DEEP RESEARCH · TTD/ADTECH

The Trade Desk: Open-Internet Moat Under Competitive Pressure

A combined view of Kokai, UID2, OpenPath, CTV, retail media, and governance risk

0. Bottom line first

TTD has the advantage of being core infrastructure for open-internet advertising, but it also faces real pressure from Amazon DSP, AppLovin, and agency conflict. The 2025 share-price correction removes some excess, but it also shifts the story into a prove-it phase for technology moat and customer relationships.

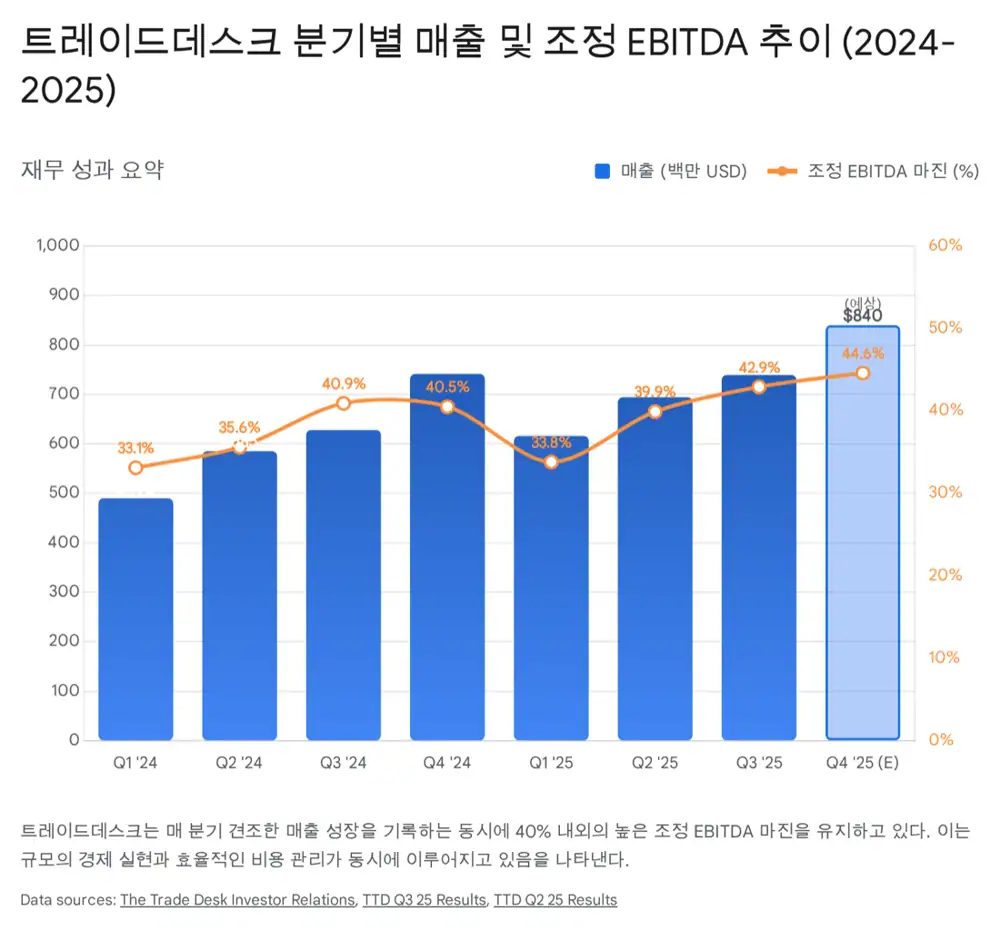

Official fact: The source cites 3Q25 revenue of USD 739 million, up 18% YoY; 22% organic growth excluding political advertising; adjusted EBITDA of USD 317 million; adjusted EBITDA margin of about 43%; GAAP net income of USD 116 million; and EPS of USD 0.23.

Interpretation: On the numbers, TTD remains a high-growth, high-margin platform. But the market now treats it less as dream adtech and more as a mature growth company that must prove itself against Amazon, AppLovin, and cash-flow expectations.

