DEEP RESEARCH · CIS / SOLID-STATE BATTERIES

CIS: Solid-State Battery Equipment Inflection and Balance-Sheet Repair

A review of the national project role, material-equipment integration, SFA support, and capital-impairment risk

0. Bottom line first

The key question for CIS is whether it can move from being an electrode-equipment maker to a process platform that co-designs solid-state battery materials and equipment. The 2025 national-project lead role and global NDAs are real strategic opportunities, but the 111.0% capital-impairment ratio, capital reduction, equity issuance, and CB overhang must be weighed just as seriously.

Official fact: The source says CIS was founded in 2002, led localization of electrode-process equipment such as coaters, calendars, and slitters, and was selected in 2025 as the lead research organization for the Ministry of Trade, Industry and Energy project to develop manufacturing process technology and equipment for 50 kg/batch sulfide-based solid electrolyte. The cited selection report includes this KIPOST article.

Interpretation: The government choosing an equipment company rather than a pure materials company suggests that solid-state batteries require material recipes and manufacturing equipment to be optimized together. Until the technology converts into revenue, backlog monetization, liquidity, and CB repayment pressure remain central.

1. Why CIS leads the national project

Solid-state batteries, especially sulfide solid electrolytes, require a fundamentally different manufacturing mechanism from liquid-electrolyte batteries. Because sulfide materials can generate hydrogen sulfide when exposed to moisture, ultra-dry environments and specialized reactor design are necessary. The source argues that simple modification of existing liquid-electrolyte equipment is not enough; material properties and equipment architecture must be synchronized.

Material-equipment integration

The merger of former subsidiary CIS Solid brings materials researchers and equipment engineers into one feedback loop.

50 kg/batch and continuous process

The national project target means pilot-level production beyond laboratory batches. The source says CIS has accumulated operating data on a continuous solid-electrolyte pilot line.

System integrator

CIS is positioned as the hub that turns the work of Isu Specialty Chemical, POSCO JK Solid Solution, Korea University, Kookmin University, and KICET into an equipment system.

Interpretation: Because Japanese players hold strong positions in solid-state patents and equipment know-how, the Korean government likely valued CIS's earlier record of localizing equipment once dominated by Japan.

