DEEP RESEARCH · HD Hyundai Heavy Industries

HD Hyundai Heavy Industries: shipbuilding supercycle, merger synergies, and FX sensitivity

A fundamental review centered on high-value backlog, defense/MRO optionality, and won-dollar scenarios

0. Bottom line first

My view is that backlog quality, merger synergy, and naval/MRO expansion matter more than short-term FX moves.

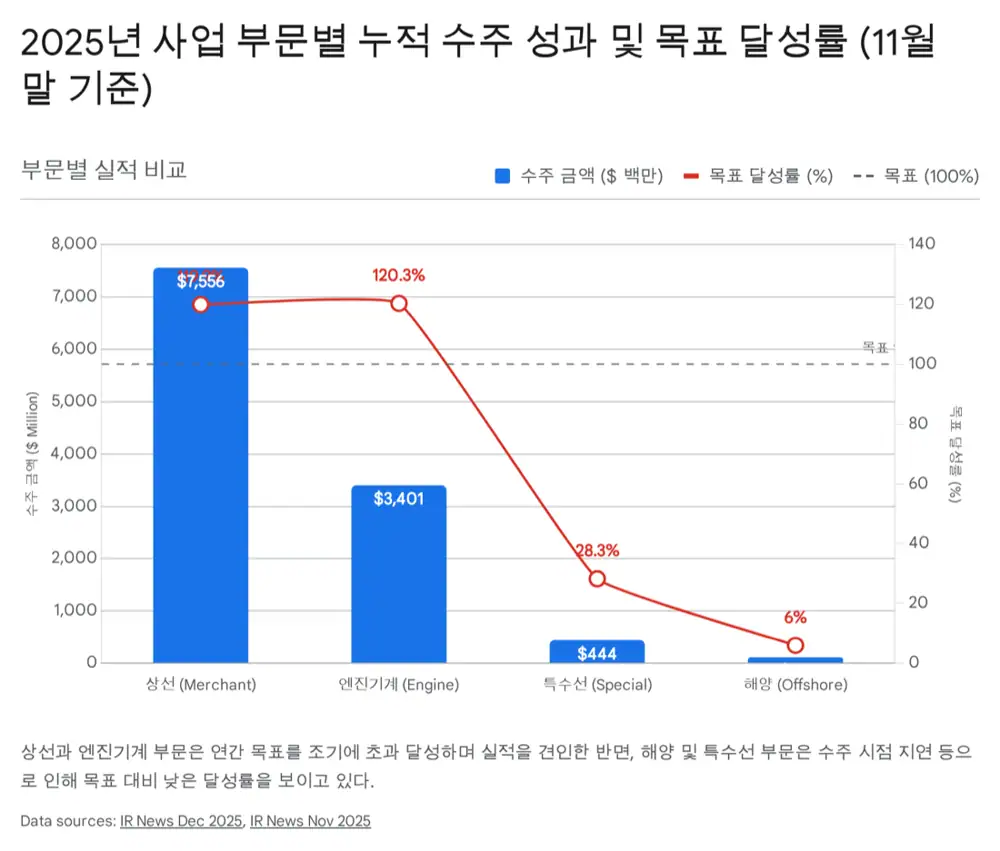

Official fact: The source cites USD 7.556 billion of commercial-ship orders as of end-November 2025, 119.9% of the USD 6.3 billion annual target and up 35.8% year on year. It also cites 47 LNG carriers, 40 containerships, six new tanker orders in November, and 18 tankers in backlog.