1. Financial performance: growth with profitability

| Metric | 3Q25 | Interpretation |

|---|---|---|

| Revenue | USD 739M | +18% YoY |

| Growth ex-political ads | +22% | Structural growth even excluding event revenue |

| Adjusted EBITDA | USD 317M | About 43% of revenue |

| GAAP net income | USD 116M | Profitable trend intact |

| EPS | USD 0.23 | Profitability remains visible after SBC |

| 4Q25 guidance | At least USD 840M revenue and about USD 375M adjusted EBITDA | Holiday season, CTV, and retail media momentum |

The source sees revenue moving from USD 2.445 billion in 2024 to roughly USD 2.9 billion in 2025. It also cites more than USD 1.5 billion of cash and equivalents at the end of 3Q25, and frames TTD’s debt-free balance sheet as financial flexibility versus peers such as AppLovin and Magnite.

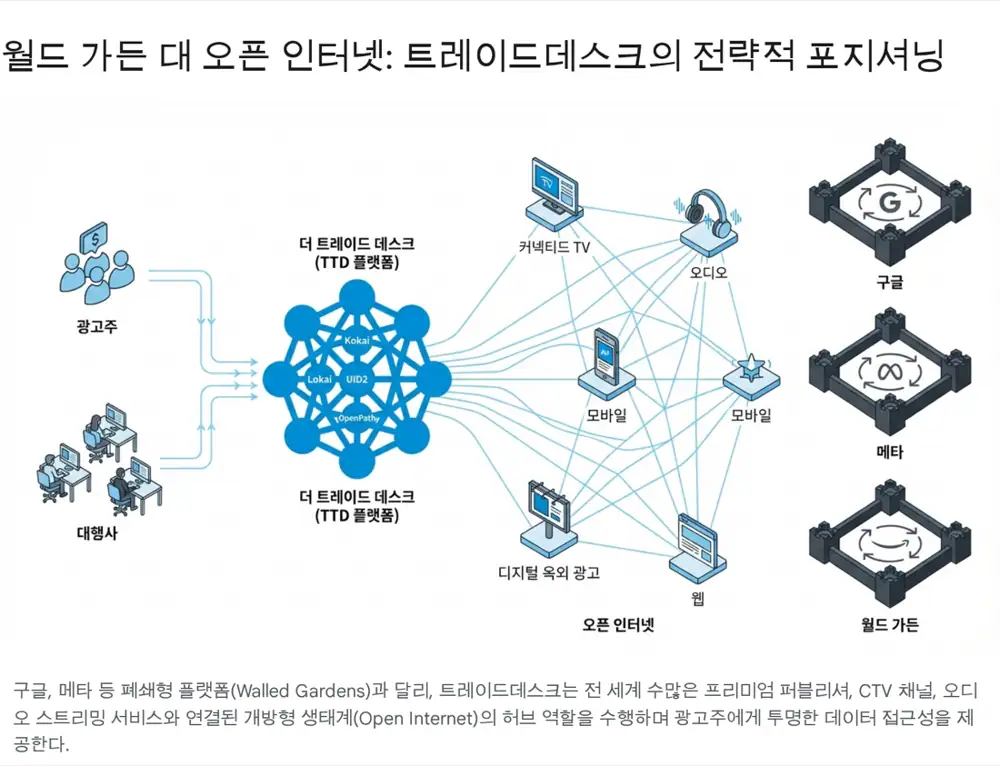

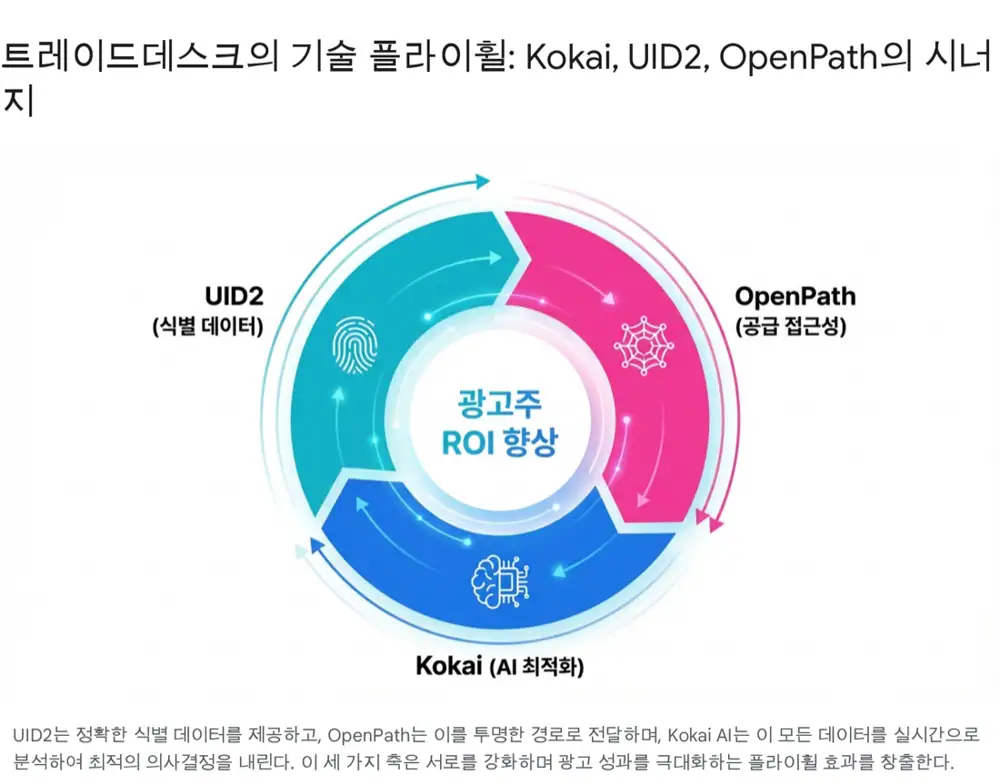

2. Technology moat: Kokai, UID2, OpenPath

Distributed AI

It analyzes more than 13 million ad impressions per second to calculate bids. The source cites average 5x ROAS for North American advertisers using Kokai.

ID for the privacy era

Built on encrypted login data such as email, it has been adopted by Disney, Paramount, NBCUniversal, Walmart, AWS, and others.

Direct supply chain

It connects directly to publishers and bypasses or minimizes SSPs. Vizio and Hearst are cited as seeing fill-rate gains and more than 23% revenue growth.

Interpretation: Kokai optimizes performance, UID2 sets an identity standard, and OpenPath reduces supply-chain cost. But OpenPath touches agency and reseller margins, creating commercial friction even if the technology logic is sound.

3. Growth verticals: CTV and retail media

The source treats CTV and retail media as TTD’s long-term growth engines. As TV viewing shifts to streaming and retailer purchase data connects with ad measurement, advertisers want to link brand exposure to actual purchase conversion.

4. Competition and customer-relationship risk

The most direct threat

Prime Video ads and purchase data target CTV and retail-media budgets. The source also says Amazon has proposed head-to-head tests against TTD.

AI performance competition

AXON 2.0 and expansion from mobile gaming into e-commerce have raised doubts about TTD’s technology moat.

OpenPath friction

Some media buyers and agencies see OpenPath as reducing their role and margins, leading to budget shifts or pauses.

