DEEP RESEARCH · HANWHA OCEAN

Hanwha Ocean: Structural Turnaround and FX Sensitivity

A combined view of 3Q25 earnings, the KRW 1,480-to-1,250 FX scenario, and the Philly Shipyard strategy

0. Bottom line first

My conclusion is that a move in USD/KRW from 1,480 to 1,250 can pressure reported operating profit, but it should not be automatically treated as impairment of intrinsic value because forward hedges and natural raw-material hedges cushion the impact.

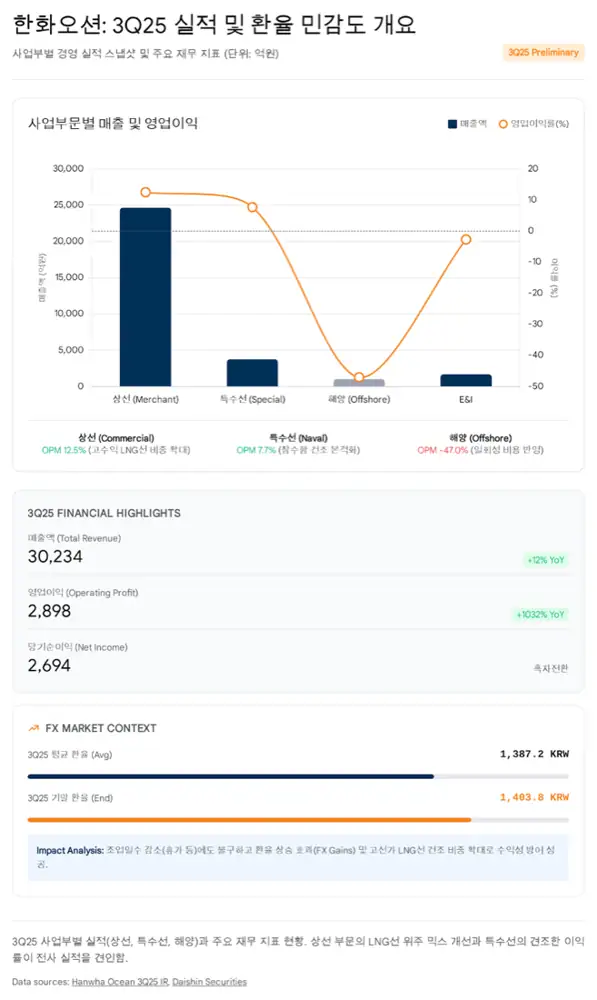

Official fact: The source reports 3Q25 consolidated revenue of KRW 3.0234tn, operating profit of KRW 289.8bn, and OPM of 9.6%. The commercial-vessel segment posted revenue of KRW 2.4639tn, operating profit of KRW 307.1bn, and a 12.5% margin.

Interpretation: The real issue is not short-term FX. It is the qualitative change driven by high-priced LNG carriers, naval vessels, a U.S. shipbuilding base, and smart-yard productivity.

LNG mix improvement

Revenue recognition from high-priced LNG carriers is lifting profitability.

MRO and submarines

Jangbogo-III Batch-II work and Philly Shipyard support naval expansion.

Hedge structure

Dollar-sell/won-buy forwards and lower imported raw-material costs cushion FX shocks.

1. 3Q25 earnings: quality of the turnaround

The source sees Hanwha Ocean in 4Q25 as standing at one of the most important strategic inflection points since joining Hanwha Group. The Global Ocean Solution Provider vision, inorganic expansion, commercial-vessel margin recovery, and naval growth confirm the return to profitability.

