DEEP RESEARCH · FUSION ALLOCATION

Genesis Mission and Fusion Allocation: Public-Market Exposure Research

Mapping listed-company routes into private fusion leaders and their strategic leverage.

0. Bottom line first

The practical problem in fusion investing is that most leaders are private. Under the Genesis Mission policy catalyst, I look at listed-company access routes through DJT, Eni, Nucor, and Liberty Energy, which have direct or indirect exposure to private fusion companies.

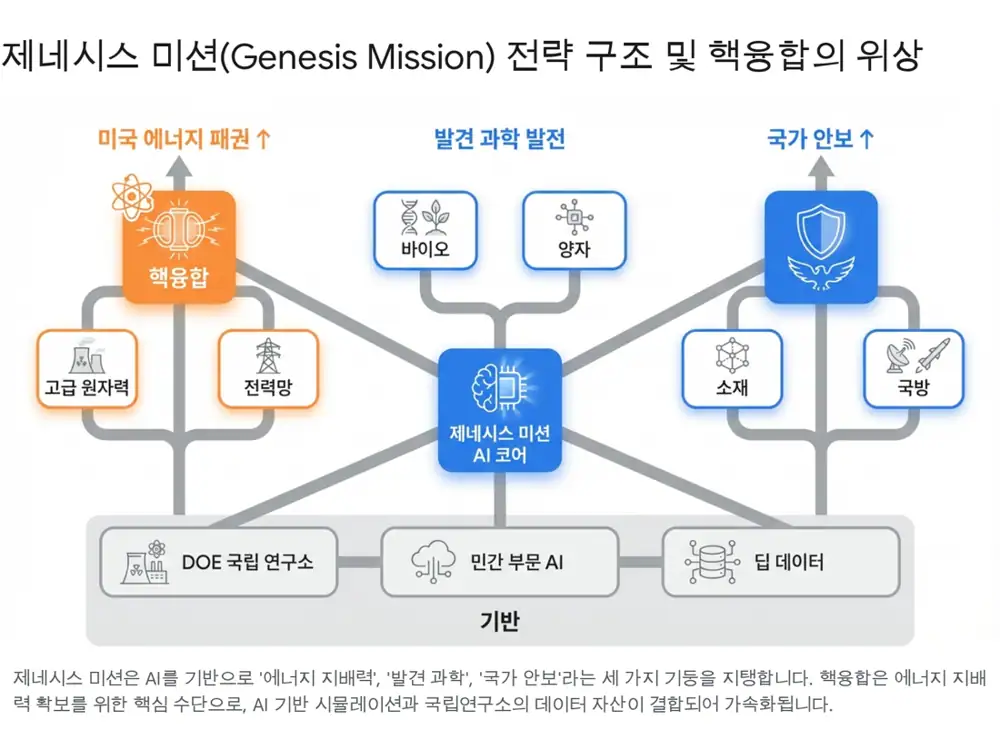

Official fact: The source says the Genesis Mission was formalized by White House Executive Order 14363 on November 24, 2025, with DOE combining scientific data from 17 national laboratories with private-sector AI compute.

Interpretation: As AI and energy security converge, fusion and advanced nuclear move up as strategic industries for data-center and advanced-manufacturing power demand.

1. Genesis Mission: AI plus energy security

The source interprets the Genesis Mission as an ambitious U.S. science and technology project. AI is framed as an operating system for national scientific infrastructure, accelerating discovery and building a technology lead over China.

2. The private fusion big four

Commonwealth Fusion Systems

MIT PSFC spinout using HTS magnets in a tokamak approach. It is building SPARC and targets ARC in the early 2030s. Total funding is about USD 3 billion.

TAE Technologies

Pursues field-reversed configuration and hydrogen-boron fuel. It has worked with Google on AI for more than a decade and raised more than USD 1.3 billion.

Helion Energy

Uses pulsed magneto-inertial fusion and direct energy conversion, with helium-3 as fuel. It has raised more than USD 1 billion and presented a 2028 Microsoft PPA.

General Fusion

Uses magnetized target fusion with liquid metal liner compression. Funding is below about USD 500 million, and recent financing stress is noted as a risk.

