DEEP RESEARCH · VERTICAL AEROSPACE (EVTL)

Vertical Aerospace (EVTL) — The Capital-Efficient OEM Bet on Urban Air Mobility 2030

A UK eVTOL maker pursuing the Airbus/Boeing OEM playbook, staring down the Valley of Death

0. Bottom line first

Vertical Aerospace (NYSE: EVTL) survived the 2025 eVTOL shake-out — but the real test starts now. Lilium's collapse showed this is a capital war, and the market's scorecard has shifted from "innovation" to viability and capital efficiency.

Official fact: As of 4 November 2025, cash on hand stands at roughly £89M (≈ US$117M), runway extending to mid-2026. Vertical estimates it needs roughly US$700M in additional funding to reach type certification in 2028 — a financing gap of roughly US$600M.

Interpretation: A large funding round in H1 2026 is non-negotiable. The cost of success is dilution; the cost of failure is a Going Concern warning. This is the textbook High Risk / High Reward optionality — to be held only as a small portfolio position.

2025 transition flight

Completing the piloted transition flight envelope validates the core technical thesis.

H1 2026 mega-round

Strategic investment, UK ATI grants and the Jefferies ATM combined must secure US$600M+.

Certification delay or funding miss

Any slip into 2029+ risks a cash-burn collapse — the Lilium scenario in repeat.

1. Introduction — AAM consolidation and Vertical's inflection

2025 will be remembered as the year of structural reordering in the global Advanced Air Mobility (AAM) and eVTOL sector. The early bloom — when hundreds of startups sold pure technical possibility — is over. The industry has entered a shake-out in which a small group of leaders advance into real certification work while liquidity-strapped competitors are forced out.

Germany's Lilium — once a flagship European eVTOL company — filed for insolvency in 2025, after a fresh investment round fell through. That single event made it brutally clear: this is no longer a contest of technical idealism but a war of capital and commercial reality. Institutional investors and analysts have rewritten the primary evaluation metric from "innovation" to viability and capital efficiency.

Against that backdrop, the UK's Vertical Aerospace has taken a different — riskier, but cleaner — position. While US leaders Joby Aviation and Archer Aviation pursue a vertically-integrated operator model and burn through enormous capital to control the whole stack, Vertical commits purely to an OEM (Original Equipment Manufacturer) model — the Airbus/Boeing playbook. It designs, certifies, assembles and sells aircraft, and leaves operations to existing airlines (American Airlines, Virgin Atlantic, JAL) and lessors (Avolon).

2. Company overview and fundamentals — reinterpreting the OEM model

2.1 Corporate DNA and the Bristol cluster

Vertical Aerospace was founded in 2016 by Stephen Fitzpatrick, founder of UK energy company OVO, and is headquartered in Bristol, UK. Bristol is decisive for Vertical's DNA: it is one of Europe's largest aerospace clusters, home to Rolls-Royce, Airbus, GKN and others, with a deep engineering talent pool and mature aerospace supply chain. That access has minimised the "manufacturing learning curve" mistakes typical of Silicon Valley-style tech startups.