5. Governance, political ads, and valuation

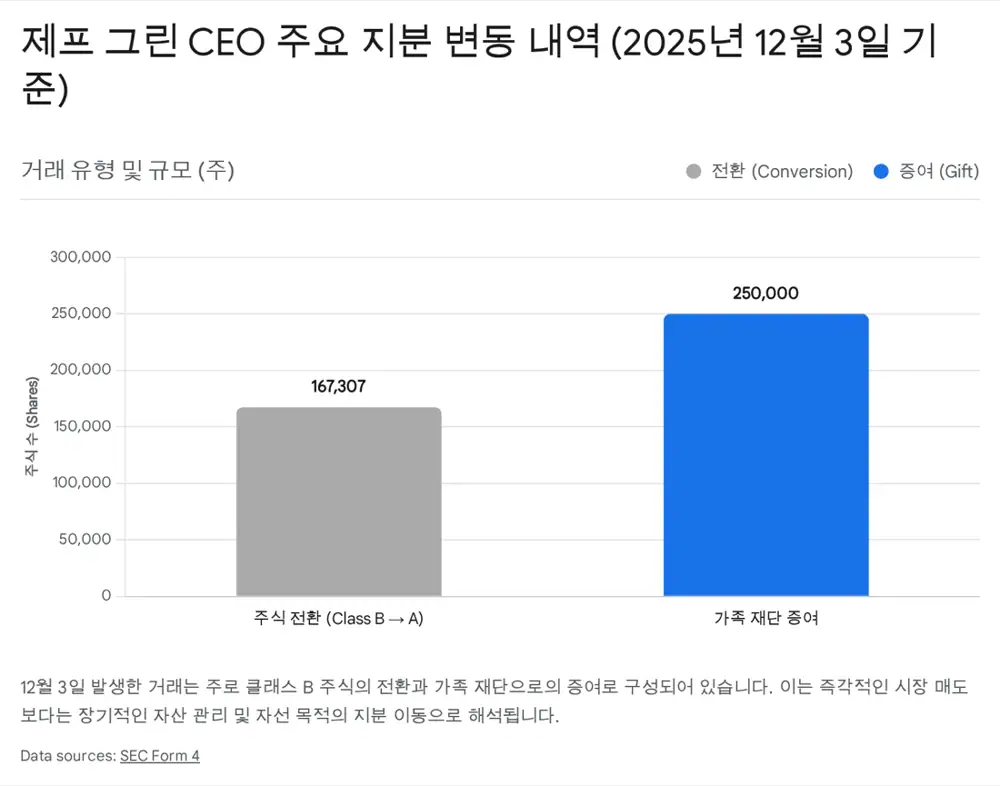

Official fact: The source says TTD received a Nasdaq Rule 5640 reprimand letter on December 9, 2025, related to a charter amendment extending the conversion timing of Class B shares, with no impact on listing status. It also cites CEO Jeff Green’s large February 2025 sale and December 2025 conversion, gift, and disposition activity as sentiment negatives.

The 2026 U.S. midterms are the positive counterweight. Citing AdImpact, the source expects 2026 political ad spending to reach a record USD 10.8 billion, with CTV accounting for more than USD 2.5 billion. TTD has an advantage in precisely targeted programmatic political advertising.