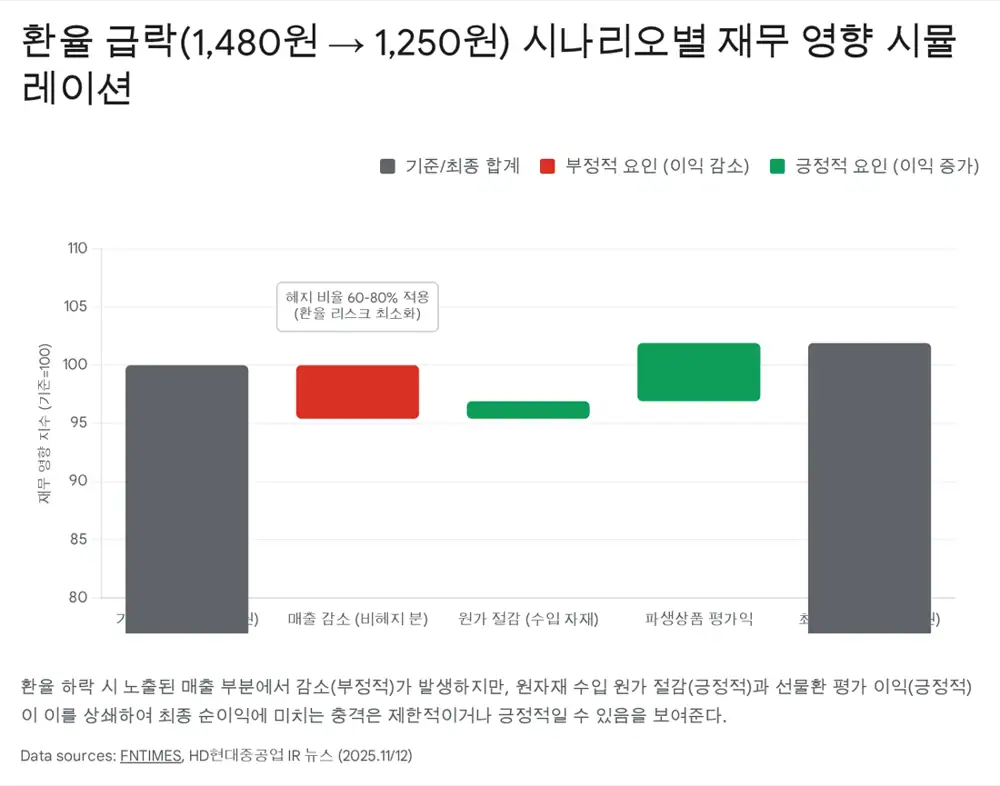

Interpretation: Even if KRW/USD moves from around 1,480 to 1,250, hedging and derivative gains make it hard to call this fundamental impairment.

USD 7.556bn

Commercial-ship orders exceeded the target.

KRW 1,480 → 1,250

The source estimates a 4.65% revenue drag under 30% exposure and 15.5% FX decline.

Defense/MRO

U.S. Navy MRO and naval integration can support a defense premium.

