DEEP RESEARCH · ORACLE

Oracle: The AI Infrastructure Pivot and Debt-Funded Expansion

A translated research-report view of Genesis Mission, GW-scale data centers, SMR power strategy, and leverage risk.

0. Bottom line first

My read is that Oracle is moving from a database company into an AI foundry. The move is built on very large numbers: $20.535 billion of half-year CAPEX, $523 billion of RPO, GW-scale data centers, and debt-funded execution.

National AI infrastructure

Oracle is framed as an early Genesis Mission collaborator, placing OCI beyond commercial cloud and closer to high-security national AI infrastructure.

Massive clusters

A 131,072-GPU NVIDIA Blackwell cluster and 1GW-plus data-center plan are the core of the demand-capture thesis.

Leverage

Balance-sheet debt can amplify upside if demand converts, but it leaves fixed costs and interest burden if execution slips.

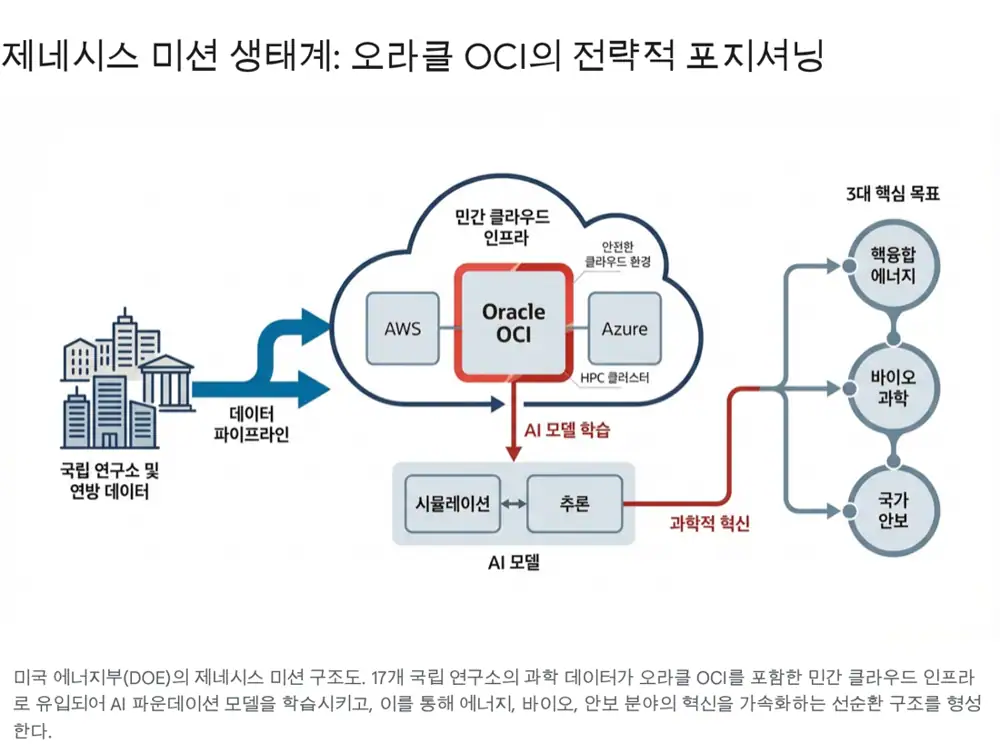

1. Genesis Mission and OCI's strategic role

Official fact: The source says the Genesis Mission was formalized in November 2025 through White House and DOE actions, and that DOE signed MOUs with 24 major technology organizations, with Oracle listed alongside Google, Microsoft, NVIDIA, OpenAI, Anthropic, and others.

Interpretation: OCI is being evaluated not merely as rented compute, but as a possible backbone for secure national science infrastructure combining security, data integration, and HPC.

