DEEP RESEARCH · KOSDAQ REVITALIZATION

2025 KOSDAQ Revitalization: Structural Reform and Beneficiary Sectors

A comparison with the 2018 policy and a map of how the KRW 150 trillion National Growth Fund, pension funds, and stricter delisting rules may reshape the market

0. Bottom line first

The difference in the 2025 KOSDAQ plan is that it is not just a liquidity injection. It attempts to change listing, delisting, pension-fund demand, and strategic-industry capital supply together. The source expects the KRW 150 trillion National Growth Fund and the delisting threshold for companies below KRW 15 billion market cap to widen the gap between quality innovators and marginal companies.

Official fact: The source says KOSDAQ opened in 1996 at 1,000 points and was still around the 900 level as of late December 2025. It also says the 2018 KOSDAQ venture fund offered a 10% income deduction, capped at KRW 3 million per person, and a 30% priority allocation of KOSDAQ IPO shares, attracting about KRW 2.9 trillion in the first three months.

Interpretation: If 2018 was a many-births policy, 2025 is closer to a many-births-and-many-deaths policy: admit good companies and remove weak ones. Investors should focus less on the index as a whole and more on sectors where policy capital meets global demand.

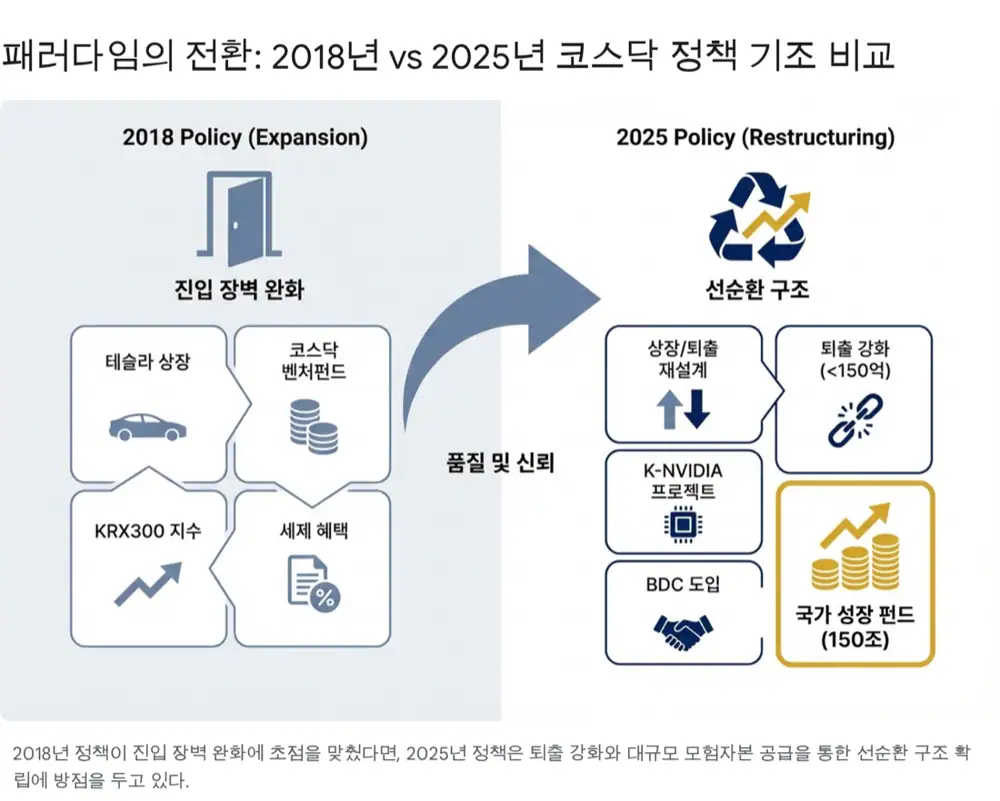

1. 2018 policy: achievements and limits

Tesla listing rules

Loss-making companies could list if growth potential was clear. The source mentions diversified criteria such as KRW 50 billion market cap and 20% sales growth.

KOSDAQ venture fund

Tax deduction and 30% IPO priority allocation created early inflows, but the source notes side effects such as excessive mezzanine issuance and insufficient verification.

KRX300

The KOSPI/KOSDAQ 300-stock index tried to induce pension buying, but it remained a recommendation and pension KOSDAQ exposure stayed around 2-3%.

