DEEP RESEARCH · APPLOVIN

AppLovin: AI Performance Marketing and a Structural Quantum Jump

Whether Axon 2.0, the Apps divestiture, and cash generation justify a pure-software platform re-rating.

0. Bottom line first

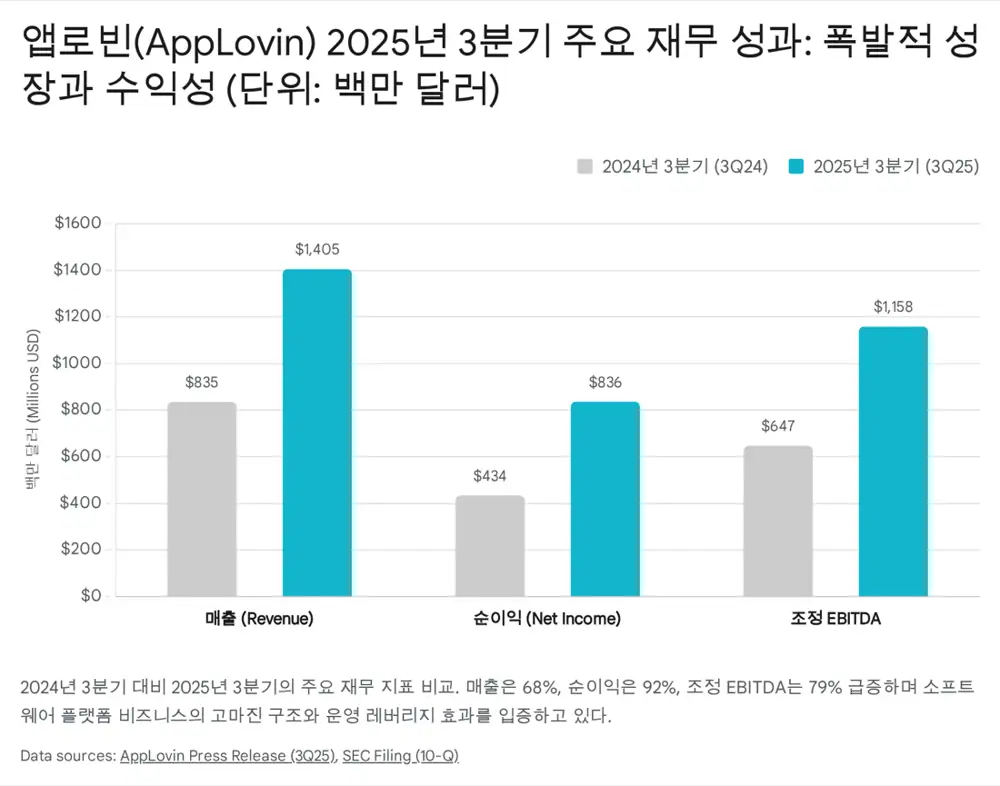

AppLovin is no longer mainly a mobile-game company; the core is AI advertising infrastructure. Q3 2025 revenue of $1.41B, 68% YoY growth, and an 82% adjusted EBITDA margin show Axon 2.0 converting technology into financial results.

1. Investment highlights and risks

The source presents an overweight view based on three points: the Axon 2.0 moat, the June 2025 Apps divestiture and pure-software transition, and powerful free cash flow plus buybacks.

