DEEP RESEARCH · KOREAN AIR

Korean Air: Merger Synergy and FX/Oil Sensitivity

A translated report tying 3Q25 weakness, Asiana integration, and high-KRW/USD risk into one framework.

0. Bottom line first

Korean Air has a short-term headwind from high FX and a structural opportunity from Asiana integration. 3Q25 showed peak-out risk, but the bigger question is whether merger synergy appears in 2026-2027 numbers.

3Q25 slowdown

Standalone revenue was KRW 4.0085 trillion, operating profit was KRW 376.3 billion, and operating margin fell to 9.4%.

FX burden

On December 24, 2025, KRW/USD was threatening the 1,480 level, pressuring dollar costs and FX translation losses.

Mega carrier

The Asiana integration targets scale economies, duplicate cost removal, and stronger hub competitiveness.

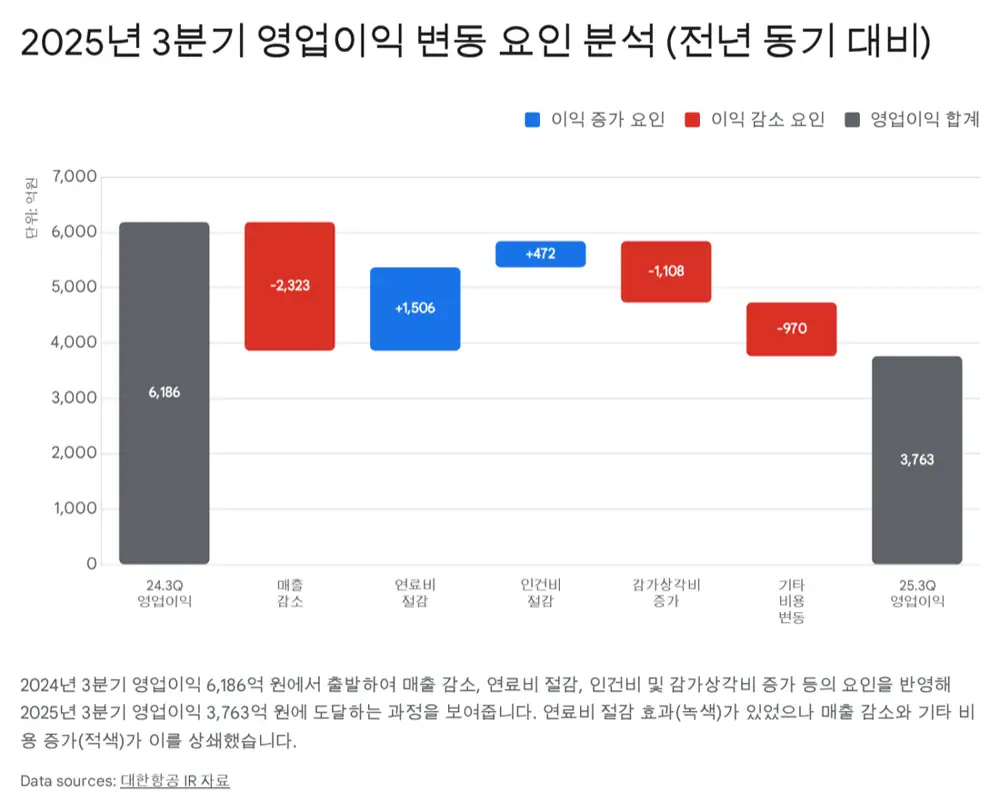

1. 3Q25 earnings diagnosis

Official fact: The source reports standalone 3Q25 revenue of KRW 4.0085 trillion and operating profit of KRW 376.3 billion. Revenue fell 5.5% year over year, while operating profit dropped 39.2% from KRW 618.6 billion. Operating margin fell from 14.6% to 9.4%.

| Item | 3Q25 | YoY | Source interpretation |

|---|---|---|---|

| Revenue | KRW 4.0085T | -5.5% | Yield normalization and holiday timing shift |

| Operating profit | KRW 376.3B | -39.2% | Cost rigidity and lower profitability |

| Passenger revenue | KRW 2.4211T | -7.5% | Endemic base effect fades, supply expands |

| Cargo revenue | KRW 1.0667T | -4.7% | Weak economy and more belly cargo supply |

Interpretation: This was not just seasonality: passenger yields, cargo rates, and fixed-cost growth all moved against earnings.

2. Cost structure: cheaper oil offset by FX and fixed costs

3Q25 fuel cost was KRW 1.0156 trillion, down 12.9% or KRW 150.6 billion from KRW 1.1662 trillion a year earlier. Jet fuel prices fell 8% and fuel consumption declined 6%, but a 2% YoY FX rise offset part of the benefit.

