DEEP RESEARCH · ECHOSTAR/SATS

EchoStar (SATS): Spectrum Monetization and the Asset-Light Pivot

A special-situation review of the AT&T/SpaceX transactions, Jupiter 3, S-Band D2D, and the potential $41.65B liquidity reversal.

0. Bottom line first

Investing in EchoStar is less a conventional telco investment and more a special-situation bet on whether spectrum monetization closes. Based on the source, completion of the $22.65B AT&T deal and the $19B SpaceX deal would create about $41.65B of liquidity. After repaying about $21.8B of long-term debt, roughly $20B of cash and stock could remain.

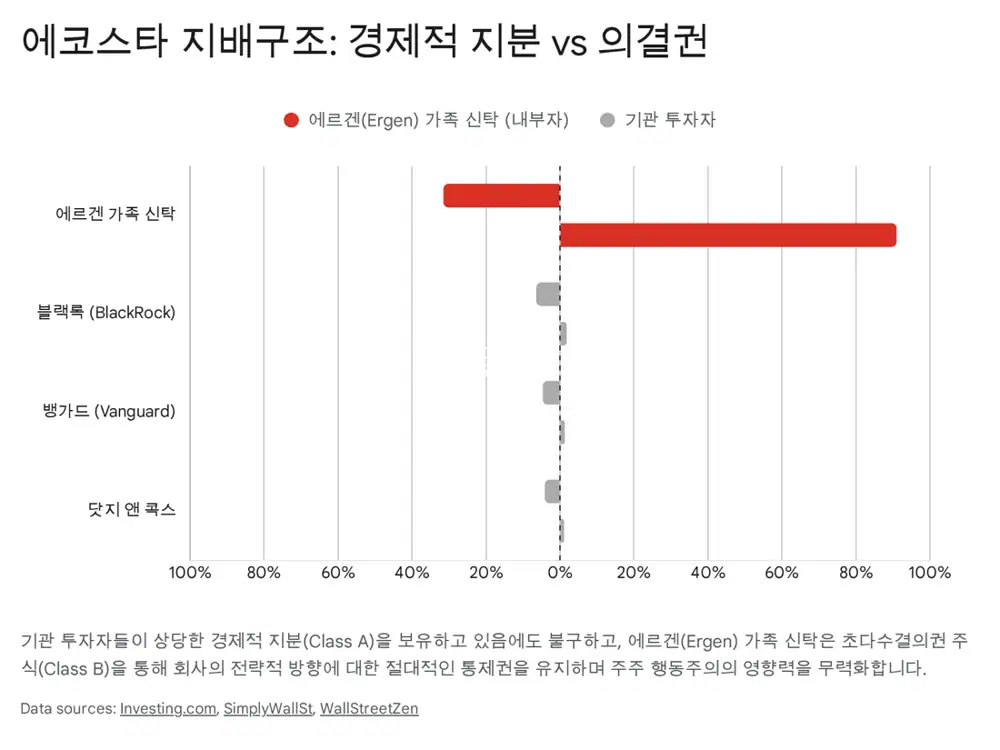

Charlie Ergen control

Ergen holds about 51.5% economic ownership and more than 90% voting control through Class B shares.

S-Band moat

Globally harmonized S-Band 2GHz rights are a critical resource for SpaceX direct-to-device service.

