DEEP RESEARCH · AAM TOP FOUR

Global AAM Top Four: Technology, Market, and Regulatory Moats at Joby, Archer, EHang, and Vertical

A comparison of certification, manufacturing partners, autonomy, and financial runway in next-generation air mobility

0. Bottom line first

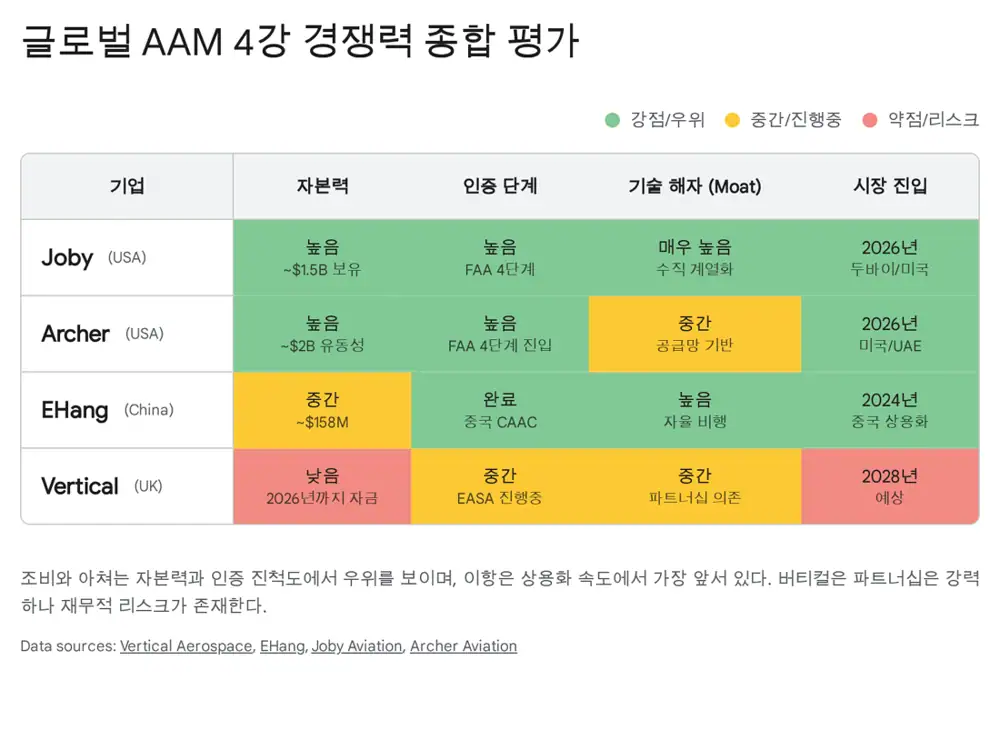

The decisive AAM variables for 2025-2026 are certification, capital, manufacturing, and early operating rights, not aircraft specs alone. My base case is a multipolar market: Joby and Archer in premium U.S. urban shuttles, EHang in autonomous tourism and logistics across Asia and emerging markets, and Vertical in the European safety-led market.

Joby Aviation

Vertical integration, six tilt rotors, 100+ mile range, 200 mph top speed, and 45.2 dBA NASA-tested low noise define the case.

Archer Aviation

A pragmatic strategy that lowers certification and production risk through Tier-1 suppliers and Stellantis manufacturing support.

EHang

The pilotless EH216-S and early CAAC approval put EHang on a different path in tourism, logistics, and emerging markets.

Vertical Aerospace

EASA SC-VTOL 10^-9 safety ambition and 1,500+ conditional pre-orders are strong, but cash runway is the tightest.

1. Industry inflection: from prototypes to certification and production

Official fact: The source frames AAM, covering both UAM and RAM, as entering the industrialization phase in 2025 as battery energy density, distributed electric propulsion, and decarbonization pressure converge.

Official fact: The source cites forecasts from Morgan Stanley and other global institutions that the AAM market could exceed USD 1 trillion, roughly KRW 1,300 trillion, around 2040.

Interpretation: This is no longer the phase where hundreds of startups survive on prototypes. The valley of death now filters for companies that can fund R&D, absorb certification uncertainty, and build early infrastructure.