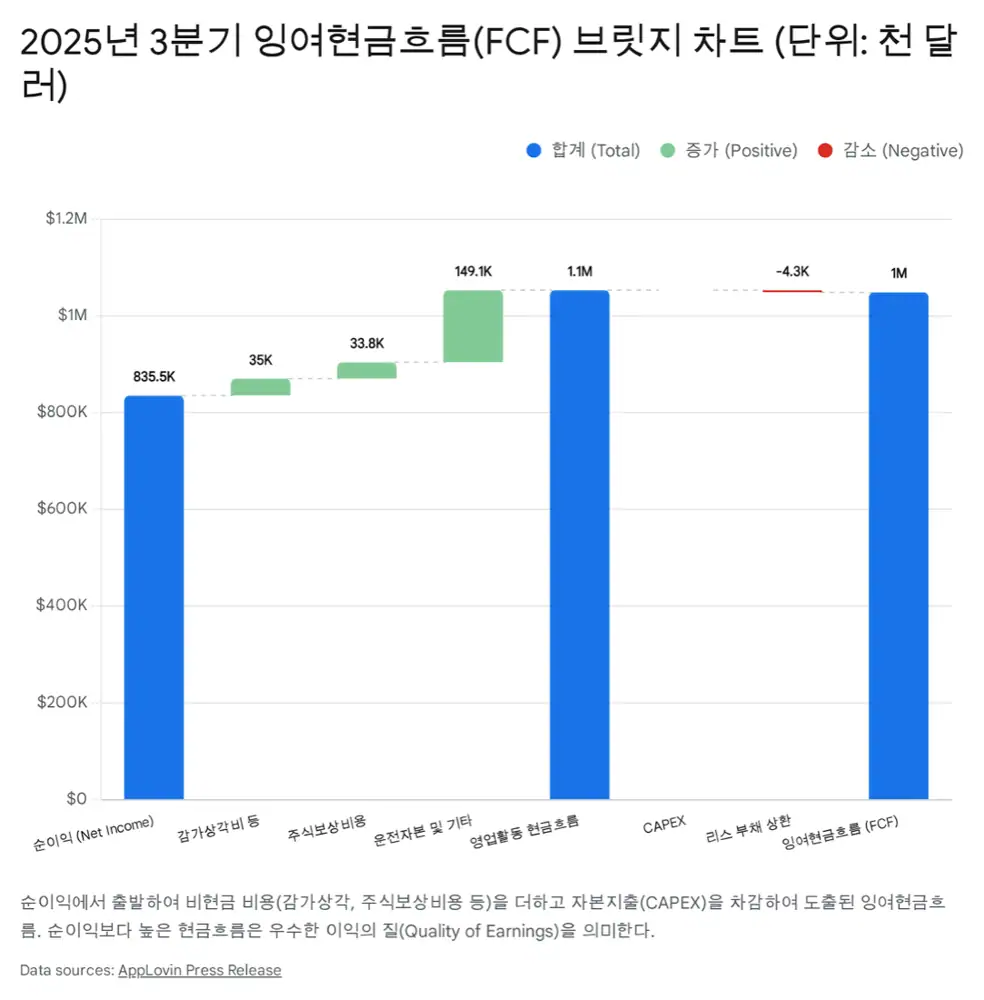

- Q3 2025 free cash flow is cited at $1.05B.

- Q3 buybacks were $571M, and an additional $3.2B program was authorized.

- Key risks are mobile-game maturity, Google Privacy Sandbox, and volatility from large M&A ambitions such as TikTok.

2. From content company to AI platform

Founded in 2011, AppLovin grew with the mobile app ecosystem. The Apps segment, including Lion Studios, generated cash but created possible conflicts with game-developer platform customers. In 2025, AppLovin sold Apps to Tripledot and classified it as discontinued operations from Q2 2025.

Interpretation: This was not just a low-margin cleanup; it changed the company’s identity from content to AI advertising infrastructure. The source says 100% of revenue now comes from the software platform.