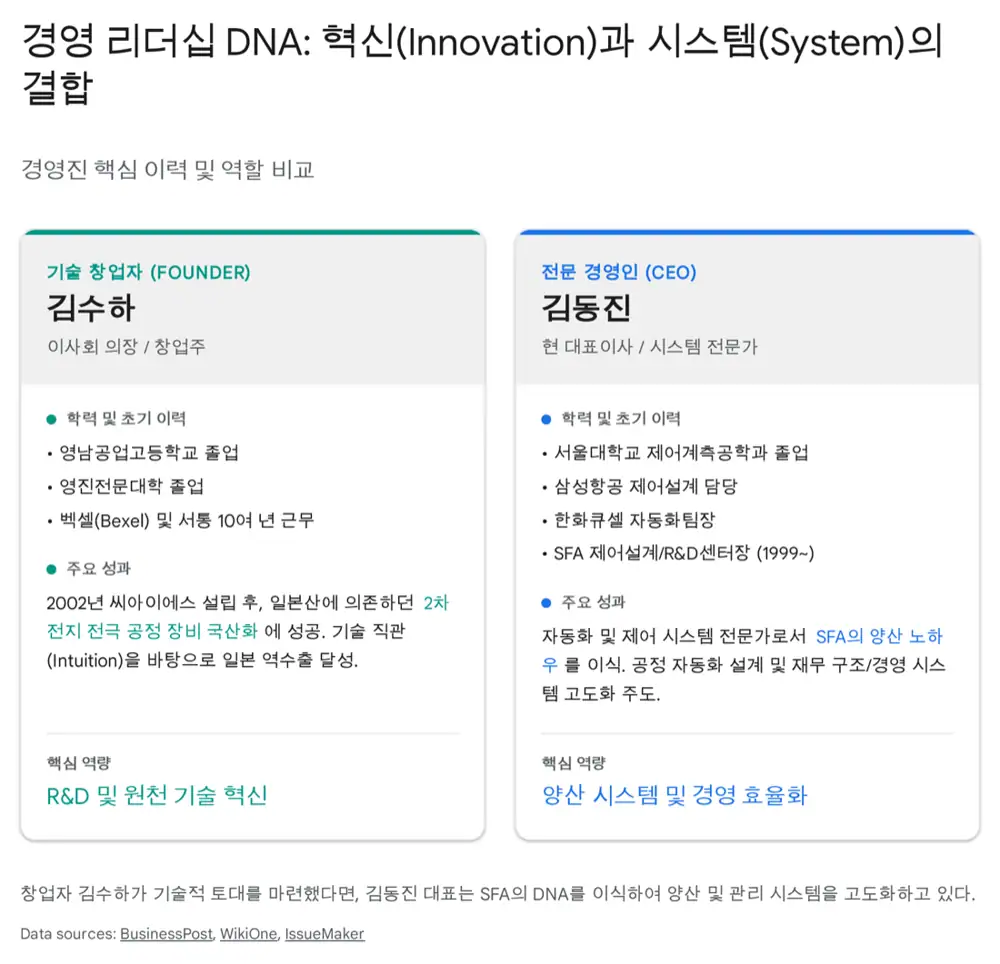

2. Leadership and SFA governance

The source frames CIS leadership as a combination of founder Kim Soo-ha's localization DNA and CEO Kim Dong-jin's system-engineering expertise. Kim Soo-ha has worked in energy since 1987, gained battery-process experience at Bexel, founded CIS in 2002, and focused on localizing coaters, roll presses, and slitters.

CEO Kim Dong-jin studied control and instrumentation engineering at Seoul National University and built a career across Samsung Aerospace, Hanwha Q CELLS, and SFA. The source describes him as an automation and precision-control manager who brought large-project management, R&D operations, high-speed/wide-width electrode-equipment design, and 2025 restructuring execution to CIS.

Official fact: The source says SFA controls CIS through DY Holdings and that, during the 2025 capital-impairment crisis, an SFA subsidiary provided KRW 40 billion of borrowings. SFA acquisition and shareholder-change references include this Seoul Economic Daily article and KRX filings.

3. Equipment portfolio: cash cow and game changer

| Area | Equipment/technology | Meaning in the source |

|---|---|---|

| Current revenue | Coater | Applies cathode and anode active materials evenly onto current collectors. The hybrid drying coater is described as doubling production speed versus existing equipment while reducing energy use. |

| Current revenue | Calendar | Compresses coated electrodes under high pressure to improve density and thickness uniformity. Precision control links directly to energy density. |

| Current revenue | Slitter | Cuts pressed electrodes to battery specifications. Minimizing burrs at the cut surface is tied to battery safety. |

| Future growth | Sulfide solid-electrolyte equipment | Continuous reactors and process equipment are core. The source says the pilot line is known to be capable of annual production on a several-ton scale. |

| Future growth | Dry coater | Dry electrode technology avoids toxic solvents such as NMP and can remove drying steps, making it important for cost reduction and solid-state process compatibility. |

CIS's technology path runs from wet-electrode process-control know-how to hybrid drying, dry coating, and then integrated solid-state material/equipment process design. The decisive proof will be commercial production orders.

