DEEP RESEARCH · NIKE

Nike: Strategic Rebuild and Valuation Reassessment at a Structural Turning Point

A turnaround check on FY2026 Q2 results, the Win Now strategy, China risk, and tariff pressure

0. Bottom line first

Nike is not yet in a full recovery, but it is in the middle of a structural reset: reducing oversupplied classics and returning to running and performance innovation. The key question is how quickly recovery in North American wholesale and running can offset China weakness, tariffs, and margin damage.

Official fact: The source cites FY2026 Q2 revenue of USD 12.427 billion, up 1% YoY, and EPS of USD 0.53, down 32% YoY. It also says Nike plans to reduce classic franchise supply by more than USD 4 billion from peak levels by FY26 year-end; in the quarter, that category fell more than 20% and created about USD 550 million of revenue headwind.

Interpretation: The near-term numbers show margin pain first, but part of the revenue sacrifice is intentional: restoring scarcity and freeing shelf space for innovation. I view this as a transition between bottom confirmation and proof of upside momentum.

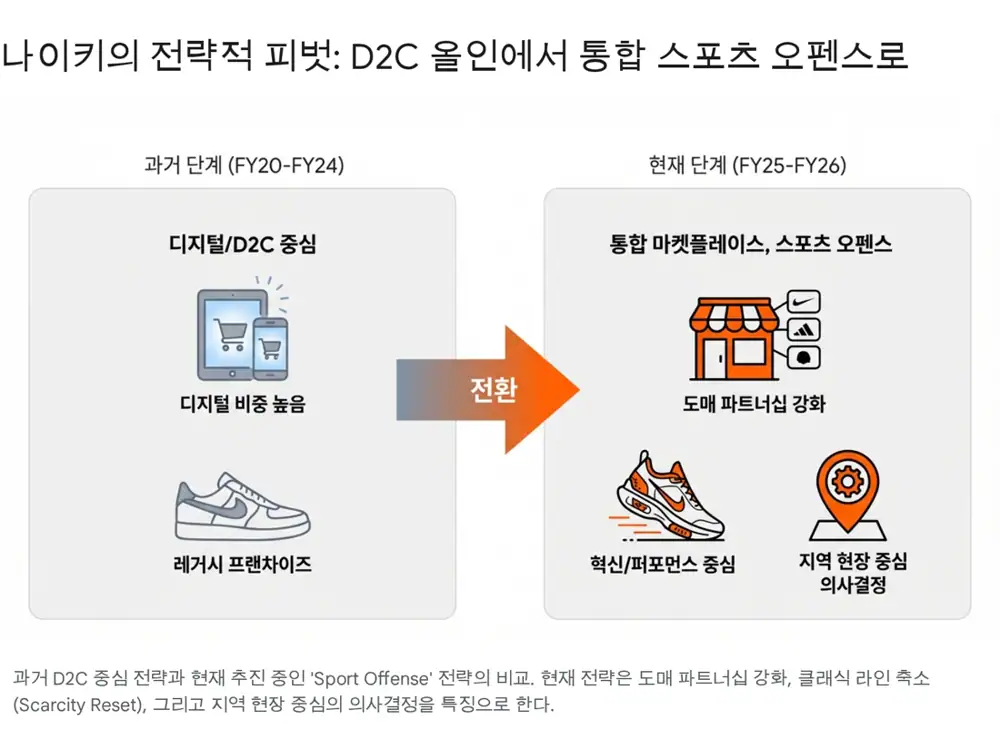

1. Strategic pivot: Win Now and Sport Offense

Nike's current strategy is concentrated in CEO Elliott Hill's Win Now action plan. It addresses cultural stagnation, delayed product innovation, weaker storytelling, and marketplace inefficiency. The core is to reduce dependence on classic franchises such as Air Force 1, Air Jordan 1, and Dunk, and to put performance innovation back at the center.

Official fact: The source describes Sport Offense as an operating model in which geography GMs report directly to the CEO while Nike strengthens city-by-city, partner-by-partner, and sport-by-sport execution. It also presents the appointment of Venkatesh Alagirisamy as COO as a step toward end-to-end integration of technology, supply chain, and sales processes.