From builder to architect

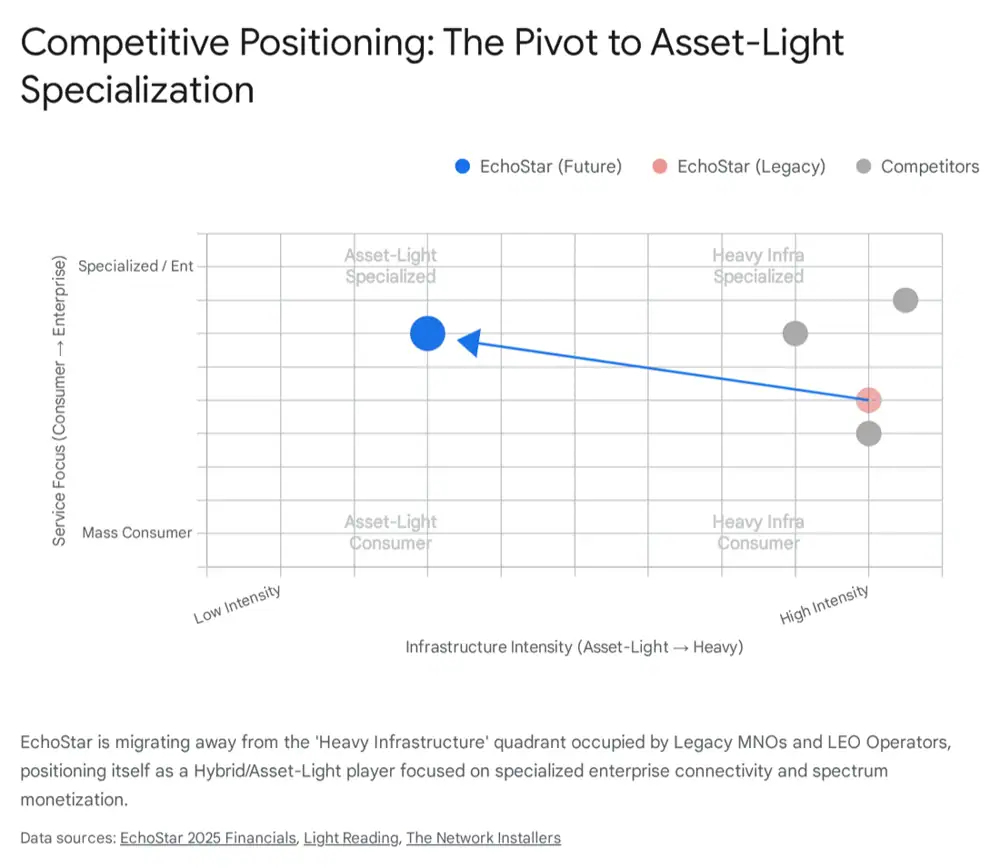

EchoStar is abandoning standalone physical 5G buildout and moving toward a core-network and spectrum-centered hybrid MNO.

1. Identity and governance

EchoStar is no longer simply a satellite-TV operator or aspiring fourth mobile carrier. The source defines it as a hybrid connectivity architect and spectrum-asset manager spanning terrestrial networks, GEO satellites, and non-terrestrial networks.

Official fact: Charlie Ergen beneficially owns about 51.5% across Class A and Class B shares, while controlling more than 90% of voting rights through super-voting Class B shares. Major institutional holders cited are BlackRock at 6.42%, Vanguard at 4.66%, and Dodge & Cox at 4.10%.

- Charlie Ergen returned as CEO & Chairman and directly oversees Pay-TV, DISH/Sling, Wireless, and Boost Mobile operations.

- Hamid Akhavan moved to CEO of EchoStar Capital, responsible for investing in TMT, aerospace, defense, and other new growth areas.

- Ergen directly held about 13.7 million shares worth about $1.4B as of November 2024, linking shareholder value to personal wealth.

Interpretation: This governance structure blocks activism and enables fast asset-sale decisions, but it also raises key-person and capital-allocation risk.

2. Technology stack: GEO satellite, hybrid 5G, S-Band D2D

Official fact: Jupiter 3, or EchoStar XXIV, is a large commercial communications satellite built by Maxar. It uses Q/V-Band feeder links to maximize user Ka-Band capacity and provides more than 500Gbps of throughput through more than 300 spot beams.

Official fact: In Q3 2025, EchoStar recognized a $16.48B impairment charge and scaled back its standalone physical 5G buildout. The new model keeps the 5G core network in-house while using AT&T infrastructure for RAN, towers, and antennas.

