DEEP RESEARCH · Celestica (NYSE: CLS)

Celestica (CLS) Deep Dive: Structural Beneficiary of the AI Infrastructure Super-Cycle

From commodity EMS to AI data center solutions provider — examining HPS hyper-growth and the valuation re-rating

0. Bottom line first

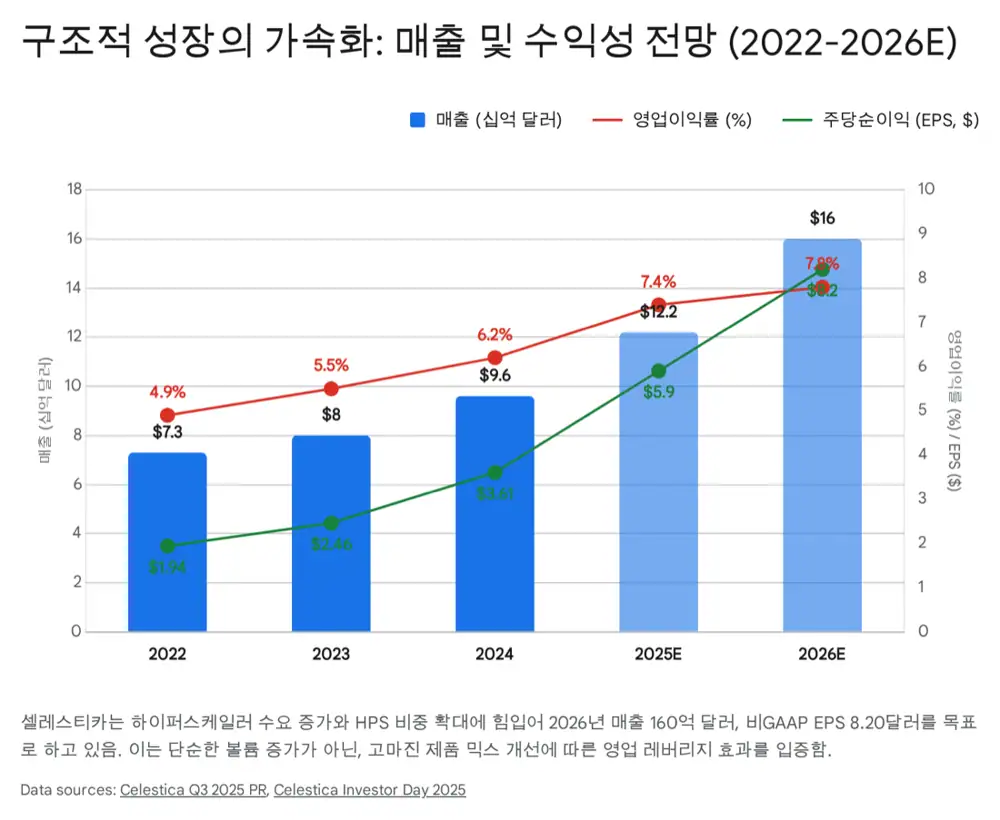

Celestica is no longer a low-growth, low-margin traditional EMS. Its business mix has shifted toward HPS (in-house designed solutions), and it has secured a dominant position in AI back-end network switching with 41% (200G+) and 55% (custom) market share. 2025 revenue guidance was raised from $11.55B to $12.2B; 2026 guidance stands at $16B. A company with 50%+ earnings growth trading at 14–22x P/E — Q, P, and C are all moving favorably at once in a "triple-tailwind" window.

Guidance raise

2025 revenue $11.55B → $12.2B; 2026 $16B. 800G/1.6T switches and AI rack solutions entering volume production.

HPS mix shift

Higher HPS share drives a structure where profit grows faster than revenue. Turn-key solutions justify premium pricing.

Operating leverage

3Q25 non-GAAP operating margin 7.6% — all-time high. 2026 target 7.8%. Thailand/Malaysia hubs hedge cost and tariff risk.

1. Introduction: The EMS paradigm shift and where Celestica sits

The global tech hardware industry is undergoing fundamental restructuring under the AI/ML wave. The traditional EMS industry — once a pure-play assembler following OEM blueprints — is now evolving into complex technology partnerships demanding advanced engineering, supply chain management, and independent design capability (JDM/ODM). Canada-based Celestica (NYSE: CLS) is one of the most dramatic transformations in this shift, moving from low-margin contract manufacturing to a trusted technology partner for hyperscalers' AI data center build-outs.

This report analyzes Celestica's 3Q 2025 results and 2025/2026 annual outlook, focusing on the explosive growth of HPS within CCS, its technological moat, valuation appeal versus global peers (Jabil, Flex), and key risks.

2. Reshaping the business: evolution toward high-value HPS

Celestica is split into two pillars: CCS (Connectivity & Cloud Solutions) and ATS (Advanced Technology Solutions). Where the two segments were once balanced or ATS provided stability, AI infrastructure spending has elevated CCS — and especially HPS (Hardware Platform Solutions), which concentrates in-house design capability — to the dominant growth engine.

2.1 CCS — the backbone of AI data centers

Official fact: 3Q 2025 CCS revenue surged 43% YoY to $2.41B. Segment margin reached 8.3%, up 70bps from 7.6% a year earlier.

Interpretation: This is not just volume growth. The margin move proves the body-shift from low-margin assembly to high-margin solutions is working.

