DEEP RESEARCH · SOLID-STATE BATTERIES

KOSDAQ Reform and the Solid-State Battery-Aerospace Portfolio

Reading Korea's KRW 150tn growth fund through Non-China supply chains, sulfide solid-state batteries, and aerospace materials

0. Bottom line first

My conclusion is that the 2025 KOSDAQ activation policy should be read not as simple liquidity injection, but as a structural effort to finance Non-China supply chains in solid-state batteries and aerospace materials.

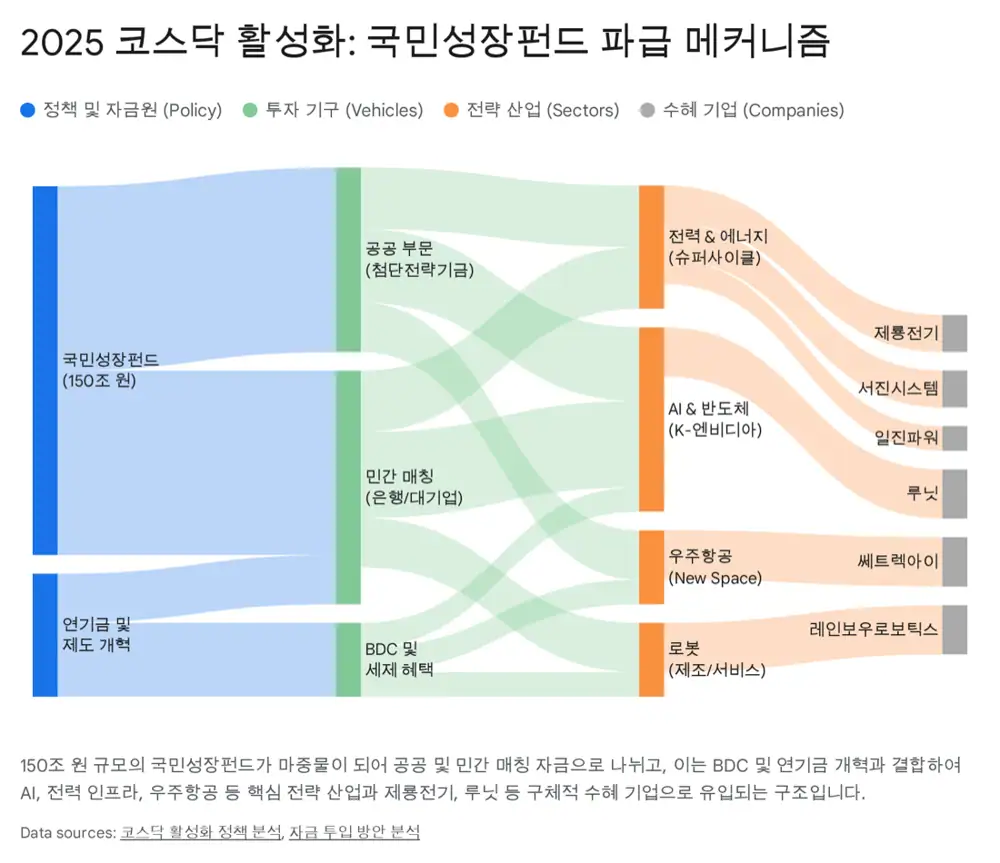

Official fact: The source highlights a KRW 150tn National Growth Fund, focus on AI, secondary batteries, and aerospace, more precise technology-special listing rules, and delisting of zombie companies.

Interpretation: The next KOSDAQ leaders are likely to be companies that prove technology sovereignty, scale-up capacity, and regional-cluster fit at the same time.

KRW 150tn fund

Redefines KOSDAQ as an incubator for national growth engines by financing scale-up.

Sulfide solid-state

Ionic conductivity around 10^-2 S/cm and EV applicability make it a policy priority.

Advanced materials

Special alloys and titanium materials connect with SpaceX value-chain expectations.

1. Policy frame: KOSDAQ as an industrial incubator

The source reads the December 2025 measures to improve KOSDAQ trust and innovation as a reform of Korea's capital-raising system, beyond a simple Korea-discount fix. The core is not a policy of listing as many companies as possible, but a grow-and-kill discipline that supports verified firms while forcing out weak ones.