- Price effect: An 8% decline in jet fuel prices drove the main saving.

- Quantity effect: Fuel consumption fell 6%, helped by more efficient aircraft such as the B787-10.

- FX effect: Fuel is dollar-settled, so KRW weakness directly reduces the oil-price benefit.

- Fixed-cost effect: Other operating costs rose 6.5% to KRW 2.6166 trillion, with depreciation up 27% after new aircraft introductions.

3. FX and oil sensitivity

The source says KRW/USD was threatening the 1,480 level on December 24, 2025, pressuring aircraft lease payments, fuel, maintenance, insurance, and overseas airport fees. Korean Air held about $4.8 billion of net foreign-currency debt at the end of 3Q25, making FX a direct non-operating earnings variable.

| Variable | Source number | P&L direction |

|---|---|---|

| Net FX debt | About $4.8B | KRW weakness increases translation losses |

| FX translation loss | KRW 175.2B | KRW 202.3B deterioration vs prior-year gain |

| Derivative result | KRW 93.1B gain | Turnaround from KRW 168.2B loss |

| Oil environment | WTI in the $50-60 range referenced | Partly buffers high-FX pressure |

4. Asiana integration and 2026-2027 scenario

2026: transition

PMI costs may slow margin recovery, but the source expects merger effects to push revenue above KRW 25 trillion.

2027: lift-off

Route cleanup, workforce/resource efficiency, and the launch of the integrated LCC could make structural profit improvement visible.

5. Governance and shareholder returns

The source says Hoban Construction affiliates raised their Hanjin KAL stake to 18.46% in May 2025, narrowing the gap with Chairman Cho Won-tae and related parties at 20.13% to 1.67 percentage points. Delta Air Lines' roughly 14.9% stake is viewed as friendly, but further buying could raise volatility.

On shareholder returns, Korean Air changed its articles in March 2025 to determine dividends before setting the record date, and maintains a policy to return up to 30% of standalone net income through fiscal 2026. After the Asiana merger, however, the policy will be reviewed in light of the merged entity's financial stability and integration costs.

6. Investor watchpoints

- Whether KRW/USD breaks 1,500 or high FX persists.

- Whether geopolitical risk drives oil prices sharply higher again.

- Whether labor, mileage, cargo-sale, or Air Incheon integration issues delay PMI synergy.

- Whether 2026-2027 revenue expansion in the merged carrier converts into operating profit.

Sources

- 1. https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224121353304

- 2. https://asianaviation.com/korean-air-sees-revenue-decline-in-q3/

- 3. https://securities.miraeasset.com/bbs/download/2137243.pdf?attachmentId=2137243

- 4. https://www.chosun.com/economy/economy_general/2025/12/24/VZWRXMV6DBBZHKGEETK6DTCLVU/

- 5. https://www.yna.co.kr/view/AKR20251224029500002

- 6. https://www.chosun.com/english/market-money-en/2025/12/09/ZNHQSE6GUNEYNBJRQN5QYD6S3U/

- 7. https://koreajoongangdaily.joins.com/news/2025-05-18/business/industry/Koreas-airline-industry-has-diametric-Q1-with-LLCs-hit-by-forex-turbulence/2308936

- 8. https://koreajoongangdaily.joins.com/news/2025-10-21/business/industry/Korean-Air-Jeju-Air-and-more-see-drop-in-revenue-in-Q3/2425499

- 9. https://www.ebn.co.kr/news/articleView.html?idxno=1692558

- 10. https://ko.tradingeconomics.com/commodity/brent-crude-oil

- 11. https://www.newdaily.co.kr/site/data/html/2025/12/17/2025121700027.html

- 12. https://money2.daishin.com/PDF/Out/intranet_data/Product/ResearchCenter/Report/2025/07/54180_54180_KAL_Earnings_Preview.pdf

- 13. https://www.iata.org/en/iata-repository/publications/economic-reports/global-outlook-for-air-transport-june-2025/

- 14. https://www.koreanair.com/contents/footer/customer-support/notice/2025/2508-infuel

- 15. https://grokipedia.com/page/Proposed_merger_of_Korean_Air_and_Asiana_Airlines

- 16. https://blog.awardfares.com/korean-air-asiana-merger/

- 17. https://m.ekn.kr/view.php?key=20251217021158344

- 18. https://news.einfomax.co.kr/news/articleView.html?idxno=4389856

- 19. https://www.etoday.co.kr/news/view/2470395