2.2 Core capabilities and differentiation

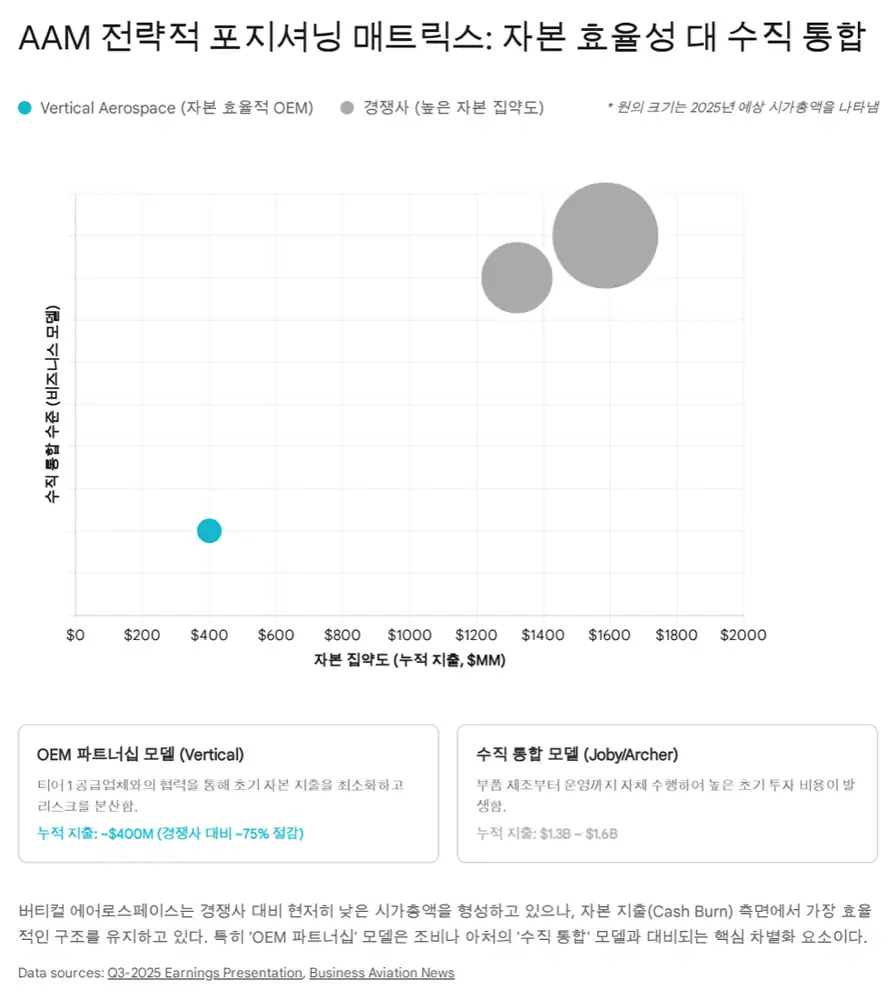

Asset-light manufacturing

Rather than vertically integrate, Vertical partners with global Tier-1 suppliers — diffusing development risk and lowering fixed costs. While competitors spend hundreds of millions on their own composite plants, Vertical focuses on design and integration.

In-housed battery tech

Airframe and avionics are outsourced — but the heart of an eVTOL's performance and economics, battery systems and propellers, is developed in-house. This sets up an exclusive position in the future battery replacement market.

Certification-led design

Designed from day one to meet EASA / UK CAA's SC-VTOL standard — requiring 10⁻⁹ safety (one catastrophic failure per billion flight hours), far stricter than the FAA's early benchmark. Slower at first, but the toughest barrier to entry long-term.

2.3 Governance reset — regulatory expertise on the board

In H1 2025 Vertical made decisive changes to its executive team and board. Stuart Simpson serves as CEO with an execution-led leadership style. The most consequential appointment is former EASA Executive Director Patrick Ky joining the board. Ky led global aviation safety standards during his EASA tenure, and his presence dramatically strengthens Vertical's regulatory negotiating power and reduces certification uncertainty. CCO Michael Cervenka, ex-Rolls-Royce, runs the commercialisation strategy.

Interpretation: The intent is unmistakable — to graduate from "tech startup" to mainstream player inside a highly regulated aerospace industry. Patrick Ky's appointment is arguably the single biggest catalyst on Vertical's EASA SC-VTOL certification track.

3. The VX4 programme — technical progress and certification roadmap

3.1 Aircraft characteristics and competitive edge

Vertical's flagship aircraft VX4 is a piloted eVTOL carrying 4 passengers + 1 pilot, targeting a top speed of 150 mph (~241 km/h) and range of 100 miles (~161 km) — optimised for inter-city and airport-shuttle missions. Architecturally it adopts a tilt-rotor with fixed-wing configuration, which delivers far higher cruise energy efficiency than multicopters (e.g. Volocopter) and a simpler, lower-drag, higher-speed structure than lift-and-cruise designs (Archer, Beta). The catch: the tilt mechanism is among the hardest to develop.

The certification-spec design unveiled in November 2025 boasts class-leading cabin space and a six-bag luggage hold (checked + carry-on) — a non-negotiable for real-world airport-shuttle economics. Many competitors sacrifice luggage volume to enlarge the cabin or only support limited cargo, which makes Vertical's design a meaningful differentiator with airline partners. A physical bulkhead between cockpit and cabin further enhances safety and privacy — a clear win for the VIP/business segment that will anchor the early UAM market.

