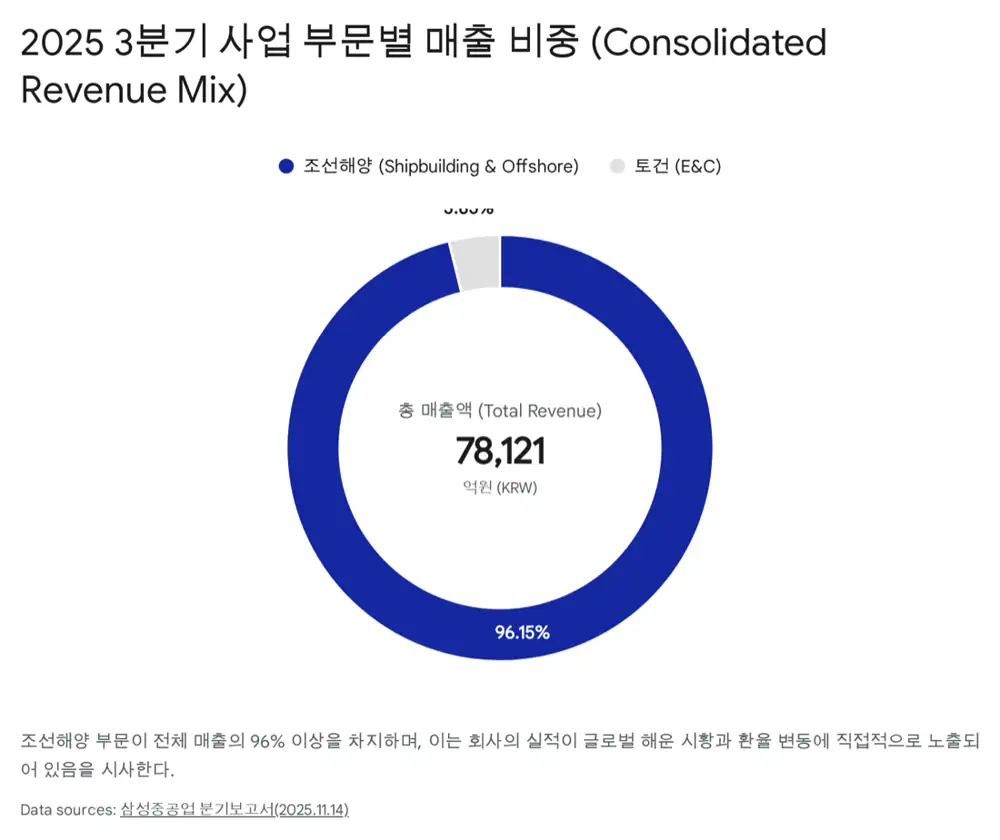

2.1 Portfolio — effectively a single business

Official fact: Two segments. Shipbuilding/marine revenue KRW 7.5112T (96.15%); civil construction KRW 300.9B (3.85%).

| Segment | 3Q25 revenue | Share |

|---|---|---|

| Shipbuilding/marine | KRW 7.5112T | 96.15% |

| Civil construction | KRW 300.9B | 3.85% |

Interpretation: Civil construction is essentially incidental. Equity value = shipbuilding/marine cycle beta. With foreign shipowners as primary customers, FX risk management becomes the core operating variable.

2.2 3Q25 numbers — a Product Mix-driven quality jump

Official fact: 3Q25 consolidated cumulative revenue KRW 7.8121T (+8% YoY), operating profit KRW 566B. 90% of the full-year KRW 630B target hit in three quarters. 3Q OPM 9.0% (+1.4pp QoQ from 7.6%).

Interpretation: Not just revenue growth — a margin step-change. Low-priced containership volumes from the past have rolled off, and high-margin LNG carriers/FLNG are taking a larger share. Management's refusal of low-priced orders is finally validated in the P&L.