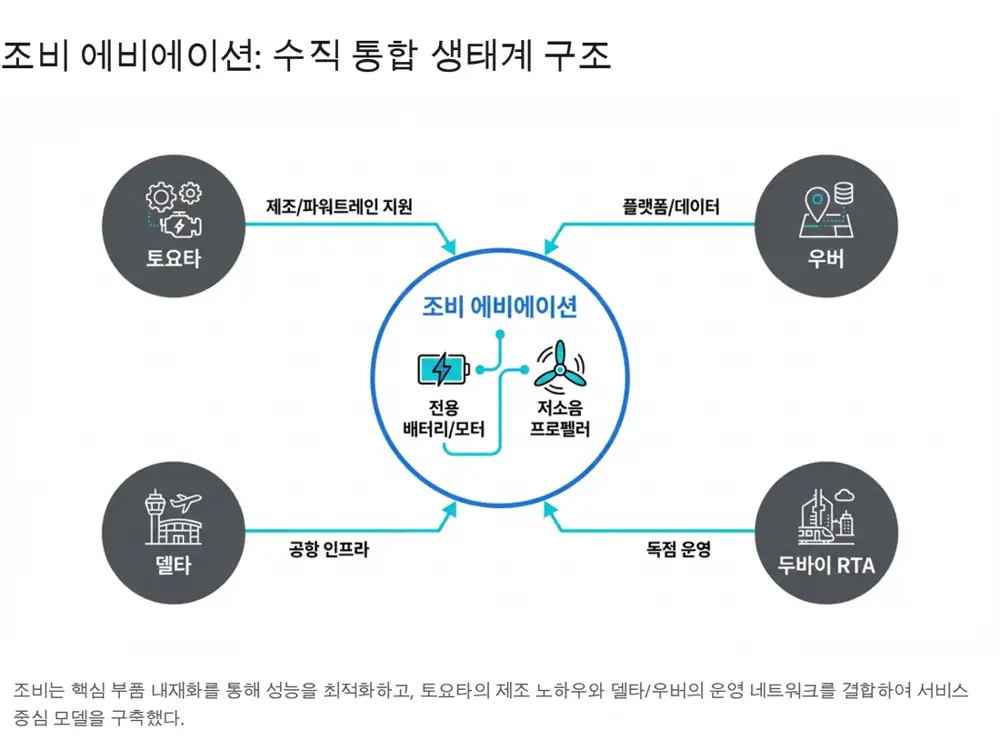

2. Joby Aviation: vertical integration and premium air taxi operations

Official fact: Joby pursues a design-to-operate model. Its S4 uses six tilt rotors, taking off vertically and tilting forward in cruise so the wing supplies lift.

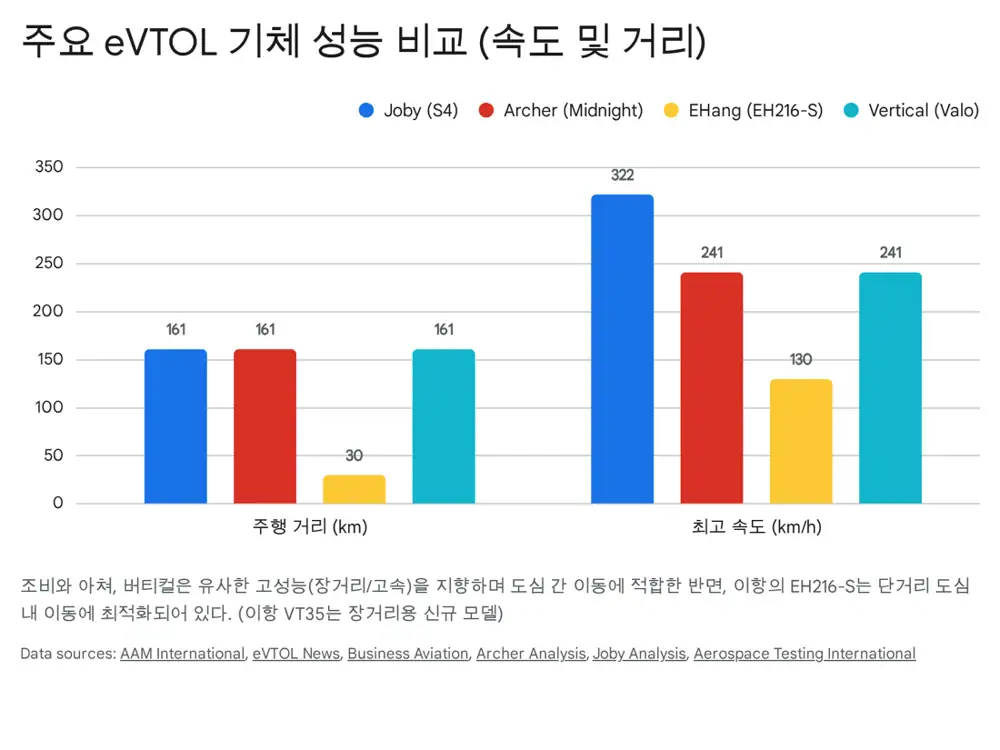

- The source cites Joby range above 100 miles and top speed of 200 mph.

