DEEP RESEARCH · SAMSUNG SDI

Genesis Mission and Samsung SDI’s Solid-State Battery Strategy

How Ulsan, liquidity, and sulfide all-solid-state batteries shape the post-2027 technology-sovereignty thesis.

0. Bottom line first

Samsung SDI is under earnings pressure in 2025, but the source frames its polarizer sale proceeds, rights offering, Ulsan cluster, and sulfide ASB roadmap as a bridge toward technology leadership after 2027.

1. Downcycle and capital redeployment

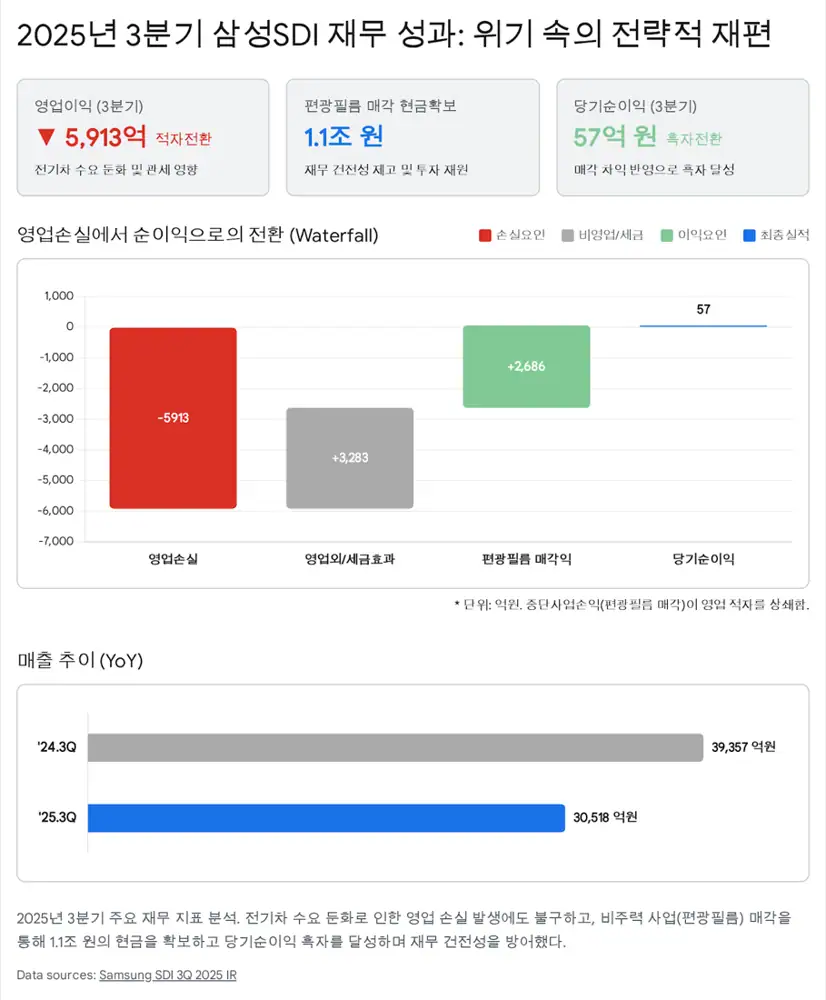

Official fact: Cumulative Q3 2025 revenue was KRW 9.408T, down 26.7% YoY, and operating profit turned to a KRW 1.4232T loss. Energy Solution revenue was KRW 8.7621T, down about KRW 3.3646T YoY.

The company sold its polarizer-film business to Wuxi Hengxin Optical Material, securing about KRW 1.1825T in cash and turning Q3 net income positive. The source interprets this as capital redeployment for all-solid-state batteries and North America JVs.

The original inline link is preserved here: http://googleusercontent.com/assisted_ui_content/2.

2. Genesis Mission and Ulsan

Official fact: Ulsan was designated as a battery special zone in July 2023 and targets KRW 8.1T of private investment by 2030. The government and Ulsan city are investing KRW 34B by 2025 in a next-generation battery park and supporting a KRW 138.5B technology-development program.

Interpretation: Ulsan is framed as a full-cycle mother-factory cluster linking materials, cells, automakers, and recycling. Samsung SDI validates ASB and LFP processes there and can transfer them to Hungary and StarPlus Energy in the U.S.

