DEEP RESEARCH · ISU SPECIALTY CHEMICAL

ISU Specialty Chemical: Precision-Chemical Moat and Solid-State Battery Li₂S Research

A combined review of the TDM/NDM oligopoly cash engine and the Li₂S commercialization roadmap.

0. Bottom line first

ISU Specialty Chemical is in a transition. The precision-chemical core is going through cycle and pricing pressure, while lithium sulfide (Li₂S) is valued as an option on solid-state battery commercialization. The key question is whether H₂S handling know-how can transfer from the TDM moat to the Li₂S moat.

Official fact: The source says the company was spun off from ISU Chemical on May 1, 2023 and completed vertical integration of production and distribution by absorbing ISU Exachem’s precision-chemical business in April 2024 through a small-scale merger.

1. Two pillars: legacy and future

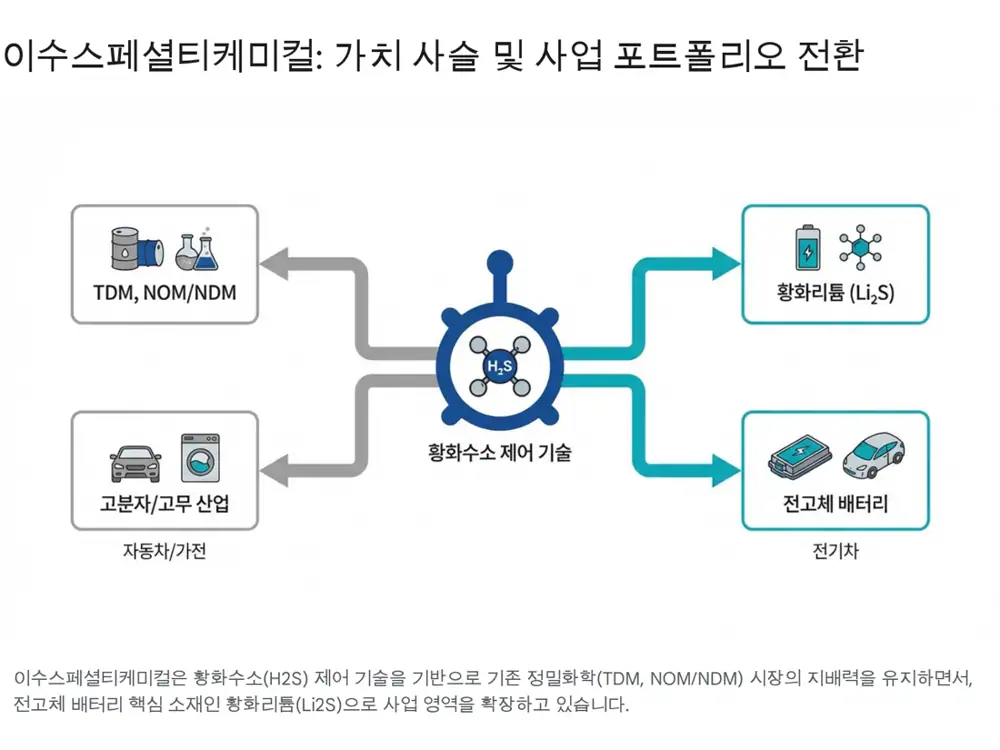

TDM, NOM, NDM

As one of the global top three makers in specialty chemicals, the company maintains an oligopolistic position and cash-generation base.

H₂S handling

Hydrogen sulfide is toxic, corrosive, and explosive, making safety and reaction-control capabilities a barrier to entry.

Lithium sulfide Li₂S

Presented as a starting material for sulfide solid electrolytes and a material that can influence solid-state battery performance and economics.

As of the end of September 2025, capital was KRW 30.2 billion, and the source says ISU Corp., Chairman Kim Sang-beom, and related parties held stable control. CEO Ryu Seung-ho is described as a professional manager who led the precision-chemical business from the ISU Chemical era.

2. Precision-chemical moat

Official fact: TDM is a molecular-weight regulator used in ABS, SBR, and SB-Latex manufacturing. The source describes the global TDM market as an oligopoly dominated by ISU Specialty Chemical, Arkema, and Chevron Phillips.

- Regulatory barrier: Stricter environmental and safety rules make new plant permitting difficult.

- Technology barrier: Hydrogen sulfide reaction control requires long-accumulated know-how.