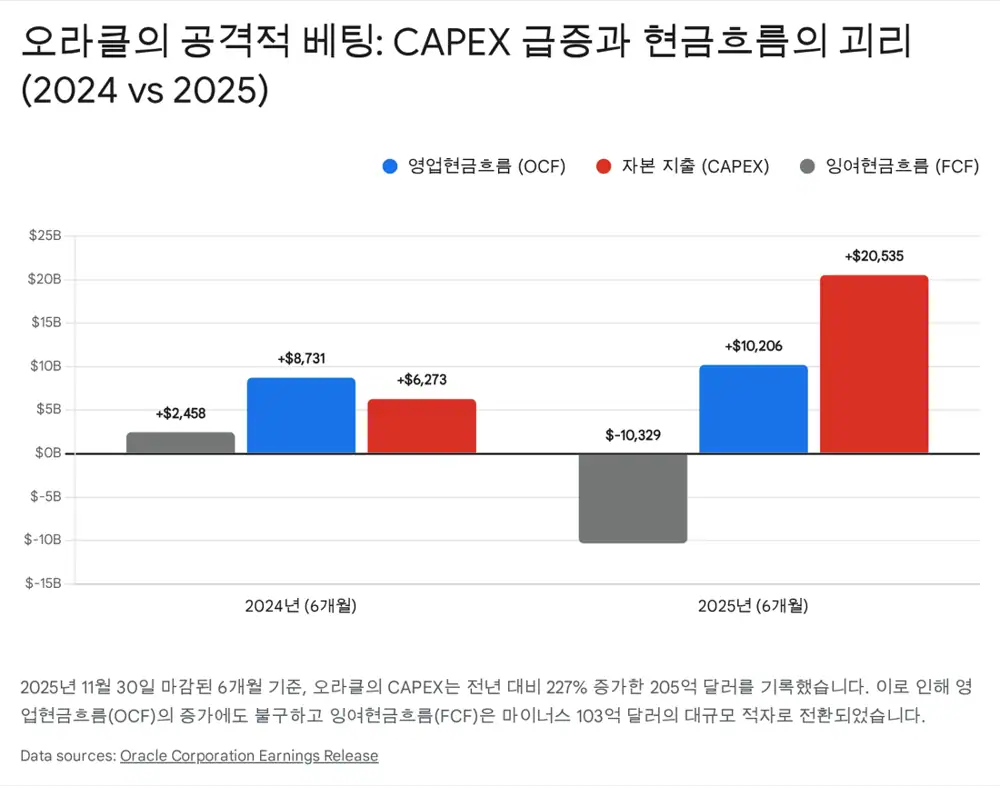

2. CAPEX and data-center expansion

During the first six months of fiscal 2026, Oracle CAPEX reached $20.535 billion, about 3.3 times the $6.273 billion spent in the year-earlier period. The source estimates annual CAPEX could exceed $40 billion if the pace continues.

| Item | Source number | Meaning |

|---|---|---|

| Half-year CAPEX | $20.535B | Investment to capture AI cluster demand |

| Prior-year period | $6.273B | Base for the 3.3x increase |

| GPU cluster | 131,072 Blackwell GPUs | Zettascale infrastructure for OpenAI/xAI-type workloads |

| Data centers | 162 operating or under construction | Largest at 800MW; 1GW-plus planned |

3. Power: the bottleneck in AI infrastructure

The bottleneck is power. The source notes that in dense data-center markets such as Northern Virginia, grid connection queues can stretch for years, pushing Oracle toward a layered power strategy including SMRs.

Power contracts

Use grid access and large PPAs to secure power for immediate deployment.

Site control

Land with power and cooling availability becomes a core data-center asset.

SMR option

Small modular reactors are less about near-term certainty and more about option value for GW-scale AI campuses.