| Segment | 3Q25 source result | Core interpretation |

|---|---|---|

| Consolidated | Revenue KRW 3.0234tn, OP KRW 289.8bn, OPM 9.6% | Revenue down about 8% QoQ due to vacation and Chuseok workday effects, but up 12% YoY |

| Commercial vessels | Revenue KRW 2.4639tn, OP KRW 307.1bn, margin 12.5% | Lower low-priced container-ship mix, higher LNG carrier share, average FX of KRW 1,387 |

| Naval and special ships | Revenue KRW 375bn, OP KRW 28.7bn, margin 7.7% | Revenue up 58% QoQ as Jangbogo-III Batch-II hulls 1 and 2 accelerate |

| Offshore | Revenue KRW 102.4bn, operating loss KRW 48.1bn, margin -47.0% | Petrobras P-79 FPSO accident-related delay and provisions |

Interpretation: Commercial and naval drive earnings while offshore one-off costs drag. The persistence of profit therefore depends on the high-value LNG backlog and naval order expansion.

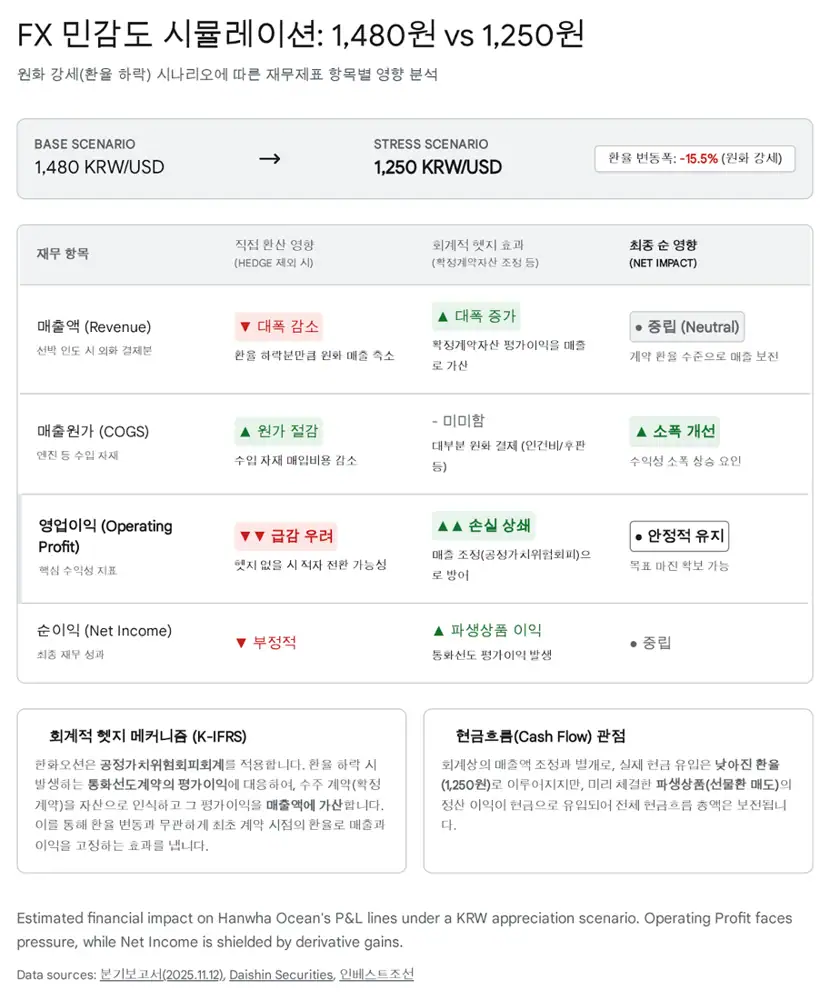

2. FX sensitivity: from KRW 1,480 to 1,250

Shipbuilders contract most vessels in U.S. dollars, so a weaker USD/KRW rate reduces translated won revenue. But part of the cost base, including iron ore and coking coal linked to steel plate, also moves in dollars, creating cost relief when the won strengthens. Won-denominated fixed costs such as labor, power, and domestic equipment do not fall, so operating leverage can work in reverse.