- Feedstock sourcing: Because H₂S is mainly a refining byproduct, refinery-complex and pipeline infrastructure matter; the source highlights the Ulsan petrochemical complex location.

- Portfolio: NOM and NDM are used in synthetic rubber, surfactants, and lubricant additives, and NDM volume growth in 3Q25 helped defend earnings.

3. 3Q25 revenue structure

| Item | Source number | Meaning |

|---|---|---|

| 9M revenue | KRW 302.6bn | Basis for revenue structure analysis |

| Product revenue | 59.1% of total | Self-produced, relatively higher margin |

| Merchandise revenue | 38.1% of total | Trading margin, helps top-line growth |

| Mercaptan | About KRW 80.1bn | Core profit source including TDM and NDM |

| IPA/Solvent | About KRW 54.6bn | Stable cash cow including D-SOL |

| Asia | KRW 117.3bn, about 38.8% | Largest region |

| Domestic Korea | KRW 102.7bn, about 33.9% | Domestic customers such as Kumho Petrochemical and LG Chem |

| Americas/Europe | KRW 80.1bn, about 26.5% | Developed-market slowdown and high-value demand coexist |

Interpretation: A roughly 28% QoQ increase in Base Oil volume helps revenue, but a higher merchandise mix can dilute overall margins.

4. Li₂S: solid-state battery option

Solid-state batteries replace flammable liquid electrolyte with nonflammable solid material, reducing fire risk and improving energy density. The source says sulfide solid electrolytes are promising for ion conductivity and electrode contact, and Li₂S is their starting material.

- Demo plant: 20 tons/year at the Onsan plant in Ulsan, with samples supplied for customer testing.

- Mother plant: In August 2025, the board approved about KRW 85.2 billion in new facility investment, including a 500-ton/year base facility and initial 150-ton production line.

- Timeline: Construction start in September 2025 and completion target in June 2026.

- Japan entity: ISU Specialty Chemical Japan was established in August 2025 to strengthen cooperation with Toyota, Panasonic, and Japan’s solid-state battery ecosystem.

5. Financial performance and risks

Official fact: 3Q25 separate revenue was KRW 99.7 billion, operating profit was -KRW 1.4 billion, and OPM was -1.4%. Revenue rose slightly from KRW 98.9 billion in the prior quarter, and the operating loss narrowed from -KRW 4.7 billion.

| Risk | Details |

|---|---|

| ABS cycle | TDM pricing depends on ABS demand in cyclical sectors such as construction, autos, and appliances. |

| Commercialization delay | If solid-state adoption is delayed, the company may face low utilization and depreciation burden on pre-invested facilities. |

| Financial burden | Debt ratio rose to 182% at end-3Q25 from 146% at the prior year-end. Borrowings increased from KRW 124.0bn to KRW 177.0bn, and net debt ratio was 99%. |

| Financing | The source mentions KRW 35.0bn of private bonds as of end-June 2025, outstanding BW, and possible additional mezzanine financing. |

6. Conclusion

Near term, TDM pricing and investment costs may delay a full earnings turnaround. Medium to long term, the key checkpoints are the 2026 mother-plant completion, large-scale supply contracts, and signs of ABS recovery. In my view, this stock should be tracked more by Li₂S commercialization milestones than by a single quarter’s P&L.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117767710

- BusinessPost 이수스페셜티케미컬 고부가 소재: https://www.businesspost.co.kr/BP?command=article_view&num=391071

- 이수스페셜티케미컬 IR 자료: https://www.isuspecialtychemical.com/files/ir_con_2025_1.pdf

- TDM·NDM 구매의향서 체결 - 마켓인: https://marketin.edaily.co.kr/News/ReadE?newsId=03548966642364408

- 1억불 수출탑 수상 - 마켓인: https://marketin.edaily.co.kr/News/ReadE?newsId=03857286642395240

- 롯데에너지머티리얼즈 고체전해질 원료공급 MOU: https://www.ziksir.com/news/articleView.html?idxno=51901

- 황화리튬 증설 완료 - ChemLOCUS: https://www.chemlocus.co.kr/news/view/136064?url=L25ld3MvZGFpbHkvMjQvMjEx

- KRX 반기보고서: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250814003502&docno=&viewerhost=&

- 메리츠증권 리포트 브리핑 - 뉴스핌: https://www.newspim.com/news/view/20250226000241