- In NASA joint testing, the S4 measured 45.2 dBA at 1,640 feet, about 500 meters, which the source describes as roughly 100 times quieter than a helicopter.

- Initial markets include New York, Los Angeles, and Dubai. The six-year exclusive agreement with Dubai's RTA is presented as a right to begin exclusive commercial service in early 2026.

- Delta supports airport shuttle demand, the Uber Elevate acquisition supports app-based booking, and Toyota strengthens manufacturing and quality systems.

Interpretation: Joby's edge is that aircraft performance, low noise, and operating rights reinforce each other. The model is capital intensive, but Toyota, Uber, and Delta make the early commercialization path unusually complete.

3. Archer Aviation: validated supply chain and practical manufacturing

Official fact: Archer uses global Tier-1 suppliers such as Honeywell, Garmin, and Safran rather than developing every component internally. The source says about 80% of aircraft parts are sourced from proven suppliers.

Official fact: The Midnight aircraft uses 12 propellers: six tilt and six fixed lift rotors. The source cites 150 mph top speed, 100-mile range, and optimization for 20-50 mile urban shuttle routes.

- Archer works with Molicel on 21700 cylindrical lithium-ion cells.

- United Airlines provides early demand credibility through a USD 1 billion aircraft purchase agreement and a USD 10 million pre-delivery payment.

- In Japan, Archer signed an agreement with Soracle, the JAL and Sumitomo joint venture, for up to USD 500 million of aircraft sales and operations.

- Stellantis is the exclusive contract manufacturing partner, bringing the Georgia facility and auto-industry production expertise.

Interpretation: Archer's moat is execution speed rather than perfectionism. Certified suppliers and auto-style production reduce development risk and initial capex burden.

4. EHang: pilotless autonomy and Chinese regulatory lead

Official fact: EHang's EH216-S has no cockpit. Flights are managed from ground command-and-control centers over 4G/5G networks. The source sees the core capability in multi-aircraft control and routing software, not only hardware.

Official fact: In October 2023, EHang received what the source describes as the world's first type certificate for an unmanned aircraft system from CAAC, followed by production and airworthiness certificates.

- Priority markets are China, Southeast Asia, the Middle East, and Brazil, where regulatory flexibility and China-linked cooperation can be stronger.

- The EH216-S range is about 30 km, making it more suitable for tourism, last-mile logistics, firefighting, and emergency response than inter-city transport.

- EHang recently introduced the VT35 long-range model with about 200 km range to expand the addressable market.

- Gotion High-Tech supports batteries, while Enpower works with EHang on electric motors and controllers.

Interpretation: EHang may be slower to enter Western markets, but it can accumulate autonomous operating data earlier. Removing pilot labor is a decisive unit-economics variable.

5. Vertical Aerospace: European safety standard and capital risk

Official fact: Vertical Aerospace's VX4, recently named Valo, targets EASA SC-VTOL certification. The source says this standard requires 10^-9 safety, or one catastrophic failure per billion flight hours, comparable with commercial airliners.

Official fact: Vertical develops through a partner consortium including Honeywell, GKN, Leonardo, and Molicel. The source says it has more than 1,500 conditional pre-orders worth about USD 6 billion from American Airlines, Virgin Atlantic, JAL, Avolon, and others.

Interpretation: Vertical's strength is conservative safety design that airlines like, plus a large order book. The challenge is that after Rolls-Royce exited electric propulsion, Vertical has had to raise technical independence through its battery center and Molicel partnership, while cash is tighter than peers.

