DEEP RESEARCH · LOTTE ENERGY MATERIALS

Lotte Energy Materials (020150): Structural Transformation and Value-Chain Repositioning

A review of whether the company can offset battery-foil weakness with AI circuit foil, ESS, and next-generation battery materials.

0. Bottom line first

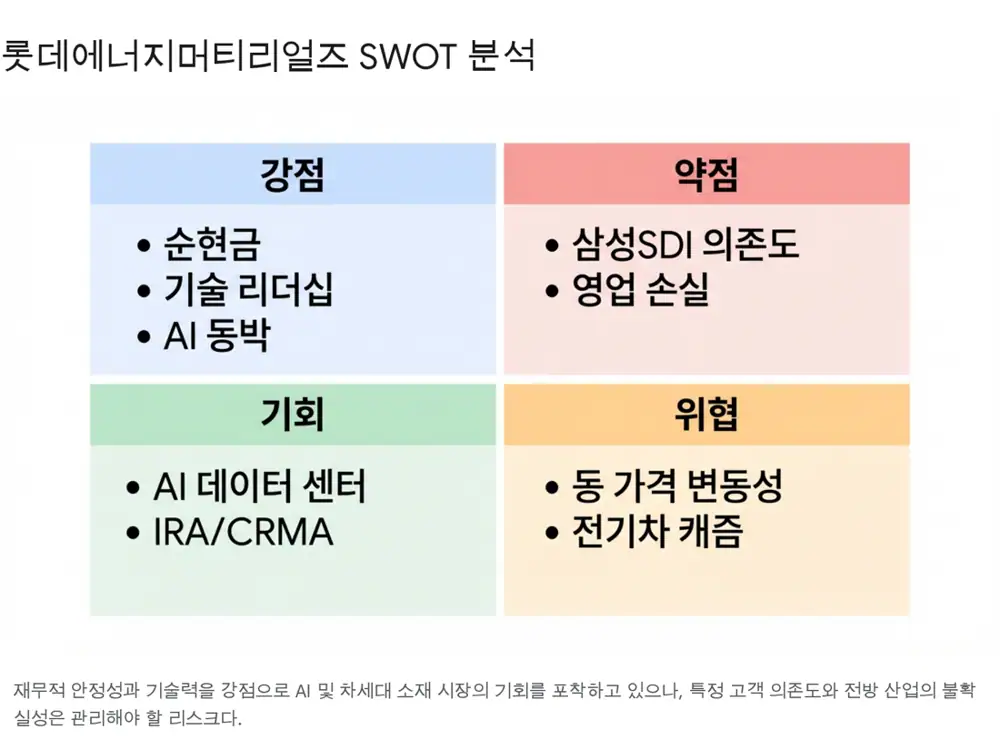

Lotte Energy Materials is suffering from weak short-term earnings during the EV chasm, but its 23.7% debt ratio and -14.9% net debt ratio give it room to pursue a quality pivot toward AI circuit foil and next-generation battery materials.

1. Market backdrop and Q3 2025 results

Official fact: Q3 2025 consolidated revenue was KRW 143.7B and operating loss was KRW 34.3B. EV demand slowdown and OEM inventory adjustment are the main near-term headwinds.

Interpretation: The issue is not only the loss, but the ability to endure it. The source highlights the 23.7% debt ratio and -14.9% net debt ratio as industry-leading financial strength that allows continued CAPEX and R&D during a downturn.