2.3 Balance sheet — what 268% debt-to-equity actually means

Official fact: 3Q25 end: assets KRW 14.5394T, liabilities KRW 10.5941T, equity KRW 3.9453T, debt-to-equity ~268%. Contract liabilities (advance payments) KRW 5.3678T — roughly 50% of total liabilities. Cash and equivalents KRW 1.4030T vs. KRW 956B at prior year-end (+46.7%).

Interpretation: The headline 268% reads differently than in other industries. Shipbuilding contract liabilities are "good debt" that converts to revenue at delivery. Real borrowing burden is materially lighter than the headline. The 46.7% jump in cash is both an artifact of the hedge policy and a signal of expanded liquidity defense.

3. Economic moat

Two asymmetries separate Samsung Heavy from domestic peers (HD Hyundai Heavy, Hanwha Ocean): FLNG market dominance and the 100% FX hedge policy.

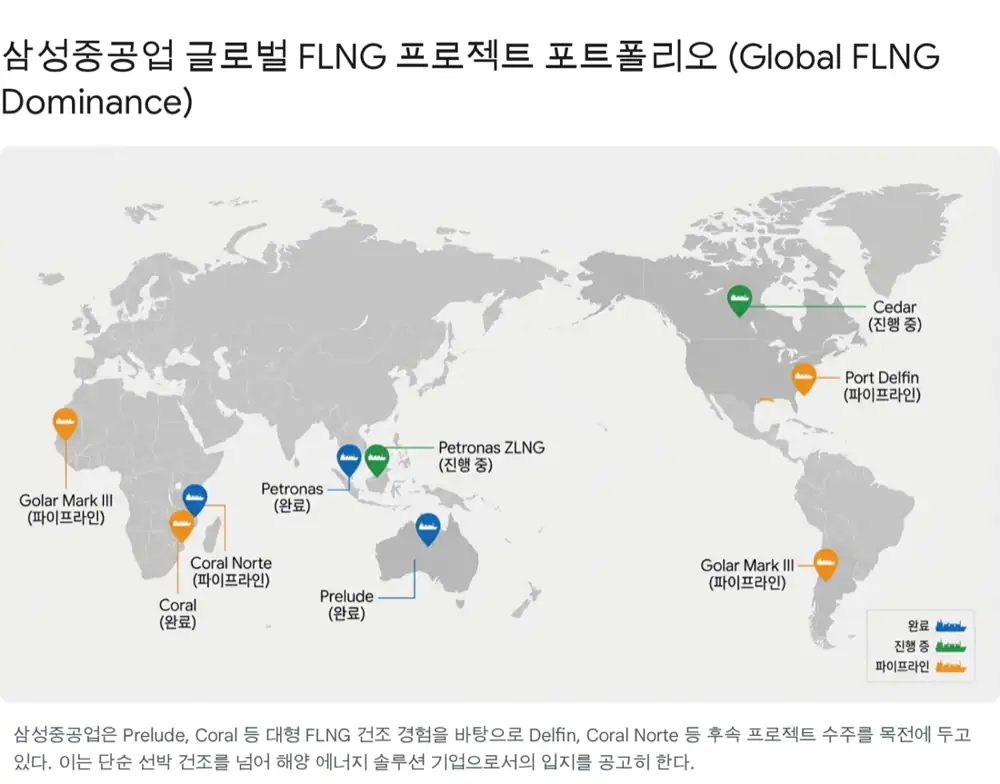

3.1 FLNG: undisputed global leader

Official fact: FLNG is a composite offshore platform that extracts, processes, liquefies, stores, and offloads gas at sea — shorter build time than onshore plants, and movable. Samsung Heavy has built 4 of the 5 large FLNGs ever ordered globally (Prelude, Petronas 1, Petronas 2, Coral).

4 reference units

Prelude, Petronas 1 and 2, Coral — 4 of 5 large FLNGs ever ordered. Effectively defines the market standard.

2 new wins

Petronas ZLNG (won Jan 2023), Cedar FLNG (won Dec 2023). On schedule.

