DEEP RESEARCH · MEMORY SEMICONDUCTORS

2025-2026 Semiconductor Deep Dive: Geopolitical Divergence and the Memory Power Shift

A review of whether the valuation gap among Micron, Samsung Electronics, and SK hynix is being driven more by geopolitics than by technology alone.

0. Bottom line first

My reading is straightforward. The AI memory supercycle helps all three companies, but the market is assigning a higher valuation to Micron because it has lower China exposure and receives U.S.-Japan policy support.

Interpretation: The core hypothesis is that U.S. policy to foster domestic and Japanese semiconductor capacity can structurally pressure Korean memory companies’ share and valuation. In this phase, security premium and geopolitical discount are both visible.

1. The 2025 second-half stock-market split

Official fact: The source compares stock trends from July 2025 to December 20, 2025 with 2026 market outlooks, industrial policy, and CAPEX strategy.

| Company | Key facts and numbers in the source | Investor read-through |

|---|---|---|

| Micron | Record high of $265.92 on December 19, 2025; FY2026 Q1 revenue of $13.64B, up 57% YoY; next-quarter revenue guidance of $18.7B | Sold-out HBM supply and strategic-asset status explain the premium. |

| Samsung Electronics | Fell to around KRW 51,700 in mid-November; HBM3E qualification delays; ongoing foundry losses | Memory recovery is offset by foundry losses and lost early AI momentum. |

| SK hynix | More than 50% HBM share; record-high Q3 operating profit; operating margin above 40% | Technology leadership is clear, but Wuxi exposure and non-fundamental volatility cap upside. |

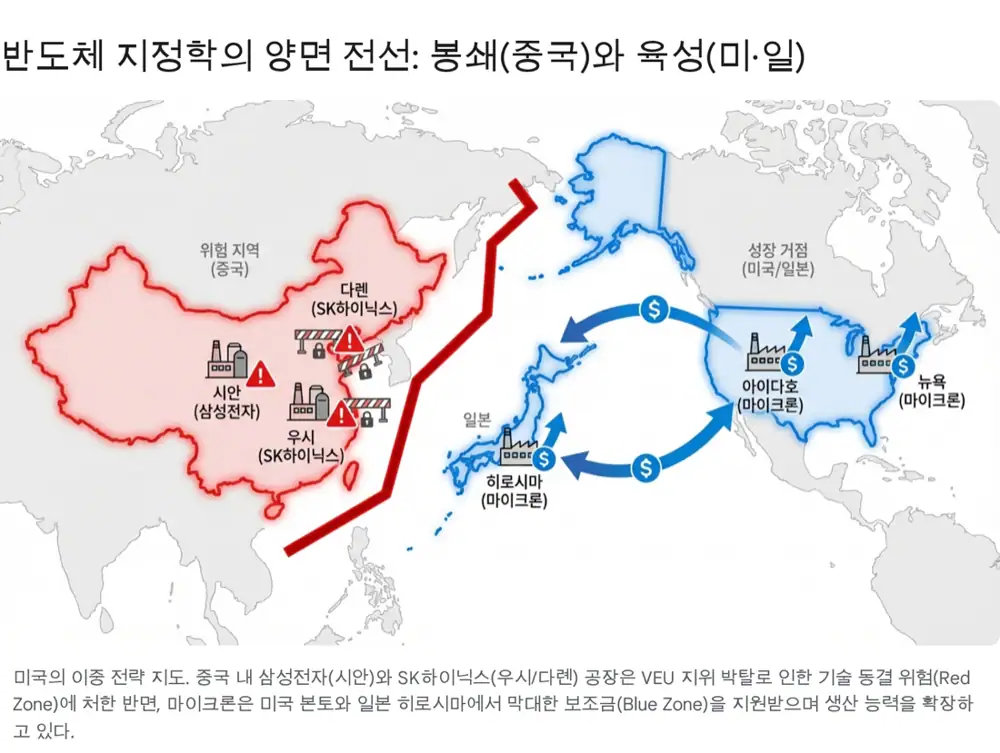

2. The U.S. two-track strategy: contain and nurture

The source frames U.S. and Japanese policy as a strategy that nurtures Micron while constraining Korean companies’ ability to upgrade China-based production.

- In September 2025, Japan decided to provide up to JPY 536B, about $3.6B or KRW 4.8T, in subsidies for Micron’s Hiroshima plant.

- The funds target 1-gamma DRAM and EUV equipment.

- The subsidy is described as covering roughly one-third of Micron’s Japan investment.

- U.S. VEU revocation and export controls may turn Korean Chinese fabs into stranded assets over time.

