DEEP RESEARCH · SUNAM / HIGH-TEMPERATURE SUPERCONDUCTORS

SuNam: 2G HTS Wire and the Fusion Value Chain

RCE-DR productivity, PLD performance upgrades, power-cable cash flow, and the fusion option in one view

0. Bottom line first

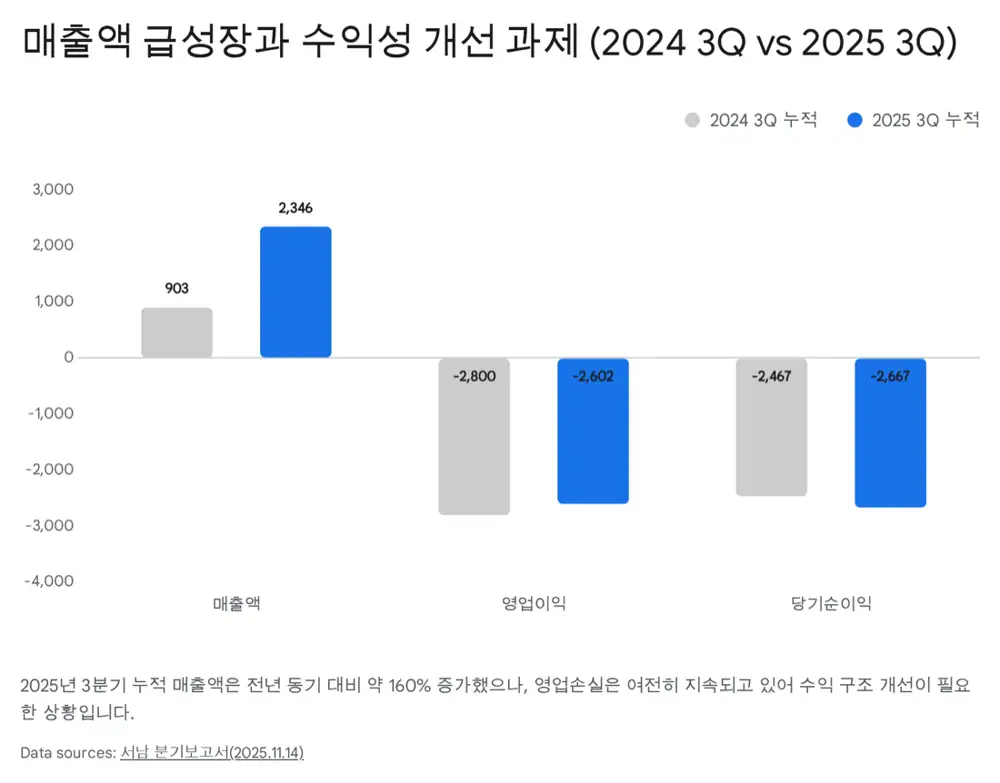

SuNam is a deep-tech company using power cables and equipment exports to support the present while targeting future re-rating through fusion and high-field magnets. Cumulative 3Q25 revenue rose 159.8% YoY to KRW 2.346 billion, but the KRW -2.602 billion operating loss and continuing R&D/CAPEX burden remain the core risk.

Official fact: The source says SuNam was founded in 2004, has developed second-generation high-temperature superconducting wire, and listed on KOSDAQ through a technology-special listing in 2020. The company name SuNam is described as an abbreviation of “Superconductor, Nano and Advanced Materials.”

Interpretation: The investment point is not the superconductivity theme itself. It is whether RCE-DR's productivity advantage becomes real cost competitiveness and whether PLD narrows the high-field performance gap. Only then can SuNam address both power-grid and fusion markets.

1. Identity: materials company plus equipment engineer

SuNam's differentiation is not just producing superconducting wire. The source sees the key edge in its ability to design and build core 2G HTS manufacturing equipment internally, including IBAD and RCE-DR systems.

Interpretation: Internal equipment capability helps process optimization speed, capital cost, and yield improvement. It also creates a separate equipment-export revenue stream. SuNam is a deep-tech materials company, but its model is closer to “materials plus process solutions.”

2. Core technology: RCE-DR speed plus PLD upgrade

2G HTS wire is made by depositing superconducting materials as a thin film on a metal substrate. The source says the industry's core challenge is balancing throughput and performance.

Productivity advantage

MOCVD can produce high-quality wire but carries cost burdens from slower deposition and lower raw-material efficiency. SuNam's RCE-DR uses large-area and fast deposition to create price competitiveness in power cables.

High-field performance upgrade

RCE-DR has been criticized for relatively weaker critical-current density in high magnetic fields. The source says SuNam has installed PLD equipment for medium/high-field wire and is running stabilization tests.

Power grid and fusion together

Combining RCE-DR productivity with PLD performance could let SuNam address both price-sensitive power-cable markets and performance-sensitive fusion/high-field magnet markets.