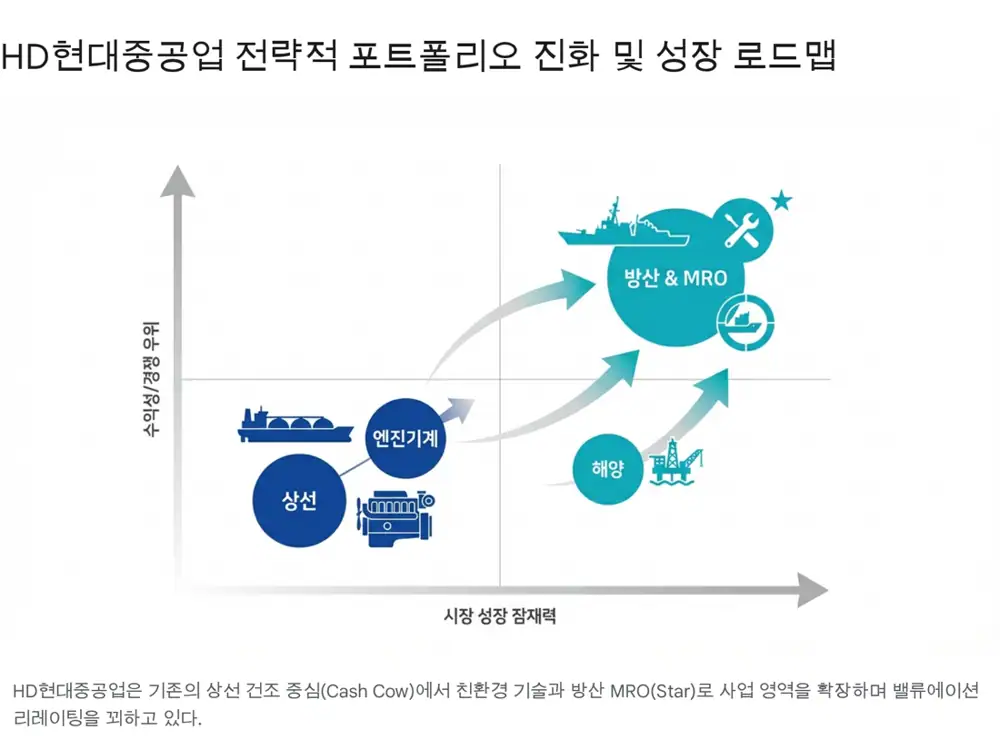

1. Industry cycle and strategic position

The current upcycle is driven by carbon neutrality, energy security, and fleet replacement, not just cargo growth. HD Hyundai Heavy Industries combines LNG carriers, VLACs, eco containerships, engine machinery, and naval vessels.

2. Merger and restructuring

The HD Hyundai Mipo merger means integrated yard operations, stronger purchasing power, design/R&D standardization, and naval capability integration. Overseas bases such as HD HVS and HD HHIP can support global production optimization.

3. Segments and FX scenario

| Item | Source number | Investment read |

|---|---|---|

| Commercial orders | USD 7.556bn, 119.9% of target | High-priced revenue conversion is key. |

| LNG carriers | 47-vessel backlog | Shows quality secured work. |

| Engine machinery | USD 3.401bn, 120.3% of target | An earnings stabilizer. |

| FX | 70% hedged, 30% exposed assumption | Operating pressure and non-operating derivative gains must be viewed together. |

4. Financials and re-rating conditions

The source estimates net cash including major subsidiaries at about KRW 8 trillion as of Q3 2025 and cites P/B around 1.0-1.2x. Re-rating requires defense-premium recognition, double-digit OPM after high-priced orders dominate revenue from 2026 onward, and real orders from ammonia propulsion or autonomous vessels.

5. Investment view

I would monitor newbuild pricing, conversion of high-value backlog into revenue, and naval export/MRO news flow.

Sources

- Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224121467647

- Seoul Finance: https://www.seoulfn.com/news/articleView.html?idxno=615961

- Sisajournal: https://www.sisajournal.com/news/articleView.html?idxno=349592

- Kyosu: http://www.kyosu.net/news/articleView.html?idxno=151157

- HD HHI Welcome: https://www.hhi.co.kr/en/company/greeting

- Chosun English: https://www.chosun.com/english/industry-en/2025/12/01/5RZIKX5S5RDN7NGQBYI63JTHFM/

- LR: https://www.lr.org/en/knowledge/press-room/press-listing/press-release/2025/lr-approves-hd-hyundai-heavy-industries-forward-accommodation-lng-carrier-design/

- Chosun: https://www.chosun.com/economy/industry-company/2025/11/24/2LVXQREGW5AOPGJAXK63IZGNZM/

- MarineLink: https://www.marinelink.com/news/hmm-places-b-order-eight-ultralarge-532800

- Google Drive PDF: https://drive.google.com/open?id=19cVO4tIggibvx2bVTNJy9rTSTDyN6L8J

- HD KSOE PDF: https://hdksoe.co.kr/upload/files/2025/08/f000e662-811d-4082-844d-1fb368a1810b.pdf

- DBRITZ: https://dbritz.kr/GeneralNews/?bmode=view&idx=167220327

- YIG SOKHA PDF: https://drive.google.com/open?id=1km6sBxvsEI2cMz3xrQDWZewzfQBc7IQy

- FNTimes: https://www.fntimes.com/html/view.php?ud=20250417150432476141825007d_18

- Alpha Spread: https://www.alphaspread.com/security/krx/329180/investor-relations/earnings-call/q3-2025