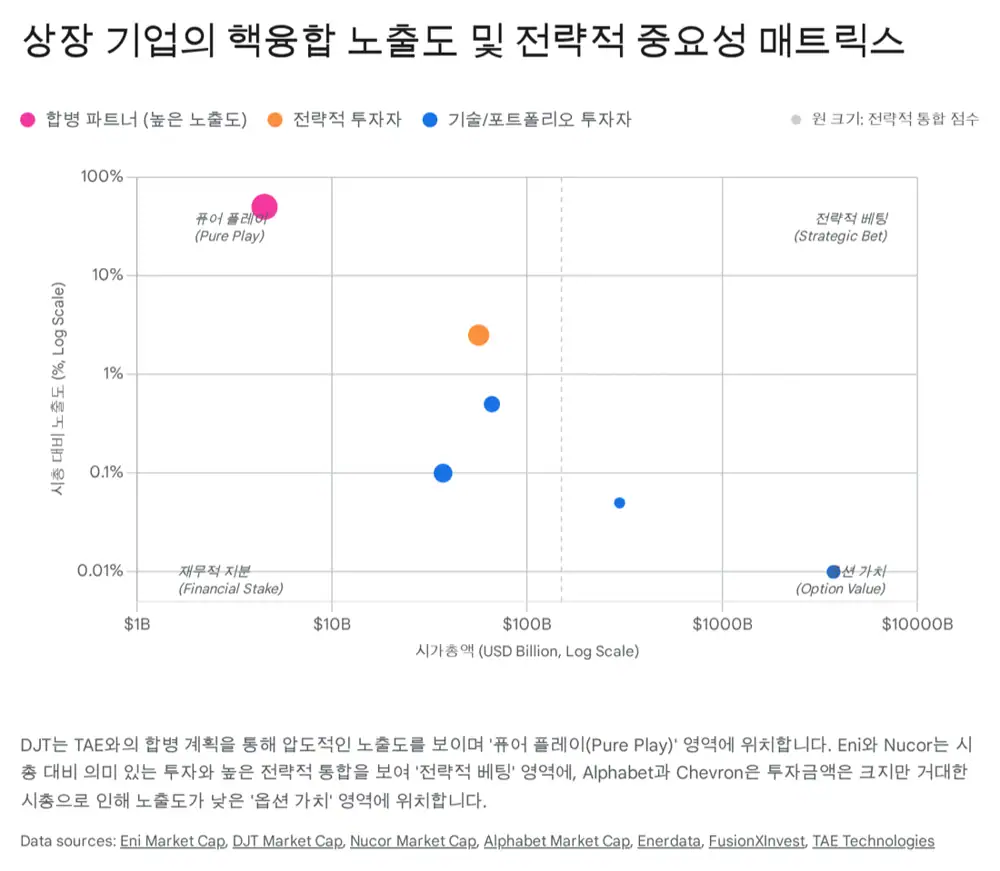

3. Listed-company exposure

| Rank | Listed company | Market cap | Target | Exposure | Attraction and caveat |

|---|---|---|---|---|---|

| 1 | Trump Media (DJT) | About $4.5B | TAE Technologies | Extreme / effectively 100% | After the stock-swap merger with TAE, it effectively becomes a listed fusion pure play. It combines policy upside with meme-stock volatility. |

| 2 | Eni S.p.A. (E) | About $56B | CFS | High / about 3% | Described as a strategic and relative-majority shareholder of CFS. It could rerate among energy majors if CFS succeeds, while offering dividend stability. |

| 3 | Nucor (NUE) | About $36B | Helion | Medium | The 500 MW steel-mill-linked plant model matters more than the investment amount. The industrial logic is energy-cost reduction. |

| 4 | Liberty Energy (LBRT) | About $2.8B | Oklo/Fervo indirect | Policy Beta | More a regulatory-easing and new-energy-infrastructure policy beta than direct fusion equity exposure. |

4. Company-level interpretation

DJT / TAE

On December 18, 2025, DJT announced a stock-swap merger agreement with TAE Technologies. The combined company is valued at more than about USD 6 billion, or roughly KRW 8.5 trillion, and DJT agreed to provide up to USD 200 million in cash plus another USD 100 million upon further SEC filings, according to the source.

Eni / CFS

Eni invested USD 50 million in CFS’s 2018 Series A and joined the USD 1.8 billion Series B in 2021 and USD 863 million Series B2 in 2025. The source infers a possible 10-15% stake from Eni’s “strategic shareholder” and “relative majority shareholder” wording.

Nucor / Helion

Nucor and Helion announced plans to develop a 500 MWe fusion power plant at a U.S. steel mill. The source sees the industrial significance in direct power supply to factories rather than in the size of the investment alone.