2. 2025 policy: structural force

The source reads the 2025 plan as qualitative upgrading plus structural force. Governance reform includes a Book-in-Book structure that evaluates the KOSDAQ division separately and stronger KOSDAQ market-committee expertise requirements, such as more than 10 years of venture, VC, or technology experience.

- Customized technology listing: AI, energy such as ESS and renewables, and space receive sector-specific review standards and standing technical advisors.

- Stricter exits: The source says delisting of companies with market cap below KRW 15 billion begins in earnest from 2026.

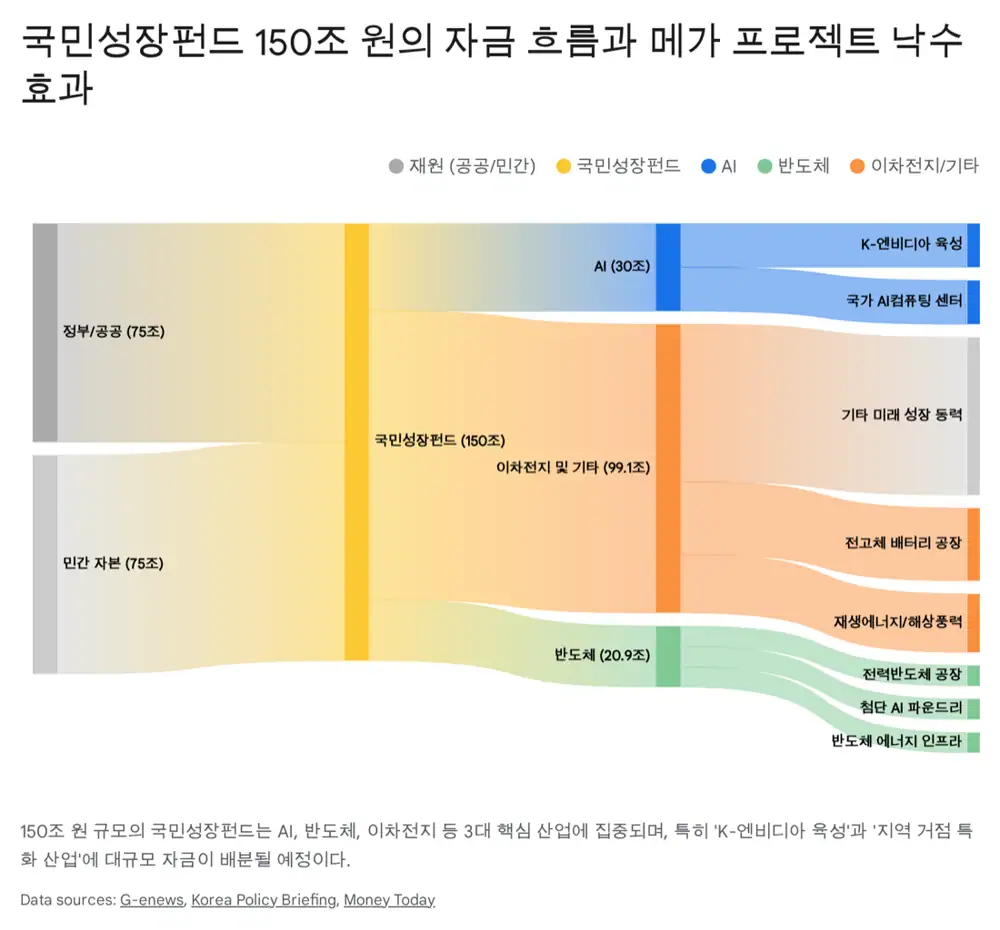

- National Growth Fund: KRW 150 trillion, with KRW 30 trillion per year over five years, targeted at AI, semiconductors, batteries, and other strategic industries.

- Regional allocation: More than 40% of fund capital is described as going to non-metropolitan regional industries.

3. 2018 versus 2025

| Item | 2018 policy | 2025 policy | Implication |

|---|---|---|---|

| Philosophy | Quantitative expansion | Qualitative upgrading | From indiscriminate listings to verified innovation |

| Listing | Tesla rules | Customized tech listings for AI, space, etc. | From broad easing to sector-specific review |

| Capital supply | KRW 300bn KOSDAQ scale-up fund | KRW 150tn National Growth Fund | The source describes a 500x increase in scale |

| Tax | KRW 30m deduction cap | Raised to KRW 50m | Stronger incentive for wealthy investors |

| Pension funds | KRX300 recommendation | Force through fund-evaluation guidelines | KOSDAQ exposure becomes an evaluation variable |

| Delisting | Substantive review focus | Market cap below KRW 15bn | Market assessment becomes a survival criterion |

4. Market expectations versus actual policy

Market participants expected an extension of the Value-Up program, such as shareholder-return incentives and clearer tax benefits. The source argues the actual policy instead contains both a demand-side surprise and a supply-side shock. The KRW 150 trillion fund is framed as about 30% of the roughly KRW 487 trillion KOSDAQ market capitalization.