3.2 The 2025 milestone — piloted transition flight

2025 is the year of decisive technical validation for the VX4. In November 2025, Vertical received its Permit to Fly from the UK CAA and immediately entered the piloted transition flight phase. Transition flight — moving from vertical lift (helicopter mode) to wing-borne horizontal flight (airplane mode) — is the pinnacle of eVTOL flight-control technology. Managing aerodynamic instability and smoothly switching thrust regimes is the true measure of engineering maturity.

Vertical has already satisfied all ~200 strict CAA safety requirements through simulation and ground testing, and plans to complete the full transition flight envelope by year-end 2025. On timing alone it lags Joby and Archer, who have already achieved transition flight. Vertical's counter-argument: "European regulatory rigour is much stricter, so the pain front-loaded today is a catalyst that accelerates type certification later." This front-loaded certification pain thesis carries weight, because the CAA supervises with a degree of joint liability over the prototype — meaning regulators already understand the aircraft's design and safety profile in depth.

3.3 Hybrid extensibility — a category-changing wildcard

In May 2025 Vertical officially announced a hybrid-electric derivative alongside the pure-electric VX4. Keeping the same airframe, part of the battery pack is replaced by a small gas turbine generator — pushing range to 1,000 miles (~1,600 km) and payload to 1,200 kg.

Breaks the energy-density ceiling

Solves the range problem imposed by current battery energy density — opening MedEvac, urgent logistics, and remote/island transport markets.

Bypasses infrastructure bottleneck

Operable where charging infrastructure is scarce — maximising TAM. Especially valuable in emerging markets and large-territory countries with slow infrastructure rollout.

Defence market entry

With post-Ukraine European defence spending rising from 2% to 5% of GDP, a low-noise / low-thermal-signature hybrid VX4 has strong potential for military transport and ISR. A stable B2G market that offsets civilian uncertainty.

