DEEP RESEARCH · Sungho Electronics (043260) / ADStech

Sungho Electronics' Strategic Acquisition of ADStech — Deep Dive

The 'Missing Link' of AI infrastructure and the geopolitical reshoring premium — a KRW 280B bet on the future of AI connected by light.

0. Bottom line first

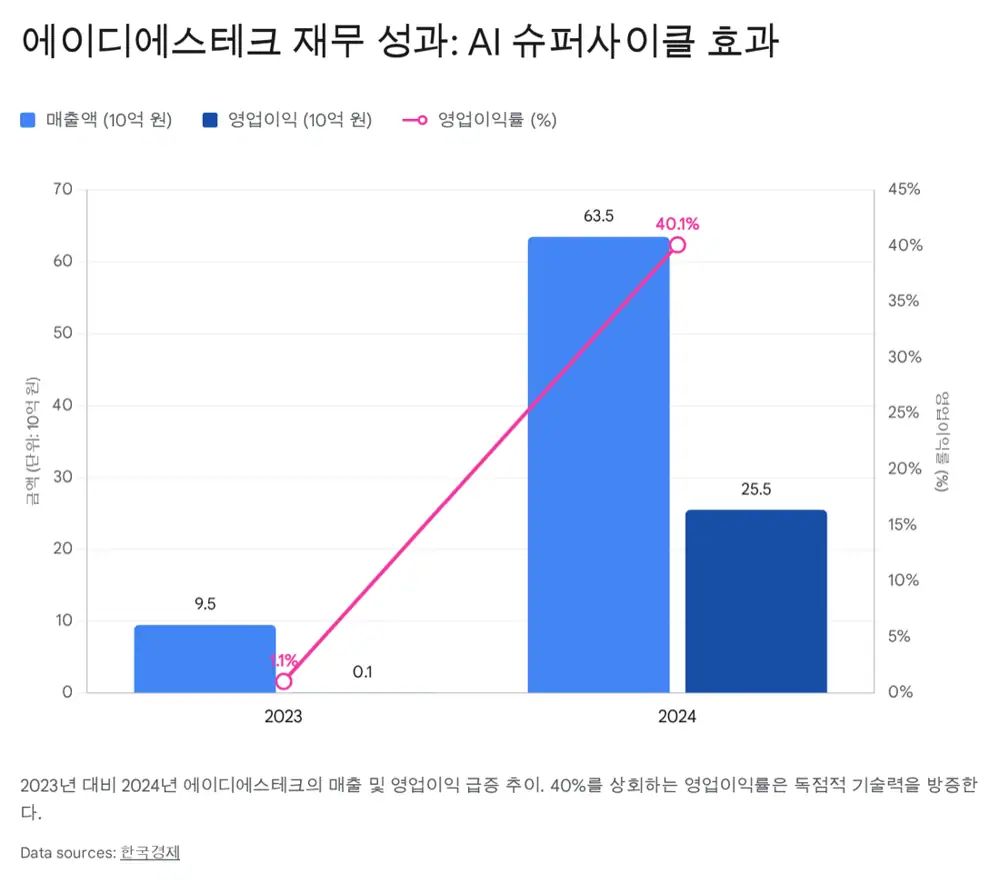

Sungho Electronics acquired 87.5% of ADStech for KRW 280B, equal to 76.23% of Sungho's 2024 total assets (KRW 367.3B) and 182.44% of its equity (KRW 153.5B) — a 'bet-the-company' move. Thesis: (1) ADStech is one of only two global suppliers of high-end active alignment equipment (the other being Germany's ficonTEC); (2) ficonTEC's acquisition by Chinese capital makes ADStech the sole 'Safe Zone' option for the Western supply chain; (3) ADStech's 2024 numbers — revenue KRW 63.5B (+568%), operating profit KRW 25.5B (OPM 40.1%) — confirm an early-cycle quantum leap.

1. Market dynamics — electronics → photonics

Official fact: AI bottlenecks have moved from compute to interconnect. Data flowing out of H100/Blackwell-class GPUs pushes server-to-server bandwidth past 400G toward 800G and 1.6T. Copper signal loss and heat make this physically impossible — optical is mandatory.

Interpretation: Global optical transceiver TAM is set to grow from $13.6B (2024) to $25B (2029, ~13% CAGR), with 800G+ growing far faster. The shift from passive to active alignment (required at 400G+) directly expands ADStech's TAM.

2. Core technology — Active Alignment

Transceiver performance is determined by coupling efficiency from the laser diode to the optical fiber, which requires nanometer-precision alignment.