5. Portfolio conclusion

For aggressive pure fusion exposure, DJT is presented as the most direct path. Eni is framed as a route to share in CFS’s success while retaining an energy-major downside cushion and dividend profile. Nucor is a real-economy option on lower manufacturing energy costs, while Liberty Energy is mainly policy beta.

Sources

- 원문: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117477165

- 미국 제네시스 미션 정보 요청: https://drive.google.com/open?id=1TZL2EDUR-5IErBLB0gIWAFyKFA6zgEIt-NEKc9iUAJU

- Launching the Genesis Mission - The White House: https://www.whitehouse.gov/presidential-actions/2025/11/launching-the-genesis-mission/

- 핵융합 기업 투자 정보 조사: https://drive.google.com/open?id=1A3Axw7aup2o2LfvOwYvY_ZVdJ64Xmg2UtPTSpdG___c

- CFS raises $1.8 billion Series B: https://www.cfs.energy/news-and-media/commonwealth-fusion-systems-closes-1-8-billion-series-b-round/

- CFS raises $863 million video: https://www.youtube.com/watch?v=6bNWtkzyShs

- CFS raises $863 million Series B2: https://cfs.energy/news-and-media/commonwealth-fusion-systems-raises-863-million-series-b2-round-to-accelerate-the-commercialization-of-fusion-energy/

- Trump Media fusion play for TAE: https://www.latitudemedia.com/news/trump-medias-bizarre-fusion-play-for-tae-technologies/

- TAE raises $150 million: https://www.prnewswire.com/news-releases/tae-technologies-raises-150-million-in-latest-funding-round-302470656.html

- General Fusion $130 million financing: https://generalfusion.com/post/general-fusion-closes-oversubscribed-130-million-transitional-financing-round/

- Reuters/Investing.com Trump Media TAE $6 billion deal: https://www.investing.com/news/stock-market-news/trump-media-tae-technologies-to-combine-in-6-billion-deal-4414623

- Indian Express Trump Media merges with TAE: https://indianexpress.com/article/world/truth-social-trump-media-merges-with-fusion-company-tae-technologies-10427555/

- GlobeNewswire DJT to merge with TAE: https://www.globenewswire.com/news-release/2025/12/18/3207544/0/en/Trump-Media-Technology-Group-to-Merge-with-TAE-Technologies-a-Premier-Fusion-Power-Company-in-All-Stock-Transaction-Valued-at-More-Than-6-Billion.html

- TAE announcement on Trump Media merger: https://tae.com/trump-media-and-technology-group-to-merge-with-tae-technologies/

- Equinor invests in fusion energy: https://www.equinor.com/news/ev/invests-fusion-energy

- Motley Fool fusion energy stocks: https://www.fool.com/investing/stock-market/market-sectors/energy/nuclear/fusion-energy/

- Enerdata Eni US$1bn CFS power deal: https://www.enerdata.net/publications/daily-energy-news/eni-signs-us1bn-deal-power-cfss-first-fusion-plant-us.html

- Eni market cap - MLQ.ai: https://mlq.ai/stocks/E/market-cap/

- Helion $35m strategic investment from Nucor: https://fusionxinvest.com/news/3488/helion-energy-secures-35m-strategic-investment-from-nucor/

- Nucor and Helion 500 MW plant: https://nucor.com/news-release/nucor-and-helion-to-develop-historic-500-mw-fusion-power-plant-122758

- Hogan Lovells Helion and Nucor 500 MWe plant: https://www.hoganlovells.com/en/publications/helion-and-nucor-announce-plans-to-develop-a-500-mwe-fusion-power-plant-at-a-us-steel-mill

- Google and CFS strategic partnership: https://cfs.energy/news-and-media/google-and-commonwealth-fusion-systems-sign-strategic-partnership/

- Oklo and Liberty Energy integrated power solution: https://investors.libertyenergy.com/news-and-events/press-releases/2025/07-23-2025-114517877

- DOE nominee Wright power supply remarks: https://www.utilitydive.com/news/doe-chris-wright-liberty-energy-senate/737545/

- Chevron invests in Google-backed fusion startup: https://www.nasdaq.com/articles/chevron-cvx-invests-in-google-backed-nuclear-fusion-startup

- Nvidia joins Google to fund CFS: https://thebusinessdownload.com/nvidia-joins-google-to-fund-commonwealths-fusion-power-plant/