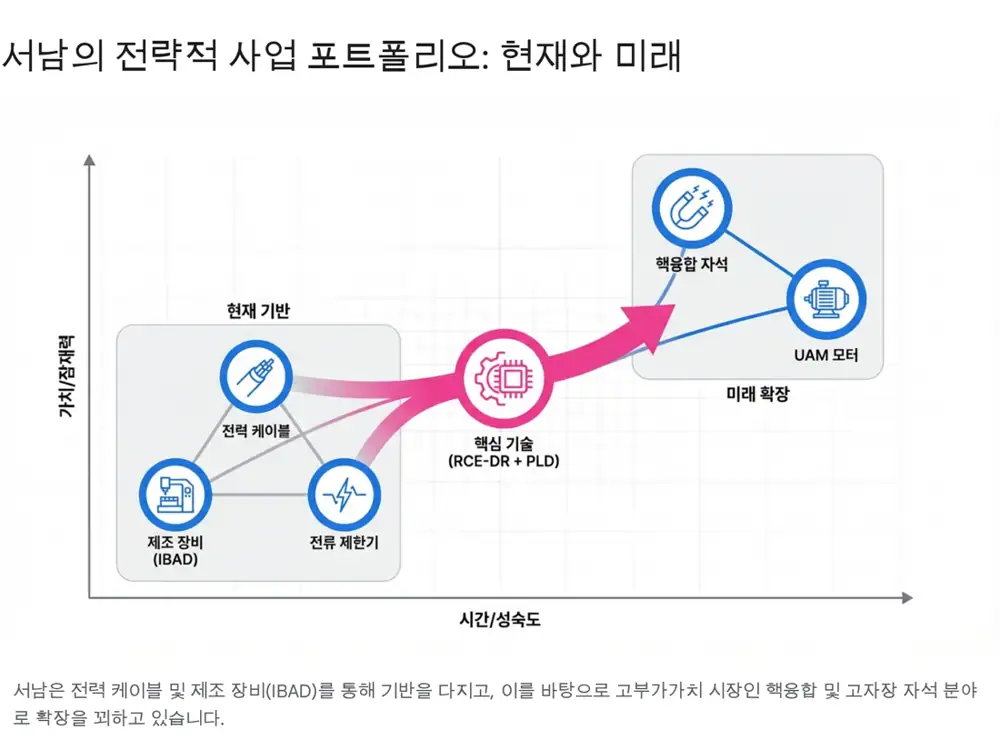

3. Portfolio: cash cow and future growth

| Type | Business/market | Meaning in the source |

|---|---|---|

| Cash cow | Superconducting power cables | The source mentions work with KEPCO and LS Cable and large-scale wire supply for the Munsan-Seonyu superconducting cable project. Urban power demand and data-center expansion are the demand backdrop. |

| Cash cow | IBAD manufacturing equipment | SuNam exports internally developed IBAD equipment to overseas research institutes and companies. The source cites equipment exports as one driver of the 2022 revenue jump. |

| Future growth | Fusion power | Tokamaks need superconducting magnets to create intense magnetic fields. SuNam was selected as a wire supplier for the U.K. STEP project and signed a framework contract, while also maintaining cooperation with CFS in the U.S. |

| Future growth | High-field magnets and applications | Demand can expand in MRI/NMR and lightweight motors for UAM. The source says SuNam's 2023 IR materials raised the magnet-sales target by about 3.7x YoY. |

4. Financials: growth and losses together

Cumulative 3Q25 results show that revenue growth has started, but breakeven and cash flow remain unresolved.

| Metric | Figure | Read-through |

|---|---|---|

| Cumulative revenue | KRW 2.346 billion | Up 159.8% from KRW 903 million a year earlier |

| Export share | 87%, KRW 2.044 billion | Evidence that global customers exist beyond a domestic theme |

| Operating loss | KRW -2.602 billion | Only slightly narrower than KRW -2.800 billion a year earlier |

| Gross loss | KRW -92 million | Manufacturing cost still exceeds selling price, requiring scale and yield stabilization |

| Net loss | KRW 2.667 billion | The source strongly infers that cash burn is continuing |

| R&D | KRW 1.347 billion | About 57% of revenue, an aggressive investment ratio |

Interpretation: SuNam is still a loss-making manufacturer with good technology. Revenue growth alone is not enough; the key is whether yields and costs improve enough after RCE-DR/PLD investment to turn gross profit positive.

