DEEP RESEARCH · ECHOSTAR

EchoStar: Revalued as a SpaceX Proxy After the Spectrum Sales

How AWS-4, H-Block, and AWS-3 transactions reshape SpaceX ownership and SOTP value

0. Bottom line first

EchoStar has effectively become a public-market SpaceX proxy by converting underused spectrum into SpaceX Class A common stock. The source's key estimates are about USD 11.1 billion of equity value, roughly 52.4 million shares, about 2.6-2.8% ownership of SpaceX, and a central estimate of 2.75%.

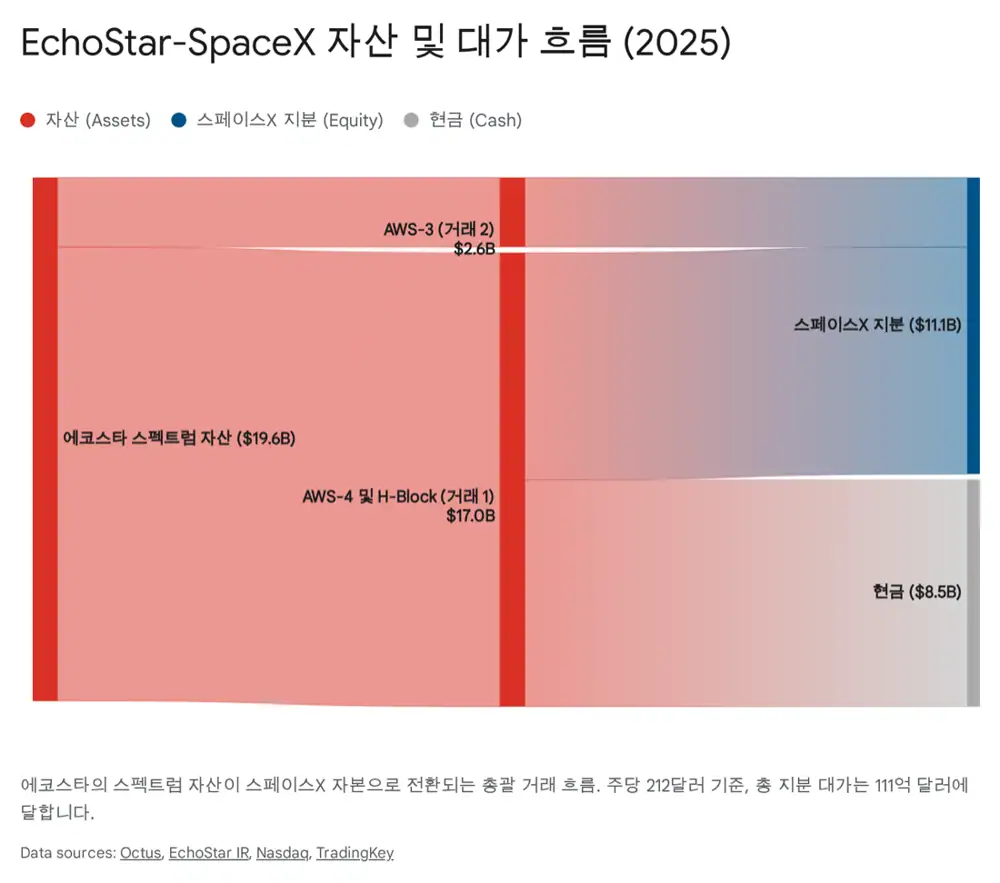

Official fact: The source says EchoStar converted spectrum assets into SpaceX equity through two definitive agreements in the second half of 2025. The first AWS-4/H-Block transaction is about USD 17 billion, consisting of up to USD 8.5 billion in cash and up to USD 8.5 billion in SpaceX stock. The second AWS-3 transaction is presented as an all-stock exchange worth about USD 2.6 billion.

Interpretation: This is not just an asset sale. It changes EchoStar's thesis from satellite TV and capital-intensive network buildout toward equity exposure to SpaceX's Direct-to-Cell network. The catch is that the shares are private and hard to monetize before a liquidity event.

1. Transaction structure: two spectrum tranches

The first transaction is the sale of AWS-4 and H-Block spectrum licenses. The source describes these bands as critical for integrating terrestrial and satellite networks and enabling mobile-device connectivity. The headline value is about USD 17 billion, and the stock component is fixed at USD 212 per share.