4 active negotiations

Mozambique Coral Norte (3.4 MTPA), US Port Delfin (4.3 MTPA, LOA signed Oct 2025), Argentina/Mauritania Golar Mark III (5.0 MTPA), Canada Ksi Lisims (6.0 MTPA).

Interpretation: Given the LNG industry norm of returning to proven yards, the 4-of-5 record is not just market share — it is a structural barrier. A challenger yard would require the operator to absorb first-of-its-kind cost overruns, which is effectively an impossible board decision.

3.2 Green-tech leadership and the smart yard

Official fact: In Sep 2025, Bureau Veritas (France) granted AIP for an ammonia-based hydrogen fuel-cell propulsion crude carrier. Cooperating with WinGD (Switzerland) and others on ammonia engine technology. The Geoje yard is accelerating digital transformation by combining IoT, AI, and robotics — welding-automation robots, AI-based production-process management, and logistics automation.

Interpretation: Both green certification and automation are upfront investments to clear "future-order eligibility" thresholds. As IMO 2050, EU ETS, and Fuel EU Maritime get stricter, the negotiating power of certified yards becomes asymmetrically stronger.

4. CEO leadership — Vice Chairman Choi Sung-ahn

Official fact: Joined Samsung Engineering in 1989, with 30+ years in plant engineering. Took over Samsung Engineering as CEO in 2018, returning a heavily loss-making company to profitability — a documented track record of crisis management. Current vision: "a technology-centric, 100-year company."

- Selectivity: Quality over quantity — focus on high-value vessel types and offshore. Exited the low-price race in favor of selective, margin-first orders.

- Innovation: A "FEED to EPC" strategy with engagement from the basic-design stage, plus modular construction.

- ESG and safety: Strengthening ESG management alongside workplace safety.

Interpretation: The Samsung Engineering turnaround was a pre-validation of large EPC P&L management capability. Because FLNG is essentially a ship-plant hybrid, Choi's plant background is not a coincidence — it is the board's explicit intent.