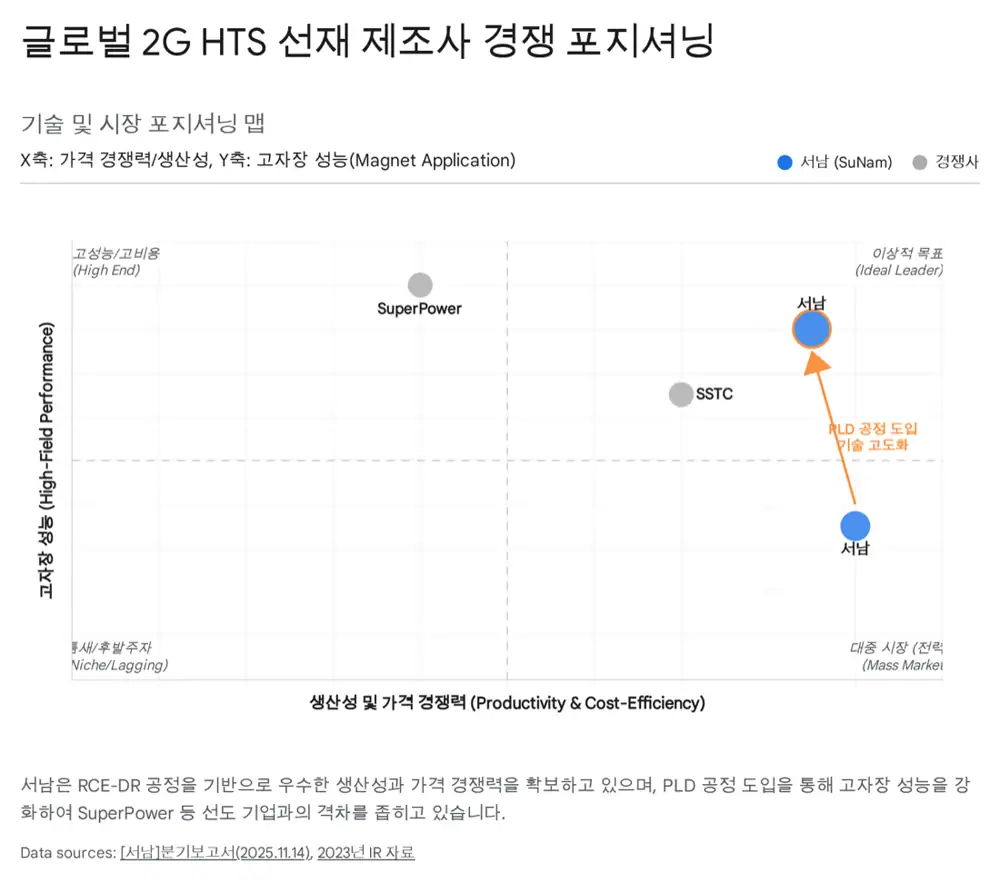

5. Competition and moat

The source says only a handful of companies can mass-produce 2G HTS wire at a commercial level. Main peers are SuperPower in the U.S./Japan camp and Shanghai Superconductor in China.

| Company | Strength | Weakness/variable |

|---|---|---|

| SuperPower | A Furukawa Electric subsidiary using MOCVD, with strong high-field performance and a leading position in fusion and high-field magnets | Relatively high manufacturing cost |

| Shanghai Superconductor | Aggressively expanding capacity on the back of Chinese government subsidies | U.S. and European market entry is constrained by Western de-risking from China |

| SuNam | RCE-DR deposition speed described as 3-5x faster than MOCVD, plus PLD to improve high-field performance | Losses, CAPEX burden, and need for high-field customer validation |

6. Management and partnerships

CEO Moon Seung-hyun is described as a Seoul National University metallurgy graduate and a technocrat who has led superconducting materials since SuNam's founding in 2004. Vice President Lee Ho-yeop is described as overseeing technology and general management.

Official fact: The source says SuNam's corporate research institute is split into materials-development and device-development teams, and that a focused research group of 10 people including executives has completed 17 national projects and holds 67 patents.

- Domestic partners: Through KSTAR, SuNam works with the Korea Institute of Fusion Energy; it also conducts high-field magnet research with Seoul National University and commercial power-cable projects with KEPCO and LS Cable.

- Overseas partners: In addition to U.K. STEP and U.S. CFS, the source mentions NASA, Airbus, Siemens, and a recent competitive bid win from an Indian national research institute.

7. Risks and investment view

Cash burn

Continued operating losses and CAPEX can keep consuming cash. If breakeven is delayed, equity issuance or CB financing cannot be ruled out.

Fusion timeline

Fusion is a long-term growth option, but commercialization timing remains uncertain. Project delays would affect SuNam's expected revenue.

China and global leaders

Chinese low-price competition and performance-gap expansion by leaders such as SuperPower must be watched continuously.

The source views SuNam as a company that should reinvest rather than return capital to shareholders. It says no specific dividend, share-cancellation, or Value-Up program participation was identified.

8. Overall view

SuNam is a classic high-risk, high-return deep-tech investment. The source assigns an investment attractiveness score of 3.5/5.0, with very high growth potential but a need to manage financial risk. The core points are RCE-DR productivity, performance upgrades through PLD, and global references such as STEP, CFS, and NASA.

The indicators I would track are not simple share-price momentum, but major fusion project orders, a turn to positive gross profit, the terms of any new financing, and customer validation of PLD-based high-field wire. If these are confirmed, SuNam can be evaluated not as a theme stock but as a global superconducting first mover.