The macro backdrop is the U.S. Genesis Mission. The source interprets it as a supply-chain restructuring strategy aimed at reviving U.S. manufacturing and reducing China dependence to zero. FEOC exclusion under the IRA and CHIPS Act raises the strategic value of Korean materials, parts, and equipment companies that can build Non-China battery and aerospace supply chains.

2. Solid-state batteries: sulfides and wet process rise

The EV chasm is tied to fire safety and driving range. Liquid-electrolyte lithium-ion batteries carry thermal-runaway risk and density limits, while solid-state batteries target both safety and higher energy density through nonflammable solid electrolytes and bipolar structures. They are also attractive in aerospace, where batteries must handle vacuum and extreme temperatures.

| Electrolyte | Source advantage | Source weakness | Suitable area |

|---|---|---|---|

| Sulfide | Ionic conductivity around 10^-2 S/cm, easier particle contact | Moisture sensitivity and H2S risk | Large EV batteries; used by Samsung SDI, SK On, Toyota |

| Oxide | High stability | Low ionic conductivity and high-temperature sintering | Small electronics, IoT sensors, some ESS and defense use |

| Polymer | Easy and low-cost manufacturing | Conductivity too low for easy room-temperature operation | Government research and specific polymer materials |

Cost is the last commercialization hurdle. Dry synthesis offers performance but is energy-intensive and hard to scale. Wet synthesis helps uniform particle control and mass production, but residual solvent can hurt conductivity. The source argues that third-generation wet synthesis from companies such as Solivis is changing the game.

3. Government-selection portfolio: private and listed pillars

Solivis

Key points are 11-12 mS/cm wet-synthesis performance, a 40-ton Hoengseong plant, and KRW 42.2bn of cumulative funding.

InChems

Located in the Ulsan battery cluster, with H2S suppression technology and a 120-ton-per-year pilot line.

TDL

Enchem acquired 54.56%; procurement registration and direct-production certification open the government market.

Energy11

A NineTech affiliate developing hybrid solid-electrolyte films and sodium secondary batteries.