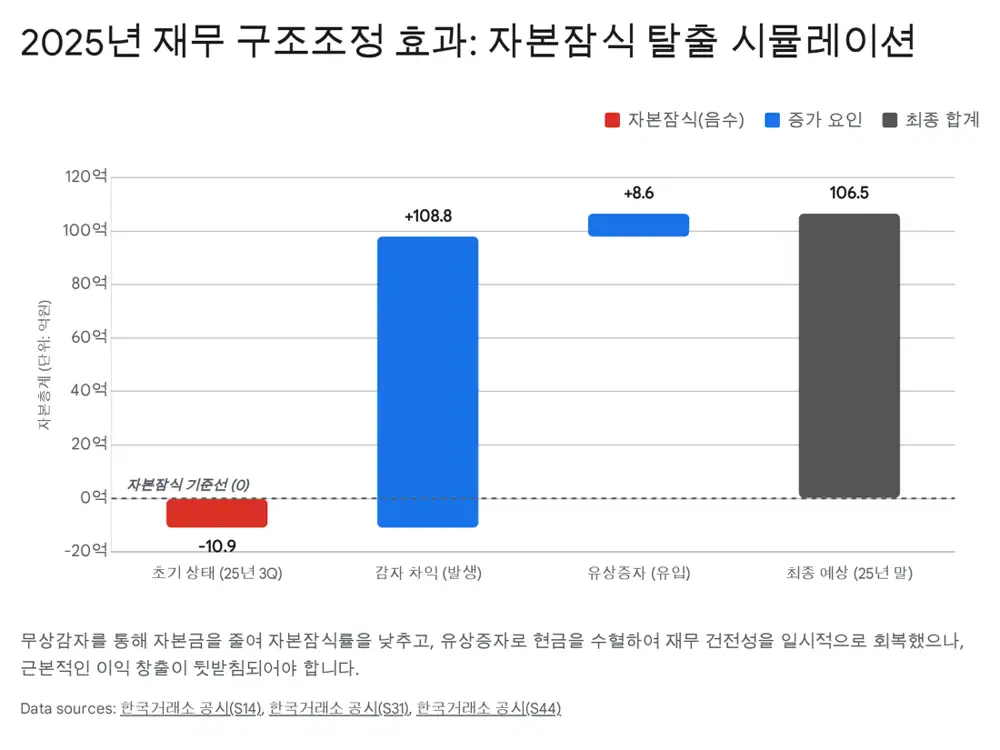

4. Financial risk: the numbers matter first

The source describes 2025 as CIS's hardest financial year since founding and the first year of balance-sheet restructuring. The technical story must be read together with delayed revenue recognition and capital-structure risk.

| Item | Figure/event | Read-through |

|---|---|---|

| Capital impairment | Capital-impairment ratio once reached 111.0% at end-3Q25 | A full impairment state that raises management designation and delisting concerns |

| Backlog | About KRW 816.9 billion, described as a record high | Orders exist, but customer EV line delays slowed delivery and revenue recognition |

| 3Q25 results | Revenue KRW 87.65 billion, down 41.2% YoY / operating profit KRW 7.55 billion | The profit turnaround is positive, but the source reads it closer to cost-cutting profit than enough to erase accumulated deficits |

| Capital reduction | August 7, 2025: par value KRW 500 → KRW 100, 5:1 reduction / capital about KRW 136.0 billion → KRW 27.2 billion | Reduction gains were used to cover deficits and resolve book-value capital impairment |

| Equity raise | About KRW 7.3 billion through public offering and KRW 1.0 billion through third-party placement including CEO Kim Dong-jin | Designed to secure operating funds and improve liquidity |

| CB overhang | KRW 30.0 billion outstanding on the first convertible bond, put option available from October 2025 | Repayment demands could pressure cash liquidity |

Interpretation: CIS is both a technology stock and a restructuring stock. Investors should check backlog-to-sales conversion, CB repayment, and post-raise cash flow before reacting to national-project headlines.

5. Global market strategy

The source says CIS's backlog is diversifying quickly from Asia toward North America and Europe. In North America, IRA-driven supply-chain de-risking from China is favorable to Korean equipment makers, and CIS has built references by supplying equipment to major battery manufacturing sites, including Ultium Cells, the LG Energy Solution and GM joint venture.

In Europe, battery startups such as Northvolt and ACC have faced challenges stabilizing mass-production yields, which raises demand for proven Korean equipment. The source says CIS has strengthened cooperation with European network partners and obtained local quality certifications such as CE certification.

Direct OEM contact

The source highlights NDAs with a leading European automaker and a North American energy company for solid-state battery materials and equipment.

Cell-maker-centered chain may change

The traditional equipment maker → battery cell maker → OEM chain may shift as OEMs work directly with material and equipment firms.

Standard capture

If CIS captures solid-state equipment standards, the company could become a strategic partner rather than a simple subcontracted equipment supplier.

6. Overall view

CIS has a strong technology narrative: national-project leadership, material-equipment integration, and global OEM cooperation. The uncomfortable financial facts are just as clear: capital impairment, capital reduction, equity issuance, and CB overhang.

My conclusion is simple. CIS should not be analyzed only as a solid-state battery theme. I need to see whether solid-state and dry-process equipment turns into production orders, whether the KRW 816.9 billion backlog turns into revenue and cash, and whether financial stability recovers under SFA support. If those three connect, CIS can be re-rated from an electrode-equipment maker into a battery-process platform.