The second transaction is the November 2025 AWS-3 amendment. It sells unpaired AWS-3 spectrum, the 1695-1710 MHz uplink band, which the source views as essential uplink capacity for Direct-to-Cell service quality.

| Tranche | Asset | Value | Consideration | Meaning |

|---|---|---|---|---|

| First | AWS-4, H-Block | About USD 17B | Up to USD 8.5B cash + up to USD 8.5B SpaceX stock | EchoStar liquidity repair and SpaceX D2C moat expansion |

| Second | Unpaired AWS-3 1695-1710 MHz | About USD 2.6B | All SpaceX stock | Uplink reinforcement and larger EchoStar equity exposure |

| Ancillary | Debt interest support | About USD 2B | Cash interest support through November 2027 | Leverage relief |

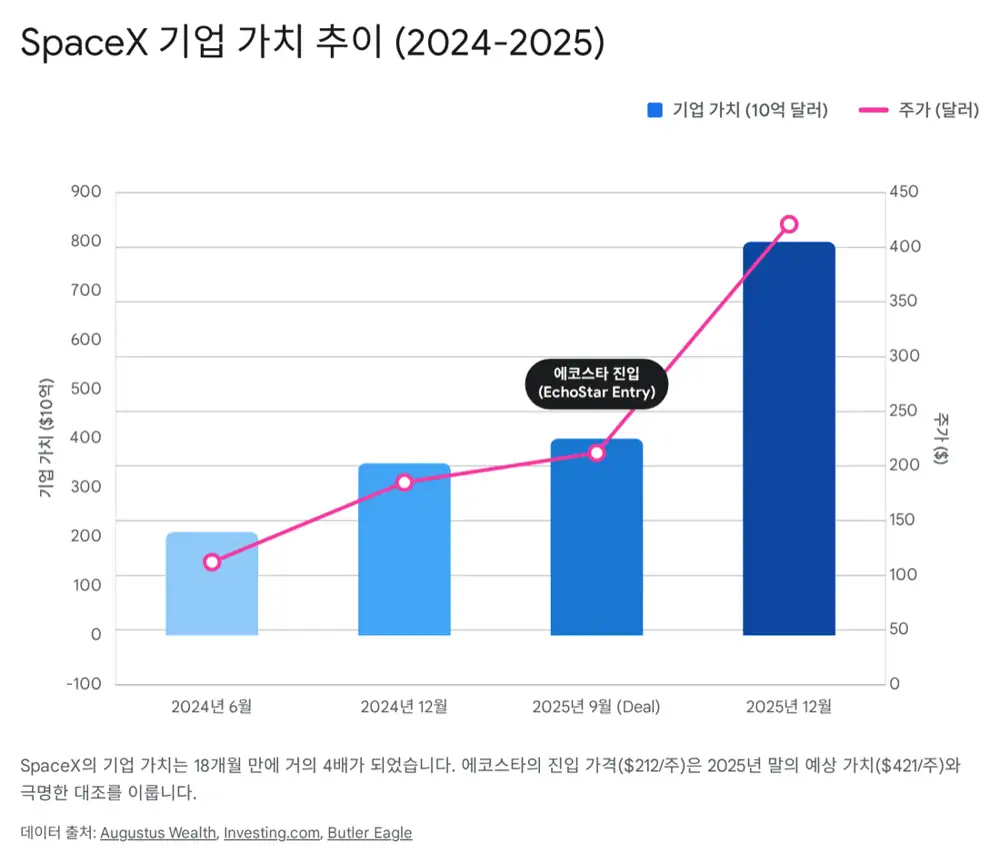

2. Ownership math: USD 212 reference price and USD 421 revaluation

Official fact: The source uses a USD 212 per-share reference price and estimates about USD 11.1 billion of equity value. That implies about 52.4 million shares and, based on a reverse calculation of fully diluted SpaceX shares, about 2.6-2.8% ownership with a central estimate of 2.75%.