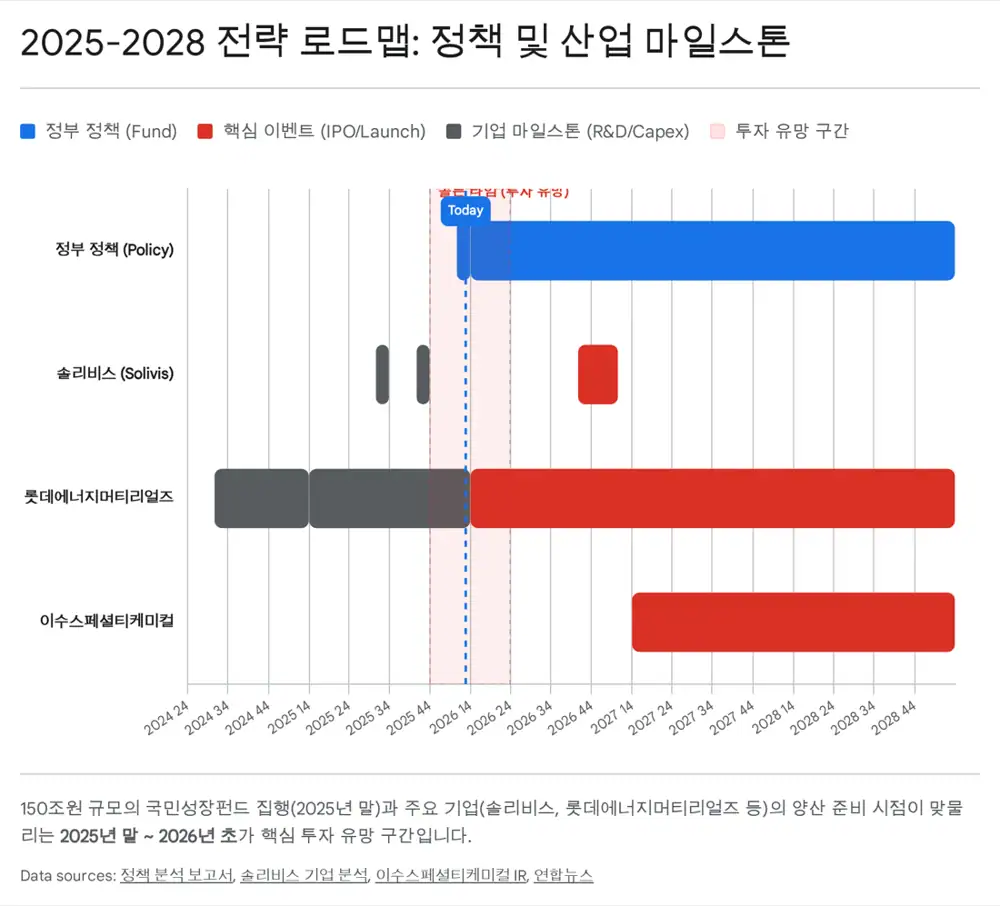

In private companies, Solivis is presented as the most aggressive candidate. Founded by Hanyang University professor Shin Dong-wook, it has more than 20 years of research know-how, 11-12 mS/cm performance versus Japanese competitors' 8 mS/cm, a 40-ton-per-year plant in Hoengseong, 2025 operation, KRW 42.2bn of cumulative investment, preliminary-unicorn selection, and up to KRW 20bn of guarantee support. The source also mentions a possible technology-special IPO in the second half of 2026.

| Listed pillar | Source investment point | Policy logic |

|---|---|---|

| Korea Zinc | KRW 10-11tn U.S. smelter, strategic minerals such as antimony, germanium, gallium, and KEMCO nickel sulfate | U.S. supply-chain alliance and resource security |

| ISU Specialty Chemical | Only Korean mass-production candidate for lithium sulfide (Li2S), Onsan demo plant, 2027 mass-production setup | Keystone for localizing solid-state materials |

| Lotte Energy Materials | Copper-foil cash flow, Iksan 70-ton pilot, plan to expand to 1,200 tons by 2026 | Regional base and major-company investment |

4. High-beta alpha and aerospace materials

Among KOSDAQ and smaller names, Lemon, Hannong Chemicals, and CIS are framed as high-beta policy-benefit candidates. Lemon applies electrospun nanofiber supports to solid-state batteries, with results showing 5.5-8x longer life and 1.5x higher capacity. Hannong Chemicals leads a government project for lithium-metal-polymer all-solid polymer electrolyte materials with LG Energy Solution and KRICT. CIS develops continuous manufacturing equipment for solid-state electrolytes and has a lineup that can address both dry and wet processes.

Nanofiber support

The source's key advantage is platform applicability across electrolyte types.

Government project

Polymer-electrolyte work creates a government-validation effect.

Mass-production equipment

Equipment suppliers may benefit first when the industry moves from lab to mass production.

The aerospace side includes SeAH Besteel Holdings and HVM. SeAH's points are talks around special alloys such as nickel-chromium-titanium for rocket and satellite engines and its special-alloy plant in Texas. HVM's points are cooperation with a first-tier supplier to SpaceX, vacuum melting technology, and aerospace-grade high-purity titanium alloy manufacturing.

5. Asset-allocation conclusion

Interpretation: I read the policy not as money printing, but as a capital-market effort to build Korea's supply-chain survival capacity amid U.S.-China rivalry. In 2025, pilot lines produce samples; from 2026, mass-production investments and the BDC system can help companies cross the valley of death.

| Portfolio | Source weight | Candidates | Logic |

|---|---|---|---|

| Core | 60% | Korea Zinc, ISU Specialty Chemical, SeAH Besteel Holdings | Companies with earnings and control of core materials or supply chains |

| Alpha | 40% | Solivis, Lemon, HVM | High-beta names with technology moats and direct policy benefits |

- The key words are Non-China, High-Tech, and Mass-Production.

- Technology alone is not enough; the proof must be CAPA from pilot to mass production.

- Policy-benefit stocks can be volatile, so listed core materials and high-beta technology names should be evaluated separately.