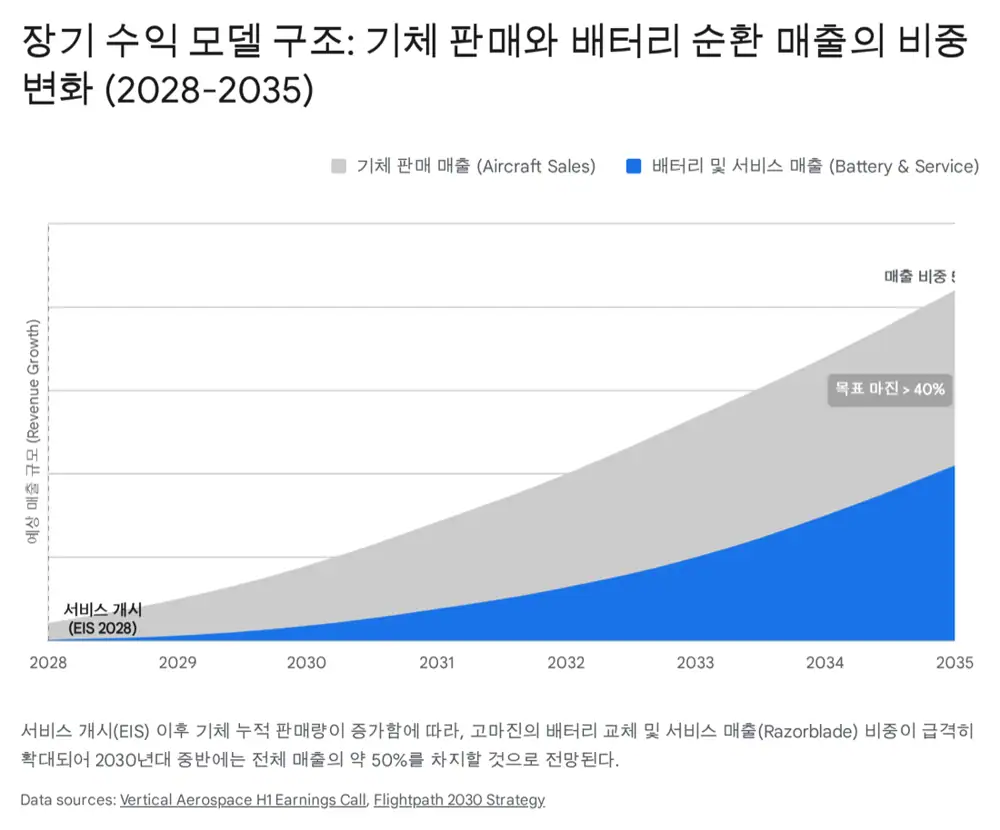

4. The Razor-Razorblade business model — economics of an exclusive battery ecosystem

The most important nuance in Vertical's revenue model is its exclusive battery ecosystem as a recurring-revenue engine. Management explicitly calls it the Razor-Razorblade model, designed to go far beyond a one-off airframe sale into a long-life, high-margin business.

4.1 Structural lock-in

The VX4 is engineered to run only on Vertical's in-house battery packs — an Apple-style closed ecosystem that technically forecloses third-party batteries. Because eVTOL batteries are punished by repeated high-output discharges at takeoff/landing and frequent fast-charging, degradation is rapid: operators must replace batteries 1–2 times per year for safety. By monopolising that replacement market, Vertical builds decades of cash flow that continues long after the airframe is sold.

4.2 Profitability simulation and margin structure

Official fact: Over the long term, management guides for roughly 50% of revenue from airframe sales and 50% from batteries and aftermarket services, targeting a 40%+ gross margin on battery replacements.

Interpretation: That far exceeds normal aircraft-manufacturing margins (10–15%) — an ambitious target to deliver software-like profitability inside a manufacturing business. It is the central pillar behind Vertical's post-2030 goal of US$100M+ net operating cash flow.

4.3 Expansion strategy — gigafactory and external sales

Vertical intends to extend its high-performance battery technology beyond the VX4. A pilot line is being built at the Vertical Energy Center in the UK, and a gigafactory site for mass production is to be selected within the next 12 months. Management signals plans to sell the battery technology externally — to other eVTOLs, high-performance EVs, and industrial drones — which would force a re-rating of Vertical from "aircraft maker" to energy technology company.

5. Manufacturing and supply chain — outsourcing risk, internalising efficiency

Vertical's capital efficiency rests on strong Tier-1 supplier partnerships. By outsourcing the two hardest pieces of aircraft development — airframe and avionics — to best-in-class partners, it dramatically cut CAPEX. That offloads the manufacturing infrastructure that startups typically cannot afford, while certified components reduce overall certification risk.

5.1 Key partnerships

Aciturri Aerostructures

Spanish aircraft-structures specialist supplying major structures on the Airbus A320 and Boeing 787. Owns design and manufacture of the VX4's wings, fuselage and empennage. Vertical avoids building its own composite plant and inherits Aciturri's serial-production know-how.

Honeywell

Supplies the VX4's flight-control computers and integrated Anthem Flight Deck. A long-term supply agreement through 2035 locks in stable component supply and certification support. Honeywell's systems are already validated on numerous commercial aircraft, sharply lowering software/hardware reliability risk with regulators.

GKN Aerospace

Initially owned wings and wiring systems; the scope has narrowed to specialised high-difficulty areas such as the Electrical Wiring Interconnection System (EWIS). Guarantees the reliability of what is effectively the aircraft's nervous system.

Leonardo

Early fuselage-development partner; the role has shifted as Aciturri took the lead on the airframe. Critically, ex-Leonardo helicopter certification experts remain on Vertical's leadership team — rotary-wing certification know-how is fully internalised.

5.2 Two-edged sword

Speed + lower certification risk

Minimal upfront investment, certified-partner technology lowers certification risk, fast production ramp-up. Aciturri and Honeywell already have mass-production capability, so Vertical can reach 200+ aircraft per year far faster than building its own plant.

Margin sharing + lower control

Profit-sharing reduces unit economics, supply-chain control weakens, partner priority shifts can delay schedules. To giants like Honeywell or GKN, Vertical is a relatively small customer — it risks being deprioritised during global supply shocks. Vertical manages this with risk-sharing partnership contracts to align incentives.

6. Financial health and funding scenarios — crossing the Valley of Death

6.1 Cash flow and runway

Official fact: Cash and cash equivalents as of 4 November 2025 were approximately £89M (≈ US$117M). Vertical states current cash takes it to mid-2026. 2025 net operating cash outflow is expected at US$110M–125M. Over the next 12 months (Q4 2025 — Q3 2026), Vertical anticipates burning approximately £175M (≈ US$235M).