| Item | Source detail | View |

|---|---|---|

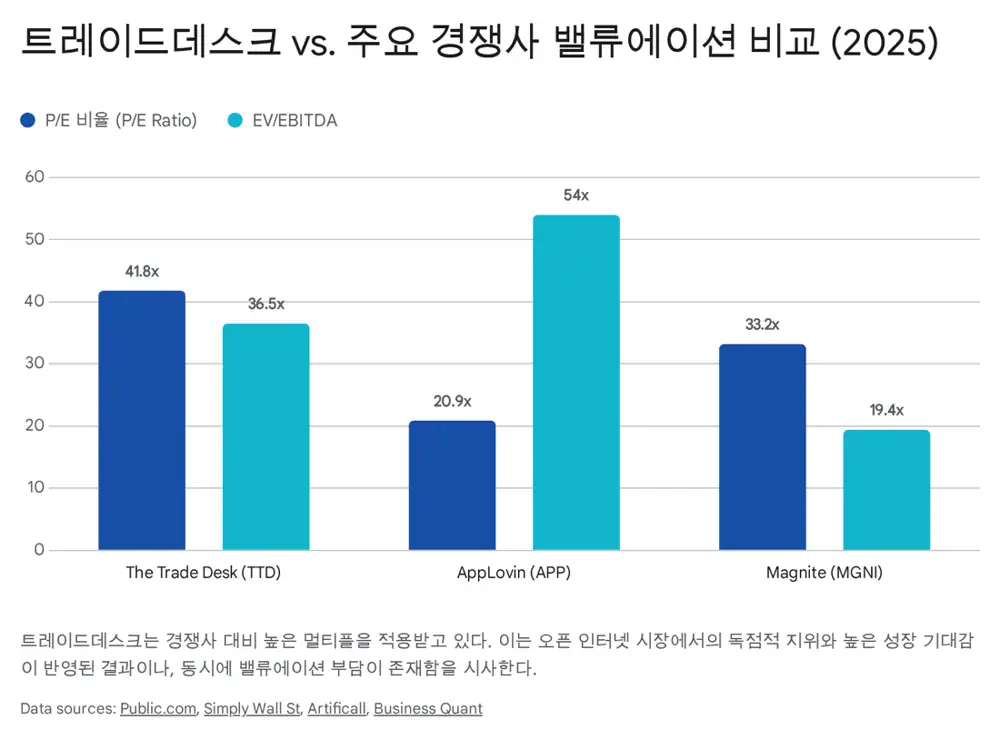

| Forward P/E | From above 100x at end-2024 to about 41x in December 2025 | De-rating underway |

| Industry average | About 34x | Still at a premium |

| Investment stance | Cautious buy | Need to confirm 2026 election momentum and Kokai stabilization |

| Risks | Amazon DSP share, agency churn, growth settling in the mid-teens | Additional multiple compression possible |

6. My conclusion

TTD is not a flawless monopoly platform, but it remains a core asset for absorbing structural growth in open-internet ad budgets. What it needs now is not a better story but proof in Kokai outcomes, UID2 adoption, reduced OpenPath conflict, and expanding CTV/retail-media budgets. A staged approach can make sense, but Amazon DSP and agency reaction need to be checked every quarter.

Sources

- Original post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116797215

- Reference 1: https://public.com/stocks/ttd/pe-ratio

- Reference 2: https://www.prnewswire.com/news-releases/assembly-election-outlook-report-2026-midterms-projected-to-be-the-most-expensive-in-history-302574063.html

- Reference 3: https://digiday.com/media-buying/wpp-estimates-commerce-media-spending-to-overtake-tv-this-year/

- Reference 4: https://investors.thetradedesk.com/news-and-events/news/news-details/2025/The-Trade-Desk-Reports-Third-Quarter-2025-Financial-Results/

- Reference 5: https://seekingalpha.com/symbol/TTD/earnings/revisions

- Reference 6: https://simplywall.st/stocks/us/media/nasdaq-ttd/trade-desk/news/is-trade-desk-a-bargain-after-its-69-2025-share-price-slide

- Reference 7: https://www.thetradedesk.com/resources/how-kokai-ai-drives-roas-advertisers

- Reference 8: https://support.google.com/google-ads/answer/14762010?hl=en

- Reference 9: https://www.cookieyes.com/blog/google-cookie-deprecation/

- Reference 10: https://www.thetradedesk.com/unified-id-solution-2-0

- Reference 11: https://www.zacks.com/stock/news/2805672/can-the-trade-desks-openpath-transform-the-digital-ad-supply-chain

- Reference 12: https://www.thecurrent.com/data-privacy-supply-path-spo-advertisers-openpath-publishers-2025

- Reference 13: https://digiday.com/media-buying/media-buyers-shift-spend-from-the-trade-desks-openpath-over-transparency-concerns/

- Reference 14: https://www.thecurrent.com/streaming-fuel-record-us-political-spending-2026-ctv

- Reference 15: https://www.marketingdive.com/news/inside-walmart-connect-as-retail-media-ctv-convergence-accelerates/807682/

- Reference 16: https://www.thecurrent.com/opinion-john-tegner-the-trade-desk-search-trial-google-antitrust

- Reference 17: https://www.fool.com/investing/2025/03/22/better-ad-tech-stock-applovin-vs-the-trade-desk/

- Reference 18: https://artificall.com/analysis/companies/comparisons/applovin-vs-the-trade-desk/

- Reference 19: https://simplywall.st/stocks/us/media/nasdaq-mgni/magnite/valuation