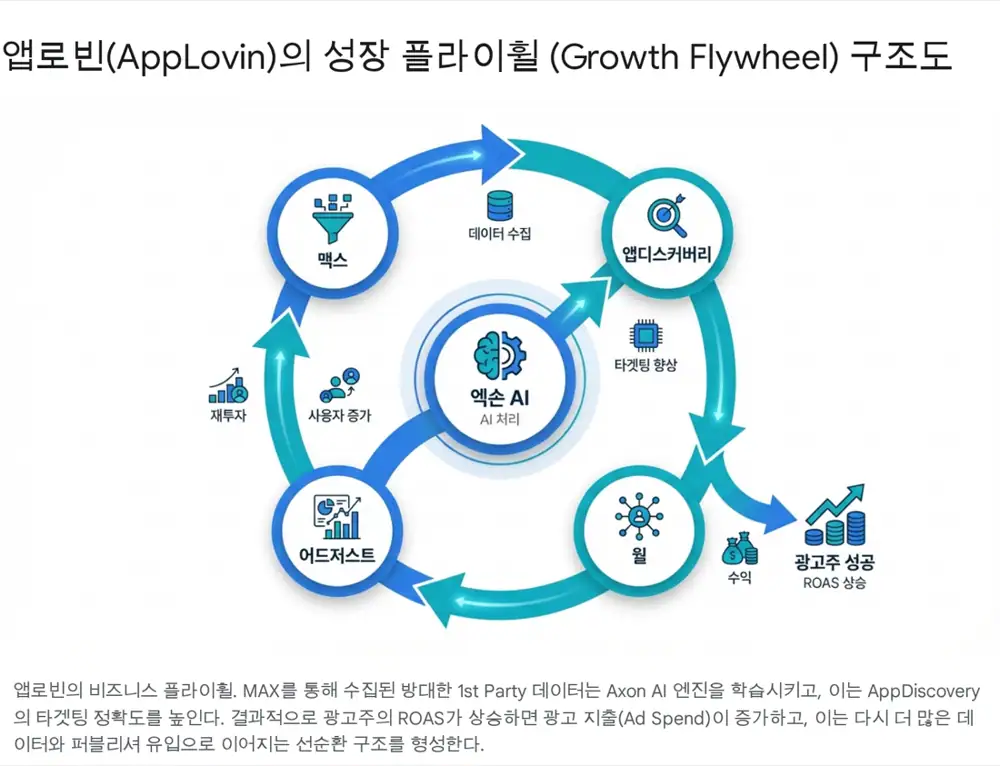

3. Solution portfolio

User acquisition

Axon AI matches optimal impressions in real-time auctions and expands TAM through e-commerce.

Monetization

In-app bidding maximizes publisher inventory value and acts as a data pipeline.

Measurement

Attribution and fraud prevention support trust.

CTV & streaming

Extends advertising inventory beyond mobile into CTV and streaming.

4. Financials and capital allocation

| Item | Source number | Read-through |

|---|---|---|

| Q3 2025 revenue | $1.405B, up 68% from $835M | Axon 2.0 and new advertisers |

| Nine-month revenue | $3.822B, up about 72% | Structural growth |

| R&D expense | $43.9M, down about 46% from $80.8M | AI automation and efficiency |

| Operating cash flow | $1.053B in Q3; $2.657B for nine months | Software-like cash conversion |

| FCF | $1.049B in Q3 | Asset-light model with CAPEX near $0.1M |

| Cash | $1.667B | More than doubled from $697M at 2024 year-end |

5. Valuation and conclusion

The source says annualized Q4 2025 adjusted EBITDA guidance of $1.29B-$1.32B implies potential annual EBITDA above $5B. With more than 60% revenue growth and nearly 80% EBITDA growth, it frames AppLovin as a high-growth GARP candidate.

My view is positive but risk-aware. Regulation, competition, ad-cycle weakness, FX, and large M&A remain variables. Still, based on current numbers, AppLovin looks like a structural winner that absorbed privacy headwinds through AI.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117285747

- Reference 1: https://www.gamebizconsulting.com/newsletter/newsletter-may25

- Reference 2: https://www.globalgamesforum.com/news/max-vs-levelplay-9-facts-about-the-mediation-space-in-2025

- Reference 3: https://www.blog.udonis.co/advertising/mobile-advertising-market

- Reference 4: https://sqmagazine.co.uk/mobile-advertising-statistics/

- Reference 5: https://newzoo.com/resources/blog/year-in-review-2025-to-date

- Reference 6: https://www.pcgamer.com/gaming-industry/analyst-firm-says-the-games-market-is-expected-to-reach-a-record-breaking-usd197-billion-by-the-end-of-2025-driven-primarily-by-stronger-than-expected-performance-on-pc-and-mobile/

- Reference 7: https://ruskinconsulting.com/the-impact-of-googles-privacy-updates-on-digital-advertising-in-2025/

- Reference 8: https://groas.ai/post/googles-2025-privacy-sandbox-rollout-what-advertisers-need-to-know

- Reference 9: https://naavik.co/digest/mobile-ads-unity-struggles-as-applovin-leads/