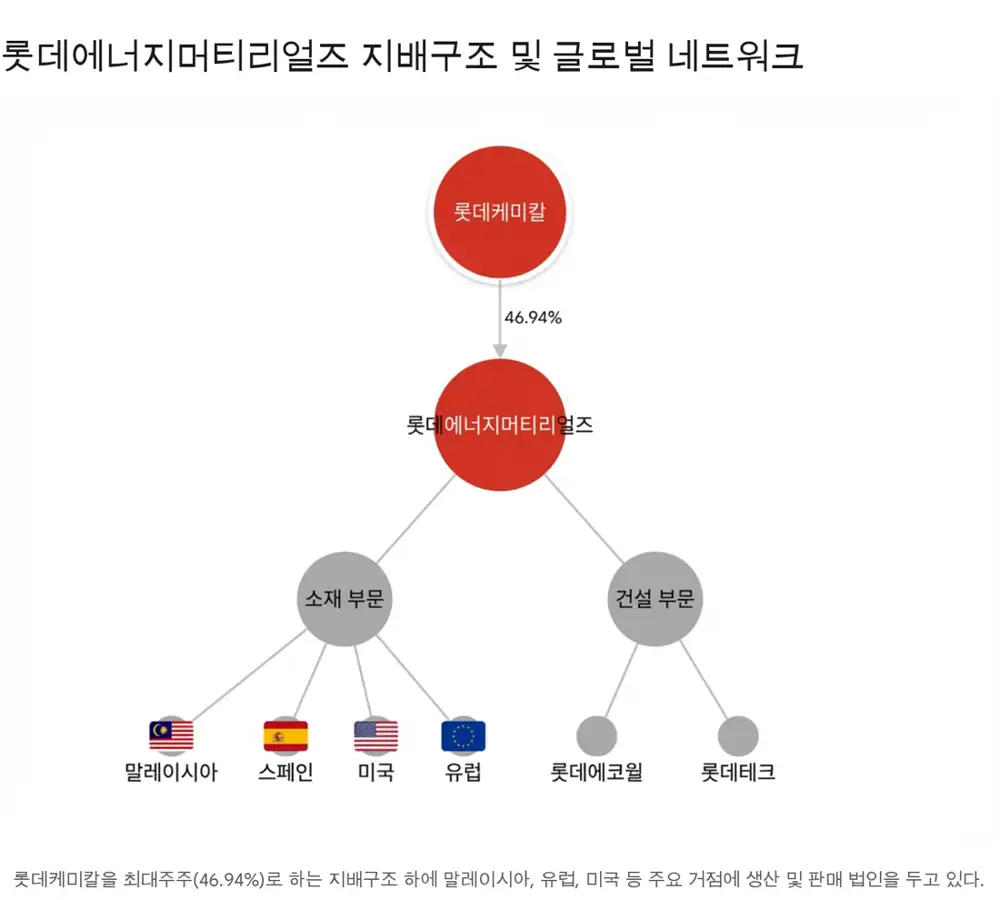

2. Company background and Lotte ownership

The company began as Duksan Metal on August 11, 1987. It became Iljin Materials, listed on KOSPI in 2010, and joined Lotte Group on March 14, 2023 when Lotte Chemical acquired a 53.3% stake.

Official fact: As of Q3 2025, the largest shareholder is Lotte Chemical with a 46.94% stake. The source describes 15 consolidated subsidiaries.

- The materials segment produces and sells elecfoil through sites in Iksan, Malaysia, Europe, Spain, and the U.S.

- The construction segment is led by Lotte Ecowall and has a relatively small group revenue share.

- CEO Kim Yeon-seop is presented as a leader with technology, safety, strategy, management, and ESG experience at Lotte Chemical.

3. Business segments and technology

High-end copper foil

The company focuses on high-strength and high-elongation products such as I2B.

Iksan, Malaysia, Spain

Iksan is the R&D and mother factory, Malaysia provides hydro-powered cost competitiveness, and Spain serves European customers.

HVLP for AI accelerators

Ultra-low-profile foil targets AI servers by reducing signal loss.

4. Customer structure and long-term contracts

The source views Samsung SDI as the key customer and says Lotte Energy Materials supplies roughly 60% of its copper foil demand through a large contract. LG Energy Solution is described as a second major customer whose share rose from about 20% in 2023 to more than 30% after 2024.

5. Strategic pivot to AI and ESS

- The company targets customer approvals from CCL/PCB makers by the end of 2025 and revenue from 2026.

- AI circuit-foil capacity is planned to expand 1.7x in 2026 and 5.7x by 2028.

- ESS foil may help restore utilization at the Malaysia plant because it can support large volumes even with lower technical difficulty than EV foil.

6. Next-generation materials roadmap

- Sulfide solid electrolyte: a 70-ton-per-year pilot line was completed at Iksan Plant 2 in September 2024, with mass production targeted after 2026.

- LFP cathode: a 1,000-ton-per-year pilot plant was completed in December 2024, targeting ESS and entry EVs from 2026.

- Silicon anode: technology was secured through an investment in French startup Enwires, with production planned for 2027.

7. Risks and final investment points

| Risk | Source detail | Response angle |

|---|---|---|

| Copper price | Copper wire purchase price rose about 22%, from KRW 11,125/kg in 2023 to KRW 13,595/kg in Q3 2025 | Surcharge pass-through, supplier diversification, more premium products |

| Overseas sites | Malaysia and Spain expansion increases FX and policy exposure | Flexible North America timing through LOTTE EM America |

| Construction liabilities | Lawsuits of about KRW 750M and KRW 870M are cited | Financial impact looks limited, but reputation risk should be monitored |

My final focus is financial stability, the shift into the AI hardware value chain, and pilot lines for next-generation materials such as solid electrolytes.