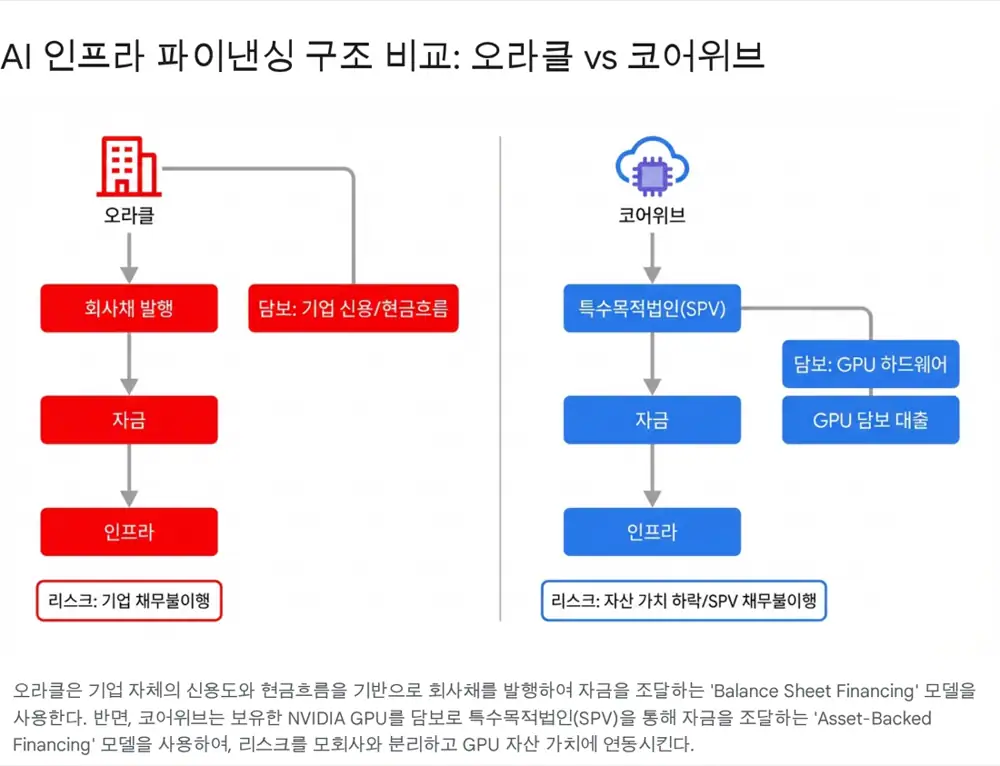

4. Debt financing and the Blue Owl signal

Oracle relies more on corporate credit and company-wide cash flow than CoreWeave-style GPU-backed SPV financing. The source argues that legacy database and ERP businesses remain cash cows able to absorb roughly $1 billion of quarterly interest expense.

Official fact: The source says Oracle discussed equity investment and financing with Blue Owl Capital for a $10 billion Michigan AI data-center project, but Blue Owl withdrew.

Interpretation: This warns that private capital appetite for AI infrastructure is not unlimited. Oracle's future financing terms may become more sensitive to the speed at which RPO turns into revenue.

5. Technical moat and investor watchpoints

OCI's technical moat is bare-metal performance using RDMA over Converged Ethernet, plus multicloud and chip neutrality. Oracle's strategy of putting Exadata inside AWS, Azure, and Google Cloud data centers turns competitors' platforms into demand channels for Oracle Database.

Bull Case

- If $523 billion of RPO converts into revenue in 2026-2027, revenue and operating income could step up together.

- Partnerships with OpenAI and Microsoft support the view that OCI is becoming essential AI infrastructure.

- In a power-constrained world, 1GW-class power options and SMR permits could become scarce assets.

Bear Case

- Debt and annual interest expense approaching $4 billion constrain financial flexibility.

- If financing partners retreat, large data-center projects can be delayed and RPO conversion can slip.

- SMRs carry high technical and regulatory uncertainty and may not support power needs until after 2030.

6. What I would monitor

- The speed of RPO-to-revenue conversion and quarterly cloud revenue growth.

- Whether alternative financing is secured for Michigan and other large data-center projects.

- The timing of FCF recovery and the burden of interest expense.

Sources

- 1. https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224118140699

- 2. https://www.executivegov.com/articles/doe-industry-ai-mou-genesis-oracle-accenture

- 3. https://markets.financialcontent.com/wral/article/marketminute-2025-12-19-oracles-ascent-the-new-north-star-for-enterprise-software-and-ai-integration

- 4. https://markets.financialcontent.com/wral/article/tokenring-2025-12-19-oracles-cloud-renaissance-from-database-giant-to-the-nuclear-powered-engine-of-the-ai-supercycle

- 5. https://www.whitehouse.gov/presidential-actions/2025/11/launching-the-genesis-mission/

- 6. https://www.energy.gov/articles/promises-made-promises-kept

- 7. https://www.ans.org/news/article-7583/white-house-to-consolidate-data-and-research-under-aidriven-genesis-mission/

- 8. https://www.alcf.anl.gov/news/energy-department-launches-genesis-mission-transform-american-science-and-innovation-through

- 9. https://www.energy.gov/genesis-mission

- 10. https://www.energy.gov/articles/energy-department-announces-collaboration-agreements-24-organizations-advance-genesis

- 11. https://www.hpcwire.com/off-the-wire/oracle-and-doe-collaborate-to-accelerate-ai-initiatives/

- 12. https://www.power-eng.com/nuclear/smrs/oracle-designing-data-center-to-be-powered-by-trio-of-small-modular-reactors/

- 13. https://www.tomshardware.com/tech-industry/oracle-will-use-three-small-nuclear-reactors-to-power-new-1-gigawatt-ai-data-center

- 14. https://www.theguardian.com/us-news/2025/dec/18/michigan-data-center-fight

- 15. https://www.morningstar.com/news/marketwatch/2025120949/oracle-is-the-canary-in-the-coal-mine-for-big-techs-debt-fueled-ai-spending-spree

- 16. https://medium.com/@Elongated_musk/gpus-as-collateral-chip-based-abs-acf55ac3f135

- 17. https://www.blackstone.com/news/press/coreweave-secures-7-5-billion-debt-financing-facility-led-by-blackstone-and-magnetar/

- 18. https://www.investing.com/analysis/oracle-feels-pressure-as-rising-debt-complicates-the-ai-data-center-narrative-200671984

- 19. https://www.fudzilla.com/news/memory-and-storage/62236-oracle-s-ai-binge-rattles-markets-as-blue-owl-flies-off