6. Technology, regulation, and financial comparison

| Category | Joby S4 | Archer Midnight | EHang EH216-S | Vertical Valo |

|---|---|---|---|---|

| Propulsion | Six tilt rotors | Six tilt + six lift | Sixteen multicopter rotors | Four tilt + eight lift |

| Battery strategy | Pouch cells, in-house pack design | Molicel 21700 cylindrical | Gotion and others, pouch/prismatic | Molicel 21700 cylindrical |

| Noise position | 45.2 dBA measured | 45 dBA target | Mid, due to multicopter traits | 50 dBA target |

| Autonomy | Piloted, later transition | Piloted | Fully pilotless from day one | Piloted, later transition |

| Manufacturing | Toyota TPS | Stellantis contract production | Yunfu in-house factory | Partner production |

| Q3 2025 financial runway | About USD 978M cash and short-term investments | About USD 1.64B+ liquidity including recent raises | Lower cash but product revenue already exists | About USD 117M cash |

United States: pragmatic path

Joby and Archer follow powered-lift special rules built around Part 23. The source describes safety targets around 10^-7 to 10^-8.

Europe: uncompromising safety

Vertical is pursuing the 10^-9 standard. Cost and schedule burden are high, but success would create a global gold standard.

China: state-led fast track

EHang benefits from low-altitude-economy policy and special unmanned-aircraft conditions, allowing early commercial data accumulation.

7. Final outlook: segmentation over a single winner

- Market leadership: Joby has the best mix of technical maturity, capital, and Toyota/Uber partnerships. Dubai exclusivity is a key test of the early revenue model.

- Fast follower: Archer is catching up through Stellantis production support and United Airlines demand.

- Game changer: EHang can dominate tourism and selected Asian/Middle Eastern markets through autonomy. Even if Western access is delayed, China and emerging markets can support an independent ecosystem.

- High risk, high reward: Vertical has attractive technology and orders, but EASA complexity and limited cash make 2026 financing and certification milestones critical.

In conclusion, I do not expect one company to monopolize AAM. A more likely structure is Joby and Archer splitting U.S. premium urban shuttles, EHang leading Asian tourism and logistics, and Vertical plus other European names leading safety-led European routes. Investors should watch certification milestones and cash burn before anything else.

Sources

- Naver Blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117306714

- Vertical VX4 - eVTOL Aircraft for Urban Air Mobility: https://www.aaminternational.com/projects/vertical-vx4/

- Aviation Week - Joby Versus Archer: https://aviationweek.com/business-aviation/aircraft-propulsion/joby-versus-archer-vertical-integration-strategy-key-split

- Joby low-noise NASA testing: https://www.jobyaviation.com/news/joby-revolutionary-low-noise-footprint-nasa-testing/

- Joby 8-K 2023-06-28: https://ir.jobyaviation.com/sec-filings/all-sec-filings/content/0001819848-23-000253/0001819848-23-000253.pdf

- Joby 8-K 2023-08-02: https://ir.jobyaviation.com/sec-filings/all-sec-filings/content/0001819848-23-000318/0001819848-23-000318.pdf

- Joby UAE air taxi launch: https://ir.jobyaviation.com/news-events/press-releases/detail/87/joby-to-launch-air-taxi-service-in-uae

- Flying Magazine - Joby Dubai 6-year deal: https://www.flyingmag.com/joby-aviation-signs-exclusive-6-year-deal-for-electric-air-taxi-service-in-dubai/

- Joby company analysis Google Drive note: https://drive.google.com/open?id=1xBj5h60w2eA0nHtuIF9XSnWe4dSHrXSwAmSDJUhD0JU

- Joby and Toyota supply agreement: https://www.jobyaviation.com/news/joby-and-toyota-expand-partnership-long-term-supply-agreement/

- Toyota and Joby corporate announcement: https://global.toyota/en/newsroom/corporate/41788284.html

- JDA Solutions eVTOL TC applicants comparison: https://jdasolutions.aero/blog/lessons-for-insightful-comparison-of-2-leading-evtol-tc-applicants/

- Archer selects Molicel battery cells: https://investors.archer.com/news/news-details/2022/Archer-Selects-Molicel-to-Supply-Battery-Cells-for-its-Production-Midnight-Aircraft/default.aspx

- AviTrader - Molicel to supply Archer Midnight: https://avitrader.com/2022/11/17/molicel-to-manufacture-and-supply-battery-cells-for-archers-evtol-aircraft-midnight/

- SmartBuy - Archer vs Joby technical and market analysis: https://smartbuy.alibaba.com/best-selling/best-air-lift-archer-vs-joby

- Archer company analysis Google Drive note: https://drive.google.com/open?id=1N9aPCUtmqCEE6IYAzbuWwv8M3T-q0WY-InBegRPzc8E