Sources

- 원문 / Original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117405129

- 코스닥 활성화 정책 분석 및 전망: https://drive.google.com/open?id=1KklOBNrPtbr9nN5_rdxIePxZFHPcP1yGbzErIj8frPY

- 고려아연 미국 제련소 투자 분석: https://drive.google.com/open?id=1A8wrPyt-Wl-PAazY317EOO_BSnloJlwSGrBRjkvbHY4

- 이수스페셜티케미컬 457190 report: https://file.alphasquare.co.kr/media/pdfs/company-report/20240903103719381K_02.pdf

- 한농화성 전고체 배터리 기사: https://www.thebigdata.co.kr/view.php?ud=202410220224568718cd1e7f0bdf_23

- 레몬 전고체 상용화 기사: https://www.newsprime.co.kr/news/article/?no=595000

- 솔리비스 기업 분석 요청 및 계획: https://drive.google.com/open?id=10NErv_DwxRj8bqlOg9KsH2ScuANg0Ts93hfjxoeN_20

- 이수스페셜티케미컬 IR book: https://www.isuspecialtychemical.com/files/irbook_2025.pdf

- MK Solivis article: https://www.mk.co.kr/en/business/10975341

- 조선비즈 전고체 배터리 테마 기사: https://biz.chosun.com/stock/c-biz_bot/2025/10/24/U3IJEDRAHRP36LAE2YBXLY5L5E/

- 스틸데일리 세아베스틸지주 기사: https://www.steeldaily.co.kr/news/articleView.html?idxno=196972

- THE VC InChems profile: https://thevc.kr/inchems

- Daum InChems pilot production article: https://v.daum.net/v/20240204160118395

- 디지털데일리 울산 배터리 특화단지 article: https://m.ddaily.co.kr/page/view/2023081613242928252

- 서울국제금융오피스 엔켐 전고체 배터리 기업 인수: http://seoulfnhub.kr/bbs/board.php?tbl=bbs47&mode=VIEW&num=31616&category=kr&findType=&findWord=&sort1=&sort2=&page=&mobile_flag=

- 딜사이트 엔켐 티디엘 인수: https://dealsite.co.kr/articles/107896/089038

- 디지털데일리 엔켐 티디엘 인수: https://m.ddaily.co.kr/page/view/2023080115390650014

- 뉴스핌 에너지11 article: https://www.newspim.com/news/view/20240930000081

- 이머니뉴스 에너지11 article: http://www.emoneynews.co.kr/news/articleView.html?idxno=115756

- Korea Zinc U.S. smelter release: https://www.koreazinc.co.kr/en/korea-zinc-partners-with-the-u-s-department-of-war-and-u-s-department-of-commerce-to-build-a-state-of-the-art-critical-minerals-smelter-in-the-united-states-with-6-6-billion-of-capital-expenditures/

- NIST CHIPS incentives for Korea Zinc subsidiary: https://www.nist.gov/news-events/news/2025/12/department-commerce-awards-chips-incentives-subsidiary-korea-zinc-crucible

- 이수스페셜티케미컬 852억 투자 기사: https://www.globalepic.co.kr/view.php?ud=202509082133151229ac3d53c8ec_29

- 레몬 지원책 기대 기사: https://www.thebigdata.co.kr/view.php?ud=202409030636223966cd1e7f0bdf_23

- 연합뉴스 롯데에너지머티리얼즈 pilot article: https://www.yna.co.kr/view/AKR20240205085600003

- 폴리뉴스 롯데에너지머티리얼즈 article: https://www.polinews.co.kr/news/articleView.html?idxno=662842

- 톱텍 레몬 공지사항: https://toptec.co.kr/home/customer/notice/?mod=document&uid=211

- 아시아경제 레몬 article: https://cm.asiae.co.kr/article/2023030809241905867

- 머니S 한농화성 article: https://www.moneys.co.kr/article/2025060210303072257

- The Elec 씨아이에스 pilot line article: https://www.thelec.kr/news/articleView.html?idxno=37853

- Steel Radar SeAH SpaceX article: https://www.steelradar.com/en/seah-steel-will-supply-steel-materials-to-spacex/

- Korea Herald SeAH SpaceX article: https://www.koreaherald.com/article/3071414

- Chosunbiz SeAH aerospace article: https://biz.chosun.com/en/en-finance/2025/12/14/BCQ432EYM5F47FOONRJUXQ7MNQ/

- 한국경제 HVM SpaceX value chain article: https://www.hankyung.com/article/202508015569a

- 파이낸셜경제 우주항공 관련주 article: http://www.finomy.com/news/articleView.html?idxno=245975