3. Competitive structure & geopolitical alpha — ficonTEC's 'Chinification'

| Item | ADStech | ficonTEC |

|---|---|---|

| Country | South Korea | Germany (acquired by Chinese capital) |

| Owner | Sungho Electronics (Korean capital) | Robotechnik (Chinese capital) |

| Core tech | Active Alignment, High-speed Assembly | Automated Micro-assembly, Testing |

| Key customers | Mellanox (Nvidia), Fabrinet | Intel, Cisco, Huawei |

| Geopolitical risk | Safe Zone (US ally) | Risk Zone (China tech control) |

| Strengths | Nvidia-aligned supply, cost performance, fast CS | Broad product line, EU R&D network |

Official fact: Robotechnik paid an astonishing premium (approx 9,915% over book value) for ficonTEC — proof of the technology's strategic value. But the US Commerce Department's restrictions on advanced equipment exports to China, and US fabless players' supply-chain security policies, are simultaneously pushing customers away from ficonTEC.

Interpretation: ADStech becomes the only 'Safe Zone' alternative. With Mellanox already >90% of revenue, when 1.6T lines expand, ADStech equipment is the structural default — a built-in moat.

4. Financials — hockey-stick turnaround

- Revenue: KRW 9.5B (2023) → KRW 63.5B (2024), +568%. Reflects AI data-center optical-transceiver demand exploding in H2-2023.

- Operating profit: <KRW 100M (BEP) → KRW 25.5B.

- OPM: 40.1% — extreme for a manufacturer. Signals high-IP margin, lack of competition, pricing power, and operating leverage on a still-low fixed-cost base.

5. Valuation — PER 16× looks like a bargain

Official fact: 87.5% stake for KRW 280B implies a 100% enterprise value of ~KRW 320B. Against an estimated 2024 net income of KRW 20B, that's ~16× PER.

| Comparable | PER | Note |

|---|---|---|

| ADStech (acquisition implied) | ~16× | Assumes KRW 20B 2024 NI |

| ficonTEC (Robotechnik deal) | 70–80× | Future growth priced in |

| Robotechnik (300757.SZ) itself | 150×+ | 2025E basis |

| Korean semi-equipment peers | 30–60× | Hanmi, HPSP, Park Systems |

Interpretation: Against 70–150× global peers and 30–60× domestic peers, ADStech at 16× is materially undervalued. A fair re-rating to at least 30× implies enterprise value of KRW 600B+ — Sungho effectively bought a gem at a discount.

6. Sungho's big picture — 'Power · Cool · Connect'

7. Risks

- Customer concentration: >90% of revenue from Mellanox (Nvidia). Dual sourcing or a technology shift would hit hard. Near-term alternatives are unlikely to emerge.

- PMI failure risk: Traditional manufacturer Sungho integrating an R&D-led ADStech is non-trivial; engineer attrition could be devastating.

- Overhang: Total KRW 80B of CB + BW issuance — eventual conversions dilute existing holders.

- Interest costs: Acquisition financing adds burden, but ADStech's KRW 25B+ operating profit should comfortably cover interest, producing positive leverage.

8. Scenarios

Bull (Strong Buy)

- Full-year ADStech consolidation in 2026 drives Sungho re-rating. 1.6T / CPO cycle could push ADStech revenue past KRW 100B.

Base

- Acquisition momentum coexists with overhang. Medium term, the 16× 'bargain buy' narrative materializes.

Bear

- Nvidia price pressure or supply diversification slows growth.

- Accelerated CB/BW conversions weigh on near-term supply.

9. Conclusion

"Sungho is no longer a simple component company. It now owns a key piece of equipment that builds the data highways of the AI era. ADStech combines geopolitical alpha and a deep technical moat — a powerful engine to redefine Sungho's corporate value." — Mind near-term volatility, but a Strong Buy from a medium- to long-term horizon.

Sources

- Naver blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116725664

- Sungho acquires 87.5% of ADStech for KRW 280B (Marketin): marketin.edaily.co.kr

- Robotechnik (300757) acquires ficonTEC (Futu): news.futunn.com

- RBT Technology (300757.SZ) Pre-IPO Insights: news.futunn.com

- Sungho CB KRW 50B / BW KRW 30B issuance (Marketin): marketin.edaily.co.kr

- Optical Transceiver Market Size (M&M): marketsandmarkets.com

- NVIDIA Spectrum-X Photonics / CPO: investor.nvidia.com

- Active vs Passive Alignment (PI): pi-usa.us

- Photonics Alignment Techniques (Physik Instrumente): physikinstrumente.com

- ADS Tech product page: adst.co.kr

- ficonTEC capabilities: ficontec.com

- CPO Switch (ficonTEC): ficontec.com

- Silicon Photonics CPO (IMEC): imec-int.com

- ficonTEC × Robotechnik investment agreement: ficontec.com

- Robotechnik 12 announcements (Moomoo): moomoo.com

- Robotechnik 100× premium acquisition (Futu): news.futunn.com

- EU semiconductor ecosystem economic analysis: ec.europa.eu

- Robotechnik ficonTEC acquisition plan (Futu): news.futunn.com

- Park Systems (Daishin Securities note): money2.daishin.co.kr

- Sungho transformer business analysis (Google Drive): drive.google.com