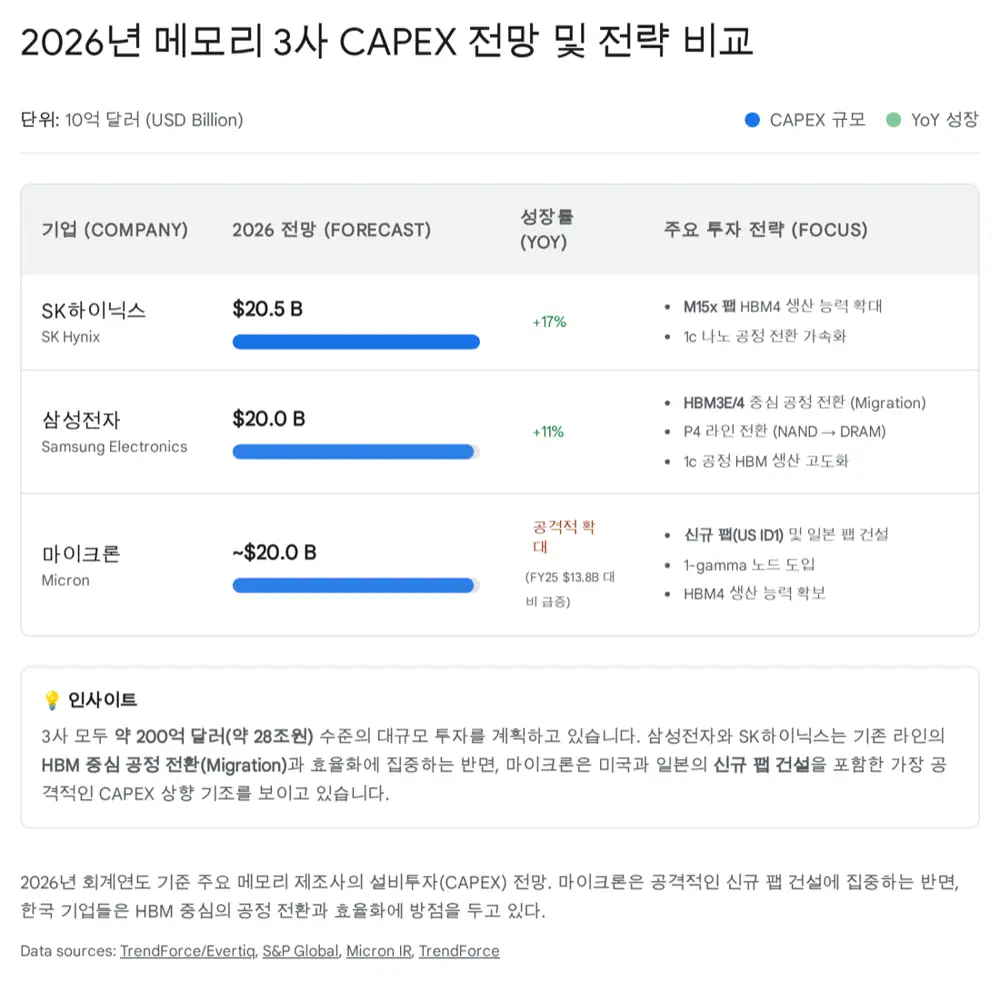

3. 2026 CAPEX and the shortage benefit

Official fact: The source says Micron lifted FY2026 CAPEX to about $20B, roughly KRW 27T, up about 11% year over year.

Micron is focused on new fabs in Idaho, New York, and Hiroshima and targets about 20% bit shipment growth in 2026. Samsung and SK hynix, constrained by China exposure, are focused more on conversion investment, advanced HBM process upgrades, and natural attrition than on raw wafer capacity expansion.

- An HBM die requires two to three times more wafer area than standard DDR5.

- As Korean suppliers allocate limited capacity to HBM, general PC and server DDR5 supply can tighten.

- Micron’s cleaner U.S.-Japan capacity can benefit disproportionately in that shortage environment.

4. HBM4 technology race

1c DRAM and turnkey

Samsung is pushing HBM4 with 1c DRAM and a memory-foundry-packaging turnkey pitch.

TSMC alliance

SK hynix plans to use TSMC 12nm and 5nm logic processes for HBM4 base dies.

1-gamma and EUV

Micron is betting on 1γ EUV in Hiroshima, claims 30% better power efficiency, and targets 20-25% HBM share.

5. Final takeaways

- The U.S. CHIPS Act and Japanese subsidies give Micron a “safe growth” shield.