Interpretation: In the short term, delisting-risk companies may become more volatile. Over the medium term, removing marginal companies and concentrating demand into quality tech firms could make stock-level dispersion much larger than index movement.

5. Beneficiary sectors and company matrix

The source links U.S. Genesis Mission, new trade order, manufacturing reshoring, and AI data-center power demand with three beneficiary areas: AI/robots, power/energy, and space.

| Sector | Company | Investment point | Policy/macro link |

|---|---|---|---|

| AI/robots | Lunit (328130) | Global medical AI leader, listed through technology special listing in 2022 | AI healthcare and data-center AI-service demand |

| AI/robots | Rainbow Robotics (277810) | Collaborative and biped robot platform, Samsung Electronics investment | Manufacturing reshoring and Physical AI |

| Power/energy | Cheryong Electric (033100) | U.S. transformer shortage and rising export exposure | Grid modernization and energy infrastructure investment |

| Power/energy | Seojin System (178320) | ESS parts and telecom equipment cases, global ESS growth | Data-center backup power and energy efficiency |

| Power/energy | Iljin Power (094820) | Power-plant maintenance and nuclear equipment | SMR/nuclear ecosystem restoration and AI power demand |

| Space | Satrec Initiative (099320) | Satellite-system exports and Hanwha Group space synergy | Customized space listings and private space development |

6. Conclusion

The 2025 KOSDAQ revitalization plan is more than a market “boom-up”; it is a market-structure reform. Investors should select companies with real earnings and verified technology within AI, semiconductors, robots, power infrastructure, and space, where policy capital is concentrated. Companies with weak market capitalization and weak business substance face higher risk under stricter delisting rules.

Sources

- Original blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117368858

- Source 1: https://www.kcmi.re.kr/common/downloadw?fid=22029&fgu=002001&fty=004003

- Source 2: https://www.businesspost.co.kr/BP?command=article_view&num=68057

- Source 3: https://www.mk.co.kr/news/business/8772788

- Source 4: https://www.newspim.com/news/view/20181228000158

- Source 5: https://www.fsc.go.kr/po010101/73347?srchCtgry=1&curPage=50&srchKey=&srchText=&srchBeginDt=&srchEndDt=

- Source 6: https://www.shinhansec.com/siw/wealth-management/fund/kosdaqventure/view.do

- Source 7: https://mobile.newsis.com/view/NISX20180326_0000263217

- Source 8: https://www.businesspost.co.kr/BP?command=article_view&num=72186

- Source 9: https://www.mk.co.kr/news/stock/8149361

- Source 10: https://www.hankyung.com/article/2025112703911

- Source 11: https://www.g-enews.com/article/Finance/2025/12/202512191539323683a6e8311f64_1

- Source 12: https://www.korea.kr/news/policyNewsView.do?newsId=148956795

- Source 13: https://www.mt.co.kr/finance/2025/12/19/2025121906013331372

- Source 14: https://www.youtube.com/watch?v=nwh8Vwb2dFY

- Source 15: https://www.lunit.io/en/media-hub/ai-based-cancer-solution-pioneer-lunit-makes-market-debut/

- Source 16: https://www.judal.co.kr/?view=stockList&themeIdx=25

- Source 17: https://www.investing.com/equities/rainbow-robotics

- Source 18: https://www.judal.co.kr/?view=stockList&themeIdx=541

- Source 19: https://stockanalysis.com/quote/kosdaq/033100/

- Source 20: https://www.youtube.com/watch?v=YXy4kjDqmQs

- Source 21: https://www.investing.com/equities/seojin-system-co-ltd

- Source 22: https://www.judal.co.kr/?view=stockList&themeIdx=94

- Source 23: https://simplywall.st/stocks/kr/capital-goods/kosdaq-a094820/iljin-power-shares/news/what-iljin-power-co-ltds-kosdaq094820-27-share-price-gain-is

- Source 24: https://simplywall.st/stocks/kr/capital-goods/kosdaq-a099320/satrec-initiative-shares/information

- Source 25: https://www.tradingview.com/symbols/KRX-099320/