| Scenario | Source calculation | Accounting impact |

|---|---|---|

| Revenue translation | USD 1bn quarterly revenue equals KRW 1.48tn at 1,480 and KRW 1.25tn at 1,250 | About KRW 230bn reduction in translated revenue |

| Operating profit | Won fixed costs do not fall with translated revenue | OPM pressure |

| Derivatives | Dollar-sell/won-buy forward contracts gain value | Financial income and derivative valuation gains defend net income |

| Natural hedge | Steel-plate-related raw materials are around 20% of vessel cost | Imported raw-material costs fall in won terms |

Official fact: The source explains that Hanwha Ocean uses currency forwards to lock future cash flows at the ordering-date exchange rate, and that a fall in USD/KRW raises the value of dollar-sell/won-buy positions.

Interpretation: Operating profit may look weaker, but hedging works at the net-income and cash-flow level. However, KRW 1,250 can hurt new-order competitiveness, so existing backlog and new pricing negotiations should be analyzed separately.

3. Strategic pillars: LNG, ammonia, and smart yards

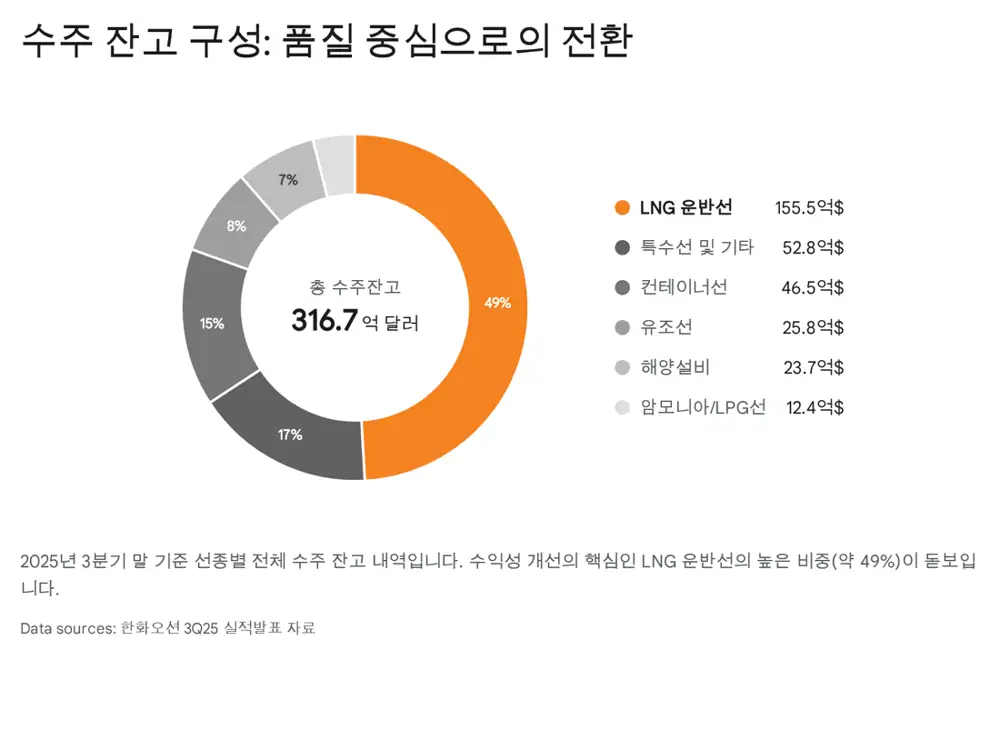

Hanwha Ocean is trying to move from shipbuilding alone into energy value chains and defense infrastructure. The source interprets its investment in U.S. LNG developer NextDecade as a strategic move to pre-empt LNG carrier orders from the Rio Grande LNG project.

Ammonia-powered eco-ships are another axis. IMO 2050 carbon-neutrality rules and stricter EU environmental regulation stimulate fleet replacement demand, and Hanwha Ocean is trying to secure future zero-carbon ship standards. The high LNG-carrier share in backlog supports the visibility of revenue and profit over the next three to four years.