Interpretation: That burn is materially below peers — Joby burns ~US$150M/quarter, Archer ~US$120M/quarter — empirical proof that Vertical's capital-efficient OEM model is real. The problem is not the rate of burn but the absolute level of cash. Mid-2026 runway is nowhere near the 2028 certification target.

6.2 The Valley of Death

Vertical estimates roughly US$700M (≈ KRW 950B) additional funding to reach type certification in 2028. Net of current cash (US$117M), that leaves a financing gap of over US$600M — larger than the company's current market capitalisation (~US$500M). Pure equity raises would imply extreme shareholder dilution. Post-Lilium investor sentiment makes large rounds harder still.

2025 Mudrick Capital round

January 2025: US$90M raised led by Mudrick Capital. July 2025: additional US$69M. Bought time but not a long-term solution — Mudrick's tranche is debt-heavy (convertibles) and may weigh on the balance sheet.

Strategic investment

Additional capital from Honeywell, Aciturri, or American Airlines. They are already deeply involved — strong sunk-cost incentive to support Vertical.

Pre-delivery payments

Early PDPs from confirmed orders. Only viable once certification is close and delivery dates are firmed up.

Government support

UK Aerospace Technology Institute (ATI) grants and similar public funding. The UK government has been actively supporting aerospace post-Brexit.

ATM programme

The recently signed Jefferies ATM (At-The-Market) programme allows Vertical to sell shares opportunistically into market strength.

Conclusion: Vertical must successfully close a large funding round in H1 2026. Miss that window — or close too small — and serious Going Concern doubts emerge.

7. Risk factors and investment view

7.1 Core risks

Certification risk

EASA / CAA SC-VTOL is stricter than the FAA. Proving 10⁻⁹ safety is theoretically clean but unexpected technical hurdles in actual demonstration could push certification beyond 2029 — directly translating into cash exhaustion.

Partner dependency

Over-reliance on giants like Honeywell and Aciturri. Strategy shifts or price hikes from them — given Vertical's weaker bargaining position — could erode margins.

Sector contagion

Lilium's collapse has chilled European eVTOL sentiment. No matter how loudly Vertical says "we're different," the market will demand a higher risk premium for European challengers.

7.2 Bull / Base / Bear scenarios

Bull Case

- Successful 2025 transition flight → successful large H1 2026 funding round → 2028 type certification.

- OEM model's natural operating leverage drives a multi-bagger from depressed levels.

- 40%+ battery-replacement gross margins materialise → US$100M+ operating cash flow post-2030.

- Hybrid VX4 wins dual-use civilian + defence adoption, expanding TAM.

Base Case

- Transition flight succeeds; funding occurs piecemeal and dilutively; certification slips 6–12 months.

- EVTL trades as a "survival-option asset" — highly volatile until the 2028–2029 certification event.

- Market debates how to price the OEM margin squeeze against the locked-in battery model.

Bear Case

- H1 2026 funding fails or is too small → Going Concern warning emerges.

- EASA SC-VTOL technical hurdles push certification beyond 2029 → cash exhaustion.

- Lilium-style liquidity crisis; share price collapses to deep optionality.

7.3 Investment conclusion — High Risk / High Reward archetype

Vertical Aerospace is the textbook "if they survive, they thrive" optionality asset. If Joby and Archer are "safer large caps" of the sector, Vertical is the volatile growth name. Investors should monitor the 2025 piloted transition flight result and H1 2026 funding announcements as the two decisive triggers — and size the position small within the portfolio.

8. Conclusion

Vertical Aerospace is applying the basic management principle of "focus" to the eVTOL industry. Unlike competitors trying to do everything, Vertical concentrates on what it does best — design, technical integration, and batteries — and outsources the rest. That strategy succeeded in suppressing early capital consumption. Now Vertical must move into the execution phase, controlling its partners and delivering a finished product.

By 2030, when flying taxis become daily reality, whether the VX4 sits at the centre of it — or in a museum — depends on Vertical's execution over the next 18 months.