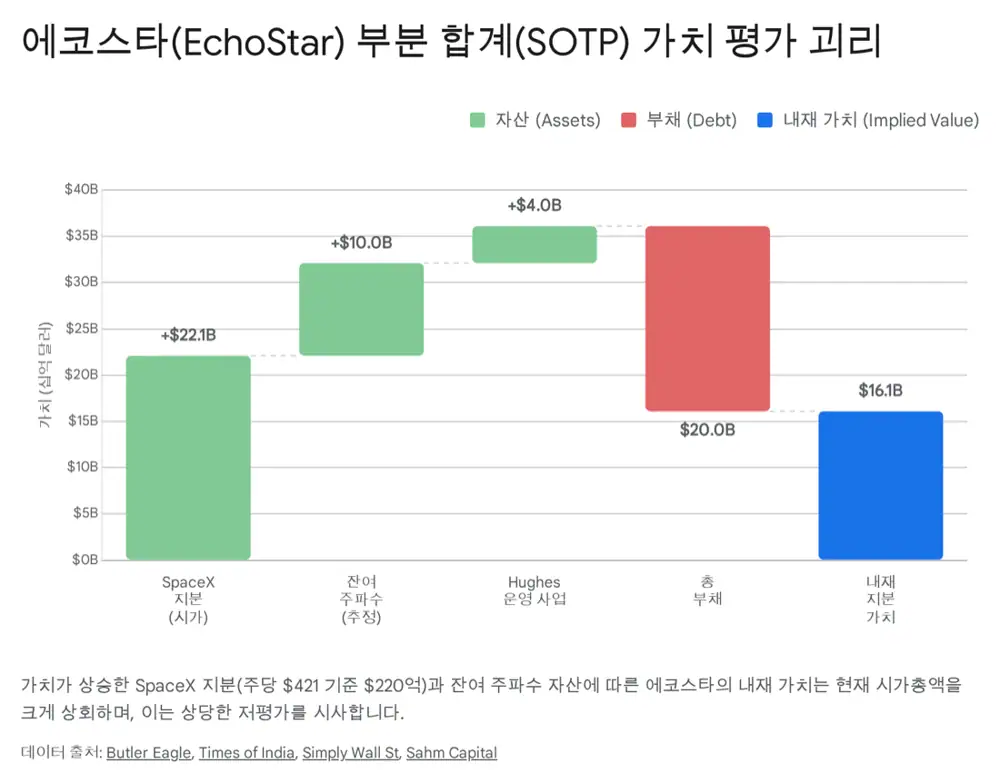

Interpretation: If the USD 421 per-share valuation mentioned for the December 2025 secondary tender is applied to the same share count, the mark-to-market value nearly doubles versus the nominal transaction basis. This creates the SOTP gap between EchoStar's public value and its embedded SpaceX stake.

USD 212/share

The transaction price used to estimate USD 11.1B of equity and about 52.4M shares.

USD 421/share

The December 2025 valuation referenced by the source, creating unrealized gain potential.

About 2.75%

The central estimate after reverse-calculating SpaceX's fully diluted share count.

3. Why stock instead of cash

The source views it as unusual that a leveraged company like EchoStar chose to receive much of the USD 11.1 billion in stock rather than cash. It signals Charlie Ergen's strategic conviction in future connectivity and SpaceX's Direct-to-Cell dominance.

The transferred AWS-4 at 2000-2020 MHz, H-Block at 1915-1920/1995-2000 MHz, and AWS-3 at 1695-1710 MHz provide mid-band characteristics suited to satellite-to-smartphone communication. The source frames this combination as the technical key to both downlink and uplink capacity for voice and data.

4. Risks: private shares, IPO timing, and control

- Illiquidity: SpaceX shares do not trade publicly. EchoStar cannot simply sell USD 11 billion of stock at will.

- IPO timeline: The source cites reports that SpaceX may prepare a potential listing in 2026 or 2027. Value realization depends heavily on such a liquidity event.

- Bull case: If SpaceX IPOs above an USD 800 billion valuation, the source says EchoStar's liquid stake value could exceed USD 22 billion.

- Bear case: Regulatory delay, market volatility, or Starship failure could leave EchoStar asset-rich but cash-poor as debt maturities approach.

- Voting power: The received shares are Class A common stock. Economic exposure is meaningful, but strategic control is likely limited under a dual-class structure dominated by Musk and insiders.

5. Overall view

As the source concludes, the number that changed everything is about 2.75%. EchoStar can no longer be explained only by declining satellite-TV economics; it now carries a space-economy proxy profile through its SpaceX stake. Still, the thesis must be evaluated together with SpaceX valuation, IPO probability, private-share discount, EchoStar's remaining debt, and cash flow. In 2026, the most important metric may be SpaceX's S-1 and listing price rather than legacy subscriber trends.

Sources

- 원문 블로그: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116745208

- 이전 에코스타 글: https://m.blog.naver.com/star_of_self/224116728104

- EchoStar spectrum sale and SpaceX commercial agreement: https://ir.echostar.com/news-releases/news-release-details/echostar-announces-spectrum-sale-and-commercial-agreement-spacex

- Simply Wall St SATS stake article: https://simplywall.st/stocks/us/media/nasdaq-sats/echostar/news/echostar-sats-is-up-111-after-spacex-ipo-buzz-highlights-its

- TradingKey SpaceX IPO article: https://www.tradingkey.com/analysis/stocks/us-stocks/251415133-elon-musk-spacex-ipo-tradingkey

- moomoo Community SATS post: https://www.moomoo.com/community/feed/echostar-sats-us-rather-than-pursue-a-conventional-initial-public-115744007061510

- Reddit EchoStar sells more spectrum: https://www.reddit.com/r/spacex/comments/1oqz311/echostar_sells_more_spectrum_in_26_billion_deal/

- Times of India SpaceX valuation memo: https://timesofindia.indiatimes.com/technology/tech-news/elon-musks-spacex-may-be-on-its-way-to-become-worlds-most-valuable-private-company-memo-say-ipo-at-funding-an-insane-flight-rate-for/articleshow/125975136.cms

- Butler Eagle SpaceX valuation: https://www.butlereagle.com/20251215/spacex-sets-800-billion-valuation-confirms-2026-ipo-plans/

- Octus EchoStar FCC inquiries: https://octus.com/resources/articles/echostar-expects-to-resolve-fcc-inquiries-with-19b-s-band-spectrum-sale-to-spacex/

- Space Intel Report AWS-4/H-Block deal: https://www.spaceintelreport.com/echostar-to-sell-aws-4-h-bloc-spectrum-licenses-to-spacex-in-17b-deal-that-includes-spacex-stock-at-212-share/

- Nasdaq AWS-3 deal: https://www.nasdaq.com/articles/echostar-sell-unpaired-aws-3-licenses-approx-26-bln-spacex-stock

- Seeking Alpha USD 2.6B spectrum: https://seekingalpha.com/news/4517107-spacex-to-pay-echostar-26b-for-more-spectrum-licenses

- EchoStar AWS-3 release: https://ir.echostar.com/news-releases/news-release-details/echostar-agrees-sell-full-unpaired-aws-3-spectrum-license

- Augustus Wealth SpaceX valuation: https://augustuswealth.com/blog/what-know-about-space-x-valuation/

- Reddit SpaceX USD 350B valuation: https://www.reddit.com/r/spacex/comments/1hcqqgj/spacex_hits_350bn_stock_market_valuation/

- Investing.com USD 400B valuation: https://www.investing.com/news/company-news/spacex-reportedly-planning-insider-share-sale-at-400-billion-valuation-4136481

- Reddit SpaceX USD 400B valuation: https://www.reddit.com/r/SpaceXLounge/comments/1lvriic/spacex_heads_to_400bn_valuation_in_share_sale/

- Reddit SpaceX USD 800B valuation: https://www.reddit.com/r/SpaceXLounge/comments/1pl85zr/spacex_officially_sets_valuation_to_800b_share/

- Investing.com EchoStar stock soars: https://www.investing.com/news/stock-market-news/echostar-stock-soars-after-spacex-valuation-set-to-double-93CH-4394081

- Times of India IPO possible: https://timesofindia.indiatimes.com/business/international-business/biggest-ipo-ever-insider-share-sale-sets-spacex-valuation-at-800-billion-2026-market-debut-possible/articleshow/125950372.cms

- Light Reading landscape analysis: https://www.lightreading.com/satellite/how-the-echostar-spacex-deal-reshapes-the-u-s-wireless-and-satellite-landscape

- CNET wireless gold article: https://www.cnet.com/tech/mobile/spacex-strikes-wireless-gold-with-echostar-sale-expect-better-coverage-with-these-carriers/

- Mobile World Live deal analysis: https://www.mobileworldlive.com/dish-network/analysis-echostar-spacex-deal-resets-satellite-mobile-sectors/

- Seeking Alpha latest valuation: https://seekingalpha.com/news/4529058-spacexs-latest-valuation-makes-it-the-worlds-most-valuable-private-company