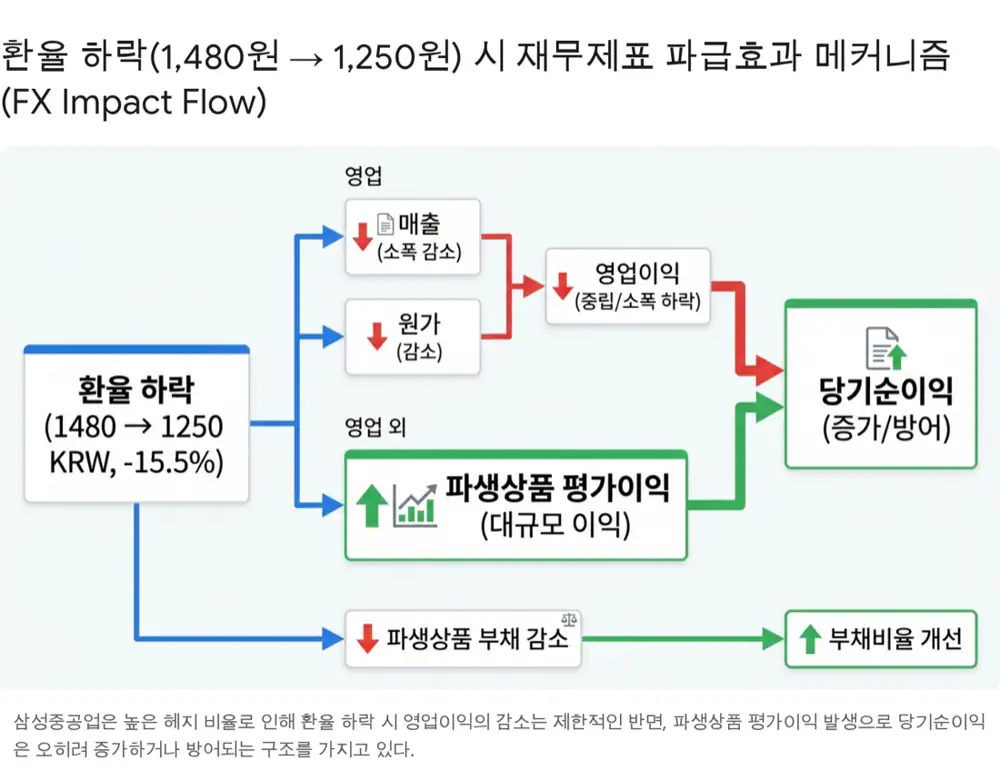

5. Core analysis: FX scenario 1,480 to 1,250 (-15.5%)

The headline of this report. Bottom line: Samsung Heavy maintains a 100% Full Hedge, so a stronger KRW does very little to operating income — instead it triggers large valuation gains in non-operating income, and net income surges. An asymmetric structure.

5.1 The 100% Full Hedge policy

Official fact: While HD Hyundai Heavy and Hanwha Ocean typically hedge 70-80% of contract value, Samsung Heavy locks in close to 100% of expected net USD cash inflows at the time of order, via forward FX contracts.

5.2 Scenario simulation: 1,480 to 1,250 (-15.5%)

Limited decline or neutral

(1) Revenue-recognition specifics — the rate is fixed at order time, so KRW strength does not directly cut backlog revenue. (2) Natural hedge — steel plate and other materials (~20% of cost) are USD-linked imports, so cost of goods drops too.

Large valuation gains

3Q25 end: current derivative financial liabilities KRW 611.06M, non-current KRW 434.62M (residue of past FX-up valuation losses). A move to 1,250 flips liabilities into assets and books gains. Reality check: 3Q25 cumulative derivative trading gains KRW 523.6B and valuation gains KRW 392.1B — actual data showing the size of the asymmetry.

Sharp debt-ratio improvement

FX decline shrinks derivative financial liabilities or flips them to assets, cutting total liabilities. Net-income growth expands retained earnings, lifting equity. The 2024 year-end 358.6% debt-to-equity stabilizes quickly in the scenario.

5.3 Wrap-up: KRW strength is an opportunity, not a crisis

A 1,250 environment is more likely a positive momentum for Samsung Heavy than a fundamental shock — via (1) a net-income surge from derivative valuation gains, and (2) financial-structure improvement from lower FX liability marks. The long-term watch item: if 1,250 persists, USD-denominated newbuild prices come under pressure, eroding pricing competitiveness over time.

6. 2026 outlook and investment strategy

6.1 2026 industry — the second LNG wave

Official fact: 2025 was a wait-and-see year for LNG carriers due to the US election and tariff politics. With the new administration's energy-security stance, FIDs on the delayed North American LNG export projects (CP2 Ph.1, Rio Grande T4/T5 etc.) are expected to start clearing from 2026. Clarksons forecasts global 100K+ cbm LNG carrier orders to reach 100 vessels in 2026, double the 50 of 2025. By 2030, roughly 259 LNG carriers aged 20+ years will need replacement.

Interpretation: 50 to 100 is more than a demand rebound — it's the catch-up of 2025's deferred demand plus the genuine kickoff of the replacement cycle. Samsung Heavy, as a long-time LNG-carrier leader, is positioned as the biggest beneficiary of the replacement wave.

6.2 Geopolitical tailwind: spoils of the US-China conflict

Official fact: USTR plans to impose port-call fees on China-built ships from October 2026. Korean shipbuilders' benefit is set to materialize.

Interpretation: In segments like containerships where Chinese yards leaned on price aggression, the price advantage gets neutralized — and orders concentrate at top-tier Korean yards with proven tech and delivery reliability.

6.3 Risk checklist

Steel plate prices

Steel plate is a large share of build cost; price increases pressure margins. Monitor iron-ore prices and pricing negotiations with POSCO, Hyundai Steel and other suppliers.

Labor shortage

Growing backlog could sustain skilled-worker shortages. The real test is whether smart-yard automation and expanded foreign-worker programs deliver in practice.