S-Band 2GHz has a lower frequency than Ku/Ka bands, so it has less rain fade and relatively better building penetration. The source’s technical view is that it is well suited for direct satellite communication with smartphones and small IoT devices.

| Technology | TRL assessment | Basis |

|---|---|---|

| Jupiter 3 System | TRL 9 | Launched in July 2023, commercial HughesNet service, 500Gbps-class performance validated |

| 5G Open RAN physical network | TRL 8 → Retired | 80% US population coverage and VoNR commercialized, then retired due to weak economics |

| Hybrid MNO Core | TRL 7 | EchoStar 5G core and AT&T RAN interworking are operating, with large-scale optimization ongoing |

| S-Band D2D | TRL 6 | Validated with Lyra-4, but large-scale Starlink constellation deployment remains early |

3. Moats and competitive landscape

Official fact: The source says EchoStar completed the bringing-back-into-use process for ITU S-Band 2GHz rights, the SIRION-1 filing, through the launch and operation of Lyra-4. This is framed as the reason SpaceX had to enter a $17B-scale cooperation.

- Technology moat: MSS-dedicated S-Band is relatively free from the interference-coordination problems that arise when terrestrial spectrum is reused from space.

- Regulatory moat: the AT&T and SpaceX transactions are framed as removing FCC buildout obligations and license-cancellation risk.

- Defense moat: Hughes is a DoD partner and has a Spiral 4 IDIQ contract worth up to $2.7B for the US Navy and federal agencies.

- Switching-cost moat: BSS has about $1.5B in backlog, and customers face high site-by-site equipment replacement costs.

| Comparison | EchoStar | Starlink | Viasat | T-Mobile |

|---|---|---|---|---|

| Core asset | GEO satellites + S-Band | LEO constellation + launch vehicles | GEO satellites | Terrestrial 5G network |

| Latency | High, about 600ms | Low, about 20~40ms | High, about 600ms | Very low, below 20ms |

| Business model | Asset-light pivot and spectrum leasing | Vertically integrated manufacturing, launch, and service | Equipment manufacturing + service | Infrastructure buildout + service |

| Government/defense strength | Very high | High | High | Medium |

Interpretation: EchoStar is no longer trying to fight Starlink head-on in consumer satellite broadband. It is being repositioned to supply spectrum that Starlink needs and to focus on specialized defense and enterprise connectivity.

4. Business structure and cash-flow reversal

| Segment | Q3 2025 source figure | Structural meaning |

|---|---|---|

| Pay-TV | Revenue $2.34B, down 10.6% YoY | DISH TV and Sling TV act as cash sources, not growth engines |

| Wireless | Revenue $939M, up 4.5% YoY, Boost Mobile net adds of 223,000 | Physical network cost reduction and wholesale-network model shift |

| BSS | Revenue $346M and backlog of $1.5B | Aviation, enterprise managed networks, and government customer base |

Official fact: As of September 30, 2025, cash and equivalents were $2.43B while current liabilities due within one year were $4.52B, creating a going-concern warning.

Official fact: If the $22.65B AT&T transaction and $19B SpaceX transaction close, liquidity of about $41.65B would be secured. The source’s pro-forma scenario says the company could repay about $21.8B of long-term debt and still have about $20B of cash and stock remaining.

- Q3 2025 cumulative operating cash flow was $326M, sharply lower than $1.2B in the prior-year period.

- Q3 2025 cumulative capex was $1.48B, but the source estimates capex could fall to annual maintenance levels of $200M~$400M from 2026 after the network buildout is stopped.

- The SpaceX deal includes $2.6B of SpaceX stock, giving it option-like upside if SpaceX eventually goes public.

5. Customers, roadmap, and risks

Defense anchor tenant

The DoD is the most important customer group, and Spiral 4 is presented as a stable revenue base for the next 10 years.