- VEU revocation and China production exposure have become risks for Samsung and SK hynix.

- The supercycle can help all memory makers, but lower geopolitical risk can deserve a higher multiple.

- Korean companies need visible HBM4 superiority and faster China-risk reduction.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117401809

- Reference 1: https://www.macrotrends.net/stocks/charts/MU/micron-technology/stock-price-history

- Reference 2: https://ca.investing.com/news/stock-market-news/micron-surges-as-global-memory-chip-shortage-boosts-profit-forecast-4371878

- Reference 3: https://stockstory.org/us/stocks/nasdaq/mu/news/why-up-down/why-micron-mu-stock-is-up-today-3

- Reference 4: https://www.technetbooks.com/2025/12/micron-reports-record-profits-as-ai.html

- Reference 5: https://thefinancialexpress.com.bd/stock/global/samsung-electronics-shares-hit-four-year-lows-on-trump-risks

- Reference 6: https://www.rcrwireless.com/20250925/ai-infrastructure/samsung-nvidia-chips

- Reference 7: https://m.economictimes.com/news/international/business/samsungs-sudden-122-billion-wipeout-shows-the-cost-of-sleeping-on-ai/articleshow/114767397.cms

- Reference 8: https://wccftech.com/samsung-dram-profits-are-not-enough-to-compete-with-tsmc-in-foundry-business/

- Reference 9: https://counterpointresearch.com/en/insights/sk-hynix-tops-dram-market-for-three-consecutive-quarters

- Reference 10: https://news.skhynix.com/sk-hynix-announces-3q25-financial-results/

- Reference 11: https://futurumgroup.com/press-release/us-regulations-for-chipmakers-sk-hynix-samsung-tsmc/

- Reference 12: https://www.eetimes.com/u-s-export-waiver-revocations-put-samsung-and-sk-hynix-in-limbo/

- Reference 13: https://koreajoongangdaily.joins.com/news/2025-12-11/business/industry/SK-hynix-shares-plummet-with-Korea-Exchanges-warning-designation/2475687

- Reference 14: https://www.digrin.com/stocks/detail/MU/price

- Reference 15: https://www.investing.com/equities/samsung-electronics-co-pref-historical-data

- Reference 16: https://www.skhynix.com/ir/UI-FR-IR02/

- Reference 17: https://twelvedata.com/markets/150300/stock/krx/005930/historical-data

- Reference 18: https://www.trendforce.com/news/2025/09/19/news-japan-pledged-jpy-536-billion-to-micron-escalating-global-semiconductor-subsidy-race/

- Reference 19: https://www.semicone.com/article-295.html

- Reference 20: https://www.tomshardware.com/tech-industry/semiconductors/microns-plans-for-an-additional-dram-fab-in-hiroshima-delayed-until-2027

- Reference 21: https://www.afslaw.com/perspectives/alerts/bis-revokes-veu-authorizations-foreign-owned-chip-factories-china

- Reference 22: https://www.federalregister.gov/documents/2025/09/02/2025-16735/revocation-of-validated-end-user-authorizations-in-the-peoples-republic-of-china

- Reference 23: https://www.semicone.com/article-285.html

- Reference 24: https://rhg.com/research/was-made-in-china-2025-successful/

- Reference 25: https://www.techpowerup.com/343119/samsung-reallocates-nand-production-to-dram-across-korean-fabs

- Reference 26: https://koreajoongangdaily.joins.com/news/2025-12-21/business/industry/Samsung-SK-hynix-profit-to-reach-68-billion-each-on-AI-supercycle/2482685

- Reference 27: https://investors.micron.com/static-files/530bd7ed-a8c8-4687-af4a-8c129f740e09

- Reference 28: https://www.trendforce.com/news/2025/12/18/news-micron-hikes-capex-to-20b-with-2026-hbm-supply-fully-booked-hbm4-ramps-2q26/

- Reference 29: https://www.techpowerup.com/344206/micron-forecasts-dram-shortages-beyond-2026

- Reference 30: https://www.mk.co.kr/en/business/11497486

- Reference 31: https://markets.financialcontent.com/wral/article/tokenring-2025-12-18-the-memory-wall-why-hbm4-is-the-new-frontier-in-the-global-ai-arms-race

- Reference 32: https://www.trendforce.com/news/2025/12/16/news-sk-hynix-samsung-reportedly-deliver-paid-hbm4-samples-to-nvidia-ahead-of-1q26-contract-finalization/

- Reference 33: https://investors.micron.com/static-files/088991c5-a249-4f66-a0a6-258d9b66f3f9