Russia Zvezda

Arbitration ongoing in Singapore over the cancelled Russian Zvezda contract. Contingent risk around advance-payment refund and damages remains. Related liabilities of KRW 895.3B recognized as of 3Q25 end.

7. Conclusion

Samsung Heavy defends industry volatility and macro uncertainty with two weapons: FLNG dominance and a full FX hedge. 2025 is on track to beat guidance, and 2026 should see a steeper growth slope as LNG orders restart. The 1,480 to 1,250 scenario is an opportunity for non-operating gains and financial-structure improvement, not a crisis.

Bottom line: rather than fixating on short-term FX swings, the actionable lens is medium-term — focus on structural earnings power and the unmatched marine franchise. (Backlog: ~USD 28.2B.)

Sources

- Original Naver blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224121550666

- 1. 삼성중공업, 암모니아 추진선 인증으로 비롯된 성장 기대와 주가 상승세 지속 - Goover: https://seo.goover.ai/report/202509/go-public-report-ko-dcb4baf2-b4db-4f58-9558-db7e9d4597f5-0-0.html

- 2. 삼성중공업, SMR 설비·디지털 트윈 자율운항 기술 선봬 - 한국일보: https://www.hankookilbo.com/News/Read/A2023090414380002354

- 3. 삼성중공업의 주가 하락과 스마트 조선소 추진의 투자 가치 분석 - Goover: https://seo.goover.ai/report/202507/go-public-report-ko-e393893e-4885-45c2-8960-5f3ad5c5636a-0-0.html

- 4. 삼성중공업 거제조선소 Outdoor AP 구축 - Samsung: https://images.samsung.com/is/content/samsung/p5/sec/business/network/publication/case-study/CaseStudy_Samsung-Heavy-Industries.pdf

- 5. [Who Is ?] 최성안 삼성중공업 대표이사 부회장 - 비즈니스포스트: https://www.businesspost.co.kr/BP?command=article_view&num=373160

- 6. 선장 바뀐 삼성중공업, 환골탈태 명 받았다 [biz-플러스] - Daum: https://v.daum.net/v/20231201065013622

- 7. 삼성중공업 기나긴 적자 고리 끊어낸 최성안 - 씨저널: https://www.c-journal.co.kr/articleView?num=353

- 8. 최성안 삼성重 부회장 "책임 경영 이끄는 100년 기업될 것" - 뉴시안: http://www.newsian.co.kr/news/articleView.html?idxno=80471

- 9. 삼성중공업 '지속가능경영보고서 2025' 발간 - 조선비즈: https://biz.chosun.com/industry/company/2025/06/25/Q3JFIIWG3NHKRHGDADNZSHAB5I/

- 10. Samsung Heavy Industries benefits from exchange rate drop with 100% hedge strategy - Chosun Biz: https://biz.chosun.com/en/en-finance/2025/05/07/X4TXAASLNJCSRO62VHN2Y7L74I/

- 11. 삼성중공업, FLNG 경쟁력에 이익 성장 기대 - 중앙이코노미뉴스: https://www.joongangenews.com/news/articleView.html?idxno=439872

- 12. 하이록코리아, 세계 점유율 50% 삼성중공업 FLNG 수주 직수혜 - 프라임경제: https://m.newsprime.co.kr/section_view.html?no=710158

- 13. [특징주] 삼성중공업, 'FLNG' 기대감에 10년 만에 최고가 - 조선비즈: https://biz.chosun.com/stock/stock_general/2025/02/19/REPY4J2CRFG5BLBHRCGIHH6GHA/

- 14. 삼성중, 11개월 연속 흑자… FLNG 수주로 실적 상승세 '탄탄' - 해사신문: http://www.haesanews.com/news/articleView.html?idxno=143810

- 15. [K조선 기술 초격차③] 삼성重, 아프리카도 캐나다도 반한 FLNG 능력 - 그린포스트코리아: https://www.greenpostkorea.co.kr/news/articleView.html?idxno=301548