Sources

- Original blog: 원문 블로그 · https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117726026

- Source 1: [특징주] 씨아이에스, 이차전지 국책과제 총괄연구기관 선정에 강세 · https://kr.investing.com/news/stock-market-news/article-968514

- Source 2: 씨아이에스, '2차전지 고체전해질 대량 양산기술 국책과제' 총괄연구기관 선정 · https://www.kipost.net/news/articleView.html?idxno=314447

- Source 3: 씨아이에스, 자회사 씨아이솔리드 흡수 합병…전고체 사업 경쟁력 강화 - 영남일보 · https://www.yeongnam.com/web/view.php?key=20240123001416026

- Source 4: 씨아이에스, 연속식 전고체 전해질 파일럿 라인 구축 - 디일렉 · https://www.thelec.kr/news/articleView.html?idxno=37853

- Source 5: 전극 공정 장비 국산화, 글로벌 확산 성과 인정 - 이코노미조선 · https://economychosun.com/site/data/html_dir/2025/09/18/2025091800013.html

- Source 6: 김수하 - 씨아이에스 - 위키원 · https://wiki1.kr/index.php/%EA%B9%80%EC%88%98%ED%95%98

- Source 7: [IPO] 김수하 씨아이에스 "세계 2차 전지 제조 설비 전문기업으로 도약" - EBN · https://www.ebn.co.kr/news/articleView.html?idxno=862707

- Source 8: 씨아이에스, 유럽 자동차 제조사와 전고체 배터리 사업 관련 NDA 체결 · https://www.kipost.net/news/articleView.html?idxno=322900

- Source 9: 씨아이에스, 유럽 자동차 제조사와 '전고체 배터리' NDA 체결 - 파이낸스스코프 · https://www.finance-scope.com/article/view/scp202410230005

- Source 10: 씨아이에스(주) 김수하 대표 - 이슈메이커 · https://www.issuemaker.kr/news/articleView.html?idxno=397

- Source 11: 2. 모집 또는 매출에 관한 일반사항 - KIND · https://kind.krx.co.kr/external/2025/12/01/000493/20251201001017/10601.htm

- Source 12: 증권신고서 - KRX 공시 · https://kind.krx.co.kr/external/2025/12/11/000801/20251211002302/10001.htm

- Source 13: [씨아이에스] 최대주주변경 - KRX 공시 · https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20230331003035&rcpno=20230331003035&orgid=K&tran=Y&langTpCd=0

- Source 14: 매각설 접고 씨아이에스 인수한 에스에프에이 - 서울경제 · https://www.sedaily.com/NewsView/26F1FAQS1H

- Source 15: 씨아이에스, 역대 최대 수주잔고 8200억원 확보 - 스마트투데이 · https://www.smarttoday.co.kr/ko-kr/articles/37557

- Source 16: 씨아이에스 2025년 9월 확정실적 발표 공시 - 토스증권 · https://www.tossinvest.com/stocks/A222080/news?menu=disclosure&symbol-or-stock-code=A222080&contentType=disclosure&contentParams=%7B%22id%22%3A%22DART%3AA%3A222080-20251112000489%22%2C%22companyCode%22%3A%22222080%22%2C%22reportItem%22%3A%224.2.0%22%7D

- Source 17: 씨아이에스, 수주잔고 8169억 확보…역대 최대 규모 - 뉴시스 · https://mobile.newsis.com/view/NISX20231107_0002512300

- Source 18: [씨아이에스] 분기보고서(일반법인) - KRX 공시 · https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250515001049&docno=&viewerhost=&

- Source 19: 씨아이에스, 북미 기업과 고체전해질 소재 NDA 체결 - BatteryDive · https://batterydive.com/743415

- Source 20: 씨아이에스, EU 자동차 제조사와 '전고체 배터리' NDA 체결 - 벤처스퀘어 · https://www.venturesquare.net/944049

- Source 21: 씨아이에스, 글로벌 전고체 배터리 소재·장비 시장 공략 본격화 - 한국M&A경제신문 · http://www.kmnanews.com/news/articleView.html?idxno=7923