4. Philly Shipyard: Jones Act and MRO market

The Philly Shipyard acquisition is Hanwha Ocean's geopolitical bet. The Jones Act requires vessels moving cargo between U.S. ports to be built in the U.S., owned by Americans, and crewed by Americans. That protectionist wall has blocked foreign shipbuilders from direct access to the U.S. market.

By acquiring Philly Shipyard, Hanwha Ocean obtained a local U.S. production base. The source interprets this as a passage right for the first Asian shipbuilder to enter the U.S. merchant and government-vessel market directly. More important is the U.S. Navy MRO market, estimated in the source at about KRW 20tn. With U.S. yard capacity tight, Philly Shipyard could become a forward base for naval MRO and future new-build combatants.

5. Risks and governance

- Trump 2.0 America First policy is double-edged: defense-cost sharing and tariffs are threats, while allied naval build-up against China and U.S. LNG exports are opportunities.

- Labor shortages are a structural risk for Korean shipbuilding. The key is how quickly foreign labor and smart yards become effective on site.

- The appointment of CEO Kim Hee-chul is interpreted as bringing Hanwha Group's energy and chemicals experience into shipbuilding and drawing group support around Vice Chairman Kim Dong-kwan.

6. Investor conclusion

A move from KRW 1,480 to 1,250 can shake short-term financial statements, but derivative hedges and lower imported raw-material costs can absorb much of the shock. I care more about LNG-centered commercial margins, U.S. market and MRO entry through Philly Shipyard, and smart-yard plus eco-ship technologies.

If these three pillars hold, Hanwha Ocean has room to be re-rated from a simple cyclical shipbuilder into a structural growth company tied to global security and energy transition.

Sources

- 원문 / Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224121468724

- Daishin Securities Hanwha Ocean report: http://money2.daishin.com/m_file/file/271/55335_Daishin%20Securities_Hanwha%20Ocean%20(042660%20KS%20Oct%2014,%202025).pdf

- Chosun government FX article: https://www.chosun.com/english/market-money-en/2025/12/16/ZKMC6FZAZZGGBCHO36YVZB2VDA/

- Invest Chosun exporter hedging article: https://www.investchosun.com/site/data/html_dir/2025/12/19/2025121980117.html

- Chosunbiz exporter hedging article: https://biz.chosun.com/en/en-policy/2025/12/16/TJEDYRKUPRBVBBGVWEPBK7PW5Y/

- Ship Technology Hanwha Philly article: https://www.ship-technology.com/news/south-korea-hanwha-group-5bn-philly-shipyard/

- Hanwha $5bn Philly Shipyard investment release: https://www.hanwha.com/newsroom/news/press-releases/hanwha-announces-5-billion-philly-shipyard-investment-as-part-of-south-koreas-commitment-to-us-shipbuilding-growth.do

- Hankook Ilbo Philly Shipyard analysis: https://www.hankookilbo.com/News/Read/A2024062113040005090

- Invest Chosun MRO market article: https://www.investchosun.com/site/data/html_dir/2025/08/29/2025082980171.html

- Invest Chosun Hanwha Ocean turnaround article: https://www.investchosun.com/site/data/html_dir/2025/01/24/2025012480224.html

- Hanwha Philly Shipyard feature story: https://www.hanwha.com/newsroom/news/feature-stories/how-hanwha-philly-shipyard-is-supporting-americas-maritime-resurgence.do

- MK politics article: https://www.mk.co.kr/en/politics/11505469

- Goover Philly Shipyard report: https://seo.goover.ai/report/202508/go-public-report-ko-64fe6168-4949-4a4d-a666-810884f0a788-0-0.html

- BusinessPost Kim Hee-chul profile: https://www.businesspost.co.kr/BP?command=article_view&num=401530

- Goover Hanwha Ocean leadership report: https://seo.goover.ai/report/202501/go-public-report-ko-0932bcbf-cf6d-4a96-bb4a-d54673aab3ad-0-0.html