Interpretation: A centrally driven digital-first D2C push alone could not handle rapid local trend shifts and wholesale partner repair. The new operating model is an attempt to improve reaction speed in markets such as China and North America.

2. Competitive edge: a damaged moat and running's counterattack

Nike's traditional moat was brand equity, cost advantages from scale, and marketing with the world's leading athletes. The source argues that recent innovation stagnation and dependence on classics eroded part of that moat, especially as Hoka and On Running gained share in performance running shoes.

Two straight quarters of 20%+ growth

Products such as Structure 26 and Vomero 18 are presented as evidence that the performance-return strategy is working.

Revenue down 30%

Among Nike, Jordan, and Converse, Converse is described as the weak point.

Hoka growth slowing

The source notes signs that Hoka growth has slowed from the 25% range to the low teens.

3. Operating variables: Q, P, and C

| Variable | Source takeaway | Investment read |

|---|---|---|

| Q: volume | Classic reductions create near-term revenue headwind, while running and North American wholesale provide support. | Separate intentional reset from genuine demand weakness. |

| P: price | Scarcity recovery and higher innovation mix are essential for price defense. | Reduced discount dependence is needed for brand repair. |

| C: cost | Tariffs and regional mix pressure margins. | Without margin recovery, valuation rerating is limited. |

The source views strong recovery in North American wholesale and double-digit running growth as positive signals. China weakness and structural tariff costs are the negative signals because Nike cannot solve them quickly by internal execution alone.

4. Risks and checkpoints

- China: Weak consumption and rising local brands such as Anta and Li-Ning could damage a high-margin growth pillar.

- Tariffs: The source mentions a possible 320bp margin hit from tariffs. Stronger protectionism could pressure both FY26 and FY27.

- Innovation products: If Aero-FIT, Nike Mind, and other new platforms fail to resonate, Sport Offense loses force.

- Valuation: The source does not view Nike as deep value now, but sees meaningful recovery potential if China stabilizes and margins improve.

5. Overall view

Nike is playing defense by lowering inventory and pulling oversupplied classics from the market, while playing offense through wholesale repair and innovation launches. My conclusion is cautious monitoring. The buying argument is not simply that the stock looks cheap; it emerges when the innovation cycle demonstrably drives gross-margin recovery.

Sources

- Original blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116861024

- NIKE-Inc-Q2FY26-OFFICIAL-Transcript_-FINAL.pdf

- The Great Swoosh Reset: https://markets.financialcontent.com/wral/article/predictstreet-2025-12-18-the-great-swoosh-reset-a-deep-dive-into-nikes-nke-2025-turnaround-strategy

- HOKA vs Nike Running Shoes Compared: https://www.marathonsports.com/blog/hoka-vs-nike-running-shoes-compared

- Nike Aero-FIT: https://about.nike.com/en/newsroom/releases/nike-aero-fit-official-images

- Nike Mind: https://about.nike.com/en/newsroom/releases/nike-mind-001-mind-002-official-images

- Global Activewear Market Size & Outlook: https://www.grandviewresearch.com/horizon/outlook/activewear-market-size/global

- Nike China conundrum AMP: https://m.economictimes.com/news/international/business/nike-shoes-china-conundrum-deepens-as-turnaround-stagnates/amp_articleshow/126069206.cms

- Nike China conundrum: https://m.economictimes.com/news/international/business/nike-shoes-china-conundrum-deepens-as-turnaround-stagnates/articleshow/126069206.cms

- Sahm Capital Nike value article: https://www.sahmcapital.com/news/content/is-nike-stock-around-67-offering-value-after-recent-rebound-in-2025-2025-12-13

- Morningstar Nike Earnings: https://www.morningstar.com/stocks/nike-earnings-china-weakness-tariffs-overshadow-progress

- Investing.com BofA target: https://www.investing.com/news/analyst-ratings/nike-price-target-lowered-to-73-from-84-at-bofa-on-china-concerns-93CH-4416727

- Investing.com Truist target: https://www.investing.com/news/analyst-ratings/truist-securities-lowers-nike-stock-price-target-to-70-on-china-headwinds-93CH-4417601