- Business Air News - Archer Japanese ecosystem: https://www.businessairnews.com/mag_story.html?ident=35729

- Archer Soracle up to $500M agreement: https://investors.archer.com/news/news-details/2024/Japan-Airlines-and-Sumitomo-Corporations-Joint-Venture-Company-Soracle-Announces-Agreement-Including-Intended-Purchase-Of-Up-To-500M-of-Electric-Aircraft-From-Archer/default.aspx

- EHang EH216-S UAM: https://www.ehang.com/ehang216s/

- EHang 184 passenger AAV: https://www.ehang.com/ehang184/

- EHang CAAC production certificate: https://www.ehang.com/news/1058.html

- EHang CAAC type certificate: https://www.ehang.com/news/990.html

- EHang Spain-China AAM cooperation: https://www.ehang.com/news/1308.html

- Urban Air Mobility News - EHang Brazil ANAC certificate: https://www.urbanairmobilitynews.com/emerging-regulations/ehang-216-s-granted-experimental-flight-certificate-from-brazils-anac/

- The FLY Report - EHang VT35: https://news.flyjets.com/article/ehang-introduces-its-vt35-long-range-evtol-aircraft/

- Aerospace Testing International - EHang VT35: https://www.aerospacetestinginternational.com/news/ehang-launches-vt35-long-range-autonomous-evtol.html

- CnEVPost - EHang VT35 200-km range: https://cnevpost.com/2025/10/13/ehang-launches-vt35-evtol/

- EHang and Gotion partnership: https://www.ehang.com/news/1231.html

- EHang and Enpower partnership: https://www.ehang.com/news/1133.html

- Vertical Aerospace - Meet Valo: https://vertical-aerospace.com/meet-valo/

- MarketBeat - Vertical Valo launch: https://www.marketbeat.com/originals/verticals-valo-launch-a-commercial-leap-disguised-as-a-dip/

- Vertical advanced VX4 prototype PDF: https://vertical-aerospace.com/wp-content/uploads/2024/07/Vertical-Aerospace-Unveils-Advanced-VX4-Prototype.pdf

- Business Wire - Vertical transition flight testing: https://www.businesswire.com/news/home/20251219805325/en/Vertical-Aerospace-Progresses-Towards-Full-Piloted-Transition-Flight

- The FLY Report - Rolls-Royce electric propulsion exit: https://news.flyjets.com/article/in-the-wake-of-rolls-royces-exit-from-electric-propulsion-which-industry-players-will-emerge-victorious/

- Vertical Energy Centre PDF: https://vertical-aerospace.com/wp-content/uploads/2023/11/Vertical-announces-the-opening-of-the-Vertical-Energy-Centre-the-UK_s-most-advanced-aerospave-battery-facility.pdf

- The Air Current - eVTOL safety debate: https://theaircurrent.com/industry-strategy/special-report-evtol-safety-continuum-10-9/

- eVTOL News - EASA and FAA guidance: https://evtol.news/news/easa-and-faa-advance-evtol-guidance

- The Air Current - Joby accident and regulatory divide: https://theaircurrent.com/industry-strategy/joby-accident-regulatory-divide-easa-faa/

- Aviation International News - China issues EHang TC: https://www.ainonline.com/news-article/2023-10-13/china-issues-worlds-first-evtol-aircraft-type-certificate-ehangs-eh216-s

- ICAO - EHang EH216-S special conditions: https://www.icao.int/sites/default/files/Meetings/a41/Documents/WP/wp_444_en.pdf

- Business Aviation - FAA EASA China eVTOL certification: https://businessaviation.aero/evtol-news-and-electric-aircraft-news/advanced-air-mobility/faa-easa-and-china-contrasting-approaches-to-evtol-certification-and-urban-air-mobility

- Joby Q3 2025 financial results: https://ir.jobyaviation.com/news-events/press-releases/detail/157/joby-reports-third-quarter-2025-financial-results

- Archer quarterly results: https://investors.archer.com/financials/quarterly-results/default.aspx

- Vertical Aerospace Q3 update PDF: https://vertical-aerospace.com/wp-content/uploads/2025/11/Vertical-Aerospace-Provides-Third-Quarter-Update-Demonstrating-Momentum-on-Transition-Flight-Testing-Business-Plan-Updates-and-Best-in-Class-Aircraft.pdf