2.1.1 The HPS explosion

Official fact: 3Q 2025 HPS revenue was about $1.4B, up 79% YoY, accounting for over half of CCS revenue. Full-year 2025 HPS revenue is projected at $5.0B, up 80% YoY.

Interpretation: HPS is not commodity manufacturing — it integrates design, engineering, prototyping, mass production, and supply chain in a JDM/ODM model. Its outsized growth is the core variable justifying Celestica's valuation re-rating.

2.1.2 Deepening hyperscaler partnerships

Official fact: Customer concentration sits with Amazon, Google, Meta, and Microsoft — the top 4 hyperscalers. Hyperscaler revenue mix is projected to expand from 51% in 2022 to 77% in 2025.

Interpretation: What was once flagged as a concentration risk is now Celestica's strongest competitive advantage. The company sits directly in the path of Big Tech's astronomical CapEx.

2.2 ATS — portfolio optimization and stability

Official fact: 3Q 2025 ATS revenue was $0.78B, down 4% YoY, but margin improved to 5.5%, up 60bps from 4.9%.

Interpretation: The revenue decline reflects strategic exit of low-margin programs (de-marketing). Management is reshaping ATS around profitability and ROIC rather than headline growth, targeting a return to mid-single-digit growth from 2026. The Capital Equipment unit within ATS is tied to the AI chip fab build cycle and represents additional upside.

3. Competitive edge: moat and vertical integration

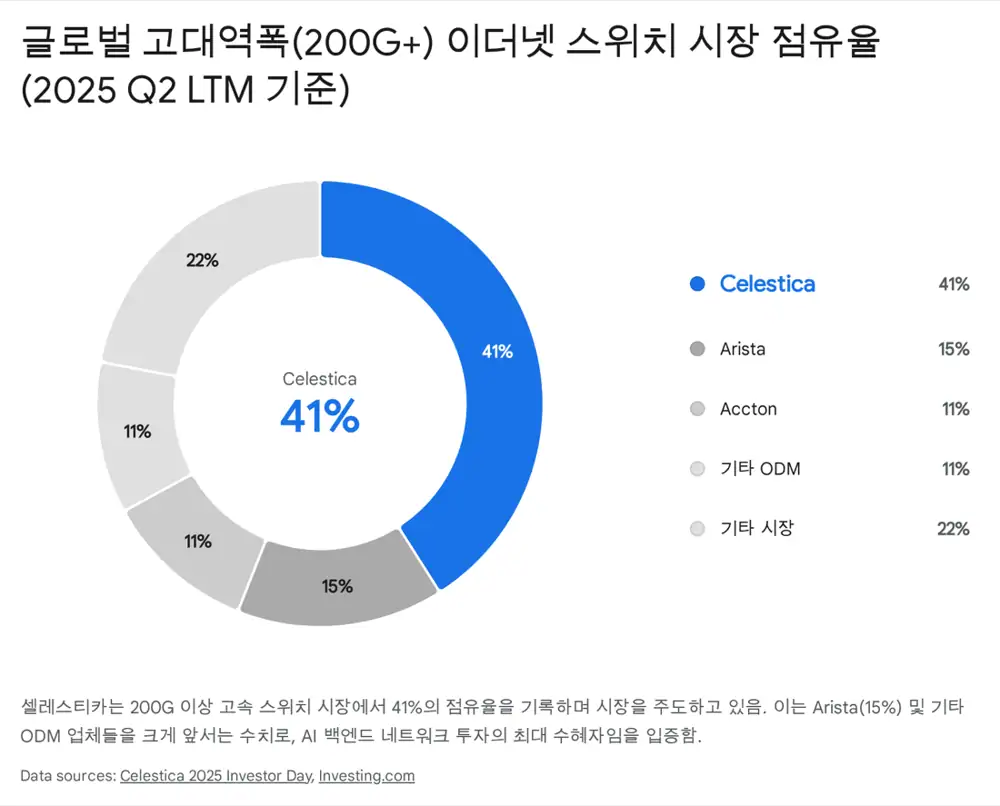

3.1 Dominant position in high-speed switching

Official fact: 41% share in the 200G+ high-bandwidth Ethernet switch market — outpacing traditional leader Arista (15%) and Accton (11%). In custom Ethernet switch solutions, Celestica holds 55% share YTD 2025.

Celestica 41%

Leader in high-bandwidth Ethernet switching.

Arista 15%

Established networking incumbent.

Accton 11%

Key ODM competitor.

Celestica 55%

Customer-specific solution share.

3.2 Strategic technology partnership with Broadcom

Interpretation: The technology edge stems from close collaboration with Broadcom. Celestica is pre-developing switch platforms using Broadcom's latest Tomahawk 6 silicon, meeting the Time-to-Market demands hyperscalers require — a barrier to entry rivals cannot easily replicate.

3.3 Vertical integration — turn-key solutions

Celestica internalizes the full stack: design, prototyping, mass production, system integration testing, and global supply chain management. Beyond standalone switches it delivers rack-level solutions that integrate AI servers, storage, and cooling. Proactive investment in next-generation thermal management — including liquid cooling for high-heat AI servers — further strengthens competitive positioning for new wins.

4. End-market outlook: AI data centers and network infrastructure evolution

As AI model parameters scale into the trillions, the data center's core competitive lever expands from