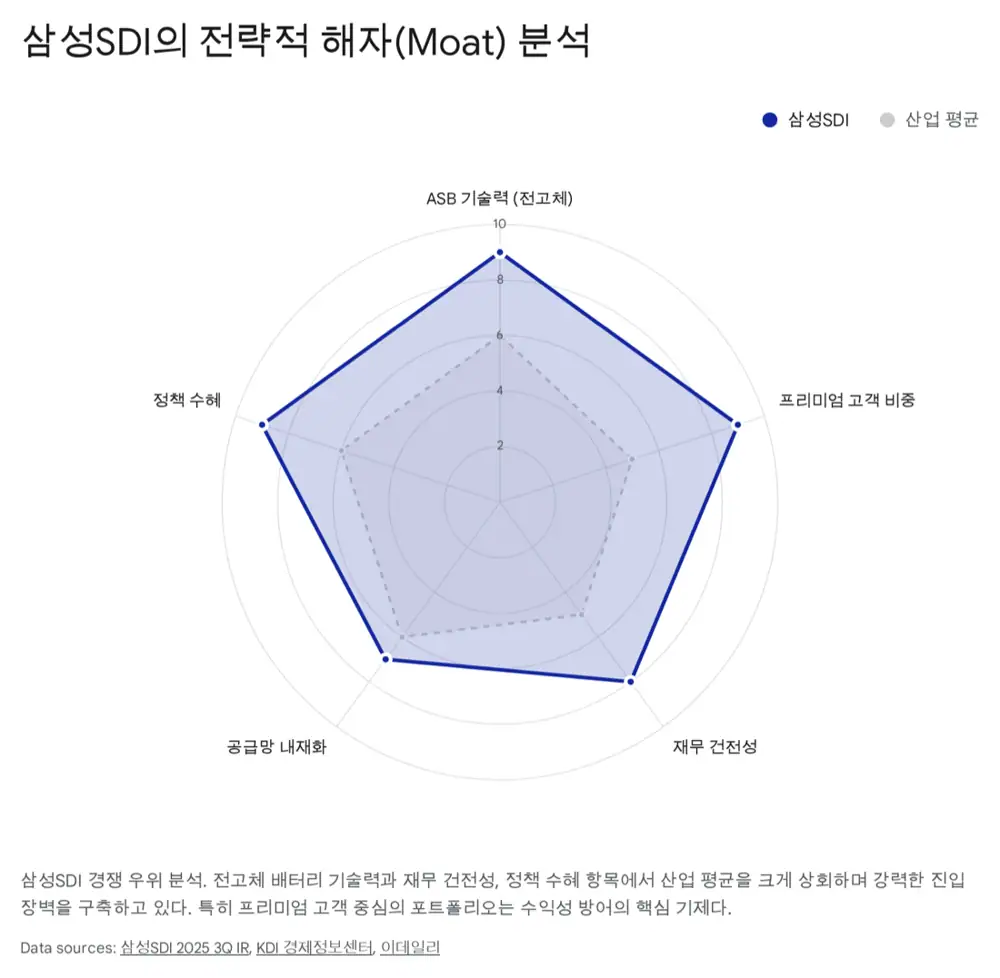

3. Solid-state battery moat

Sulfide

The source says sulfide electrolytes can reach around 10^-2 S/cm ionic conductivity.

Anode-less

Samsung targets 900Wh/L energy density, more than 40% higher than lithium-ion.

Hybrid

A mix of wet and dry process advantages targets efficiency and cost reduction.

InChems

A 120-ton pilot line and hydrogen sulfide suppression technology make it a possible value-chain partner.

4. Investment capacity and capital allocation

| Item | Source number | Meaning |

|---|---|---|

| Q3 2025 revenue | KRW 3.0518T | Near-term EV chasm impact |

| Q3 2025 operating loss | KRW 591.3B | Profitability pressure |

| Net income | KRW 5.7B | Reflects KRW 268.6B income from discontinued operations |

| Cash and equivalents | KRW 2.1486T | Up KRW 526.8B YoY |

| Cumulative CAPEX | KRW 2.3421T | Continued investment with efficiency focus |

| Rights offering | KRW 1.6549T | Funding for GM JV, ASB R&D, and overseas capacity |

5. Three moats and outlook

- Technology moat: the source says sulfide ASB, hybrid process, and anode-less design are viewed as two to three years ahead.

- Customer moat: BMW, Audi, Rivian, GM, and Stellantis support a premium-customer base.

- Policy moat: Ulsan, tax credits, AMPC, and infrastructure support create institutional protection.

For 2025-2026, ESS LFP, StarPlus utilization, SBB 1.7, and SBB 2.0 are defensive levers. For the medium term, 2027 ASB production and 46-series cylindrical batteries are the key milestones.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117429690

- Reference 1: http://googleusercontent.com/assisted_ui_content/2

- Reference 2: https://drive.google.com/open?id=1pAUeKu712-BYNbUtdgoVPAjjpqEr7zkupgLe4uiKjAE

- Reference 3: https://eiec.kdi.re.kr/policy/callDownload.do?num=241690&filenum=1&dtime=20230918000228

- Reference 4: https://www.investkorea.org/us-kr/cntnts/i-1112/web.do

- Reference 5: https://www.iusm.co.kr/news/articleView.html?idxno=1056031

- Reference 6: https://ir.edaily.co.kr/News/Read?k=03171766642338496

- Reference 7: https://www.thelec.kr/news/articleView.html?idxno=43044

- Reference 8: http://www.s-d.kr/news/articleView.html?idxno=76495

- Reference 9: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250324001033&docno=&viewerhost=&

- Reference 10: https://www.investchosun.com/site/data/html_dir/2025/03/14/2025031480025.html