Sources

- Lilium Closes eVTOL Business As New Investment Falls Through — AIN: https://www.ainonline.com/aviation-news/futureflight/2025-02-21/lilium-closes-evtol-business-new-investment-falls-through

- Germany's Lilium files for final insolvency — ch-aviation: https://www.ch-aviation.com/news/150719-germanys-lilium-files-for-final-insolvency

- Cash Burn vs. Cautious Capital — MarketBeat: https://www.marketbeat.com/stock-ideas/cash-burn-vs-cautious-capital-which-evtol-strategy-will-win/

- Five Nations Unite to Streamline eVTOL Certification: https://businessaviation.aero/evtol-news-and-electric-aircraft-news/low-altitude-economy/five-nations-unite-to-streamline-evtol-certification

- Top Five eVTOL Stocks to watch for 2025 — Joby, Archer & More: https://businessaviation.aero/evtol-news-and-electric-aircraft-news/advanced-air-mobility/top-five-evtol-stocks-to-watch-for-2025-joby-aviation-archer-more-stock-analysis

- Vertical Aerospace Permit to Fly Approval (PDF): https://vertical-aerospace.com/wp-content/uploads/2025/11/Vertical-Aerospace-Begins-Piloted-Transition-Testing-Following-Permit-to-Fly-Approval.pdf

- Vertical Aerospace Ramps Up Full-Scale Prototype Progress (10 flights): https://evtolinsights.com/vertical-aerospace-ramps-up-progress-flying-its-full-scale-prototype-with-10-flights-now-already-completed/

- Vertical Aerospace × Aciturri long-term airframe partnership: https://verticalmag.com/press-releases/vertical-aerospace-and-aciturri-aerostructures-announce-long-term-airframe-partnership-for-the-vx4/

- Vertical Aerospace Presents Its Blueprint for Sector Leadership — Nasdaq: https://www.nasdaq.com/articles/vertical-aerospace-presents-its-blueprint-sector-leadership

- Vertical Aerospace H1 2025 Results Call Transcript (PDF): https://s203.q4cdn.com/131781877/files/doc_financials/2025/q2/Vertical-Aerospace-H1-Results-Call-Transcript-87.pdf

- Vertical Aerospace Q1 2025 Earnings Call Transcript — Seeking Alpha: https://seekingalpha.com/article/4786254-vertical-aerospace-ltd-evtl-q1-2025-earnings-call-transcript

- Aciturri × Vertical airframe partnership announcement: https://www.aciturri.com/en/press-media/news/vertical-aerospace-and-aciturri-aerostructures-announce-long-term-airframe-partnership-for-the-vx4

- Vertical Aerospace Q1 2025 Operating Update (PDF): https://vertical-aerospace.com/wp-content/uploads/2025/05/Vertical-Aerospace-Provides-First-Quarter-2025-Operating-Update-Demonstrating-Momentum-Towards-Certification-and-Commercialisation.pdf

- Vertical Aerospace Q3 2025 Update (PDF): https://vertical-aerospace.com/wp-content/uploads/2025/11/Vertical-Aerospace-Provides-Third-Quarter-Update-Demonstrating-Momentum-on-Transition-Flight-Testing-Business-Plan-Updates-and-Best-in-Class-Aircraft.pdf

- Vertical × GKN Aerospace partnership — JEC Composites: https://www.jeccomposites.com/news/spotted-by-jec/vertical-aerospace-announces-partnership-with-gkn-aerospace/

- Vertical Aerospace H1 2025 Operating Update (PDF): https://vertical-aerospace.com/wp-content/uploads/2025/08/J1666.005-Vertical_PR-update_5-Aug-25.pdf

- Vertical Aerospace Closes Upsized $90M Public Offering (PDF): https://vertical-aerospace.com/wp-content/uploads/2025/01/Vertical-Aerospace-Announces-Closing-Of-Upsized-90M-Underwritten-Public-Offering.pdf

- Vertical Aerospace Prices $90M Offering — Nasdaq: https://www.nasdaq.com/articles/vertical-aerospace-prices-90-mln-offering-6-unit

- Vertical Aerospace Q3 2025 Financials (PDF): https://s203.q4cdn.com/131781877/files/doc_financials/2025/q3/3e1a2a5b-0aa3-4306-be21-793e69725084.pdf

- Original source (Naver Blog): https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224117284824