$1.5B backlog

Backlog is based on airlines, retail chains, and energy companies using backup and remote connectivity networks.

Downward pressure

DISH TV loses 200,000~300,000 subscribers per quarter, while Boost Mobile rebounded with 223,000 net adds in Q3.

Official fact: The source expects the D2D market to grow at a 32% CAGR to $10B by 2035, and the NTN market to reach $25B by 2035.

10-year roadmap

- 2025~2026: close AT&T/SpaceX deals, repay high-cost debt, and clean up physical 5G assets

- 2027~2029: EchoStar Capital leads $10B~$15B of M&A

- 2030 onward: D2D royalties and reinvested portfolio mature, shifting toward a communications-asset holding company model

Key risks

- If the DOJ or FCC blocks the AT&T or SpaceX deals, the liquidity crisis could return.

- Partner dependence could increase if AT&T raises wholesale rates or SpaceX gains leverage in spectrum-fee negotiations.

- If LEO satellite costs keep falling, the value of the GEO satellite Jupiter 3 could be impaired.

- If Charlie Ergen deploys cash into another high-risk project instead of shareholder returns or disciplined M&A, capital-allocation failure could repeat.

Interpretation: If the transactions close, EchoStar could be reborn as a debt-free holding company with large cash reserves and royalty exposure to the space economy. If approvals or capital allocation fail, the special-situation thesis weakens quickly.

Sources

- Original Naver Blog post: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116728104

- Who Owns EchoStar? SATS Shareholders - Investing.com: https://www.investing.com/equities/echostar-corp-ownership

- Charles W Ergen Net Worth - GuruFocus: https://www.gurufocus.com/insider/1909/charles-w-ergen

- JUPITER 3 - Hughes: https://www.hughes.com/what-we-offer/satellite-services/jupiter-geo-satellites/JUPITER3

- Light Reading Jupiter 3 service article: https://www.lightreading.com/satellite/hughes-opens-data-spigot-as-new-broadband-satellite-enters-service

- Jupiter 3 - Wikipedia: https://en.wikipedia.org/wiki/Jupiter_3

- JUPITER GEO Satellites - Hughes: https://www.hughes.com/what-we-offer/satellite-services/jupiter-geo-satellites

- Light Reading EchoStar 5G performance: https://www.lightreading.com/5g/echostar-s-fleeting-5g-network-continues-to-underperform-its-peers-ookla

- EchoStar NTIA filing PDF: https://www.ntia.gov/sites/default/files/publications/echostar.pdf

- EchoStar SpaceX commercial agreement release: https://ir.echostar.com/news-releases/news-release-details/echostar-announces-spectrum-sale-and-commercial-agreement-spacex

- EchoStar Mobile satellite D2D IoT blog: https://echostarmobile.com/blog/expanding-iot-opportunities-with-satellite-direct-to-device-connectivity-and-compact-antennas/

- EchoStar worldwide 2 GHz NGSO rights release: https://ir.echostar.com/news-releases/news-release-details/echostar-perfects-highest-itu-priority-worldwide-2-ghz-ngso

- EchoStar US Navy wireless contract release: https://ir.echostar.com/news-releases/news-release-details/echostar-awarded-us-navy-wireless-and-telecommunications

- US Army Fort Bliss 5G Open RAN release: https://ir.echostar.com/news-releases/news-release-details/us-army-selects-echostars-hughes-deploy-5g-open-ran-ran

- 3GPP Release 19: https://www.3gpp.org/specifications-technologies/releases/release-19

- Medium NTN and D2C growth note: https://medium.com/technology-media-telecom/ntn-and-d2c-25b-growth-by-2035-459dc4d39a47

- ABI Research NTN and D2C market release: https://www.abiresearch.com/press/global-ntn-and-d2c-market-revenue-to-reach-us25-billion-by-2035-as-tech-giants-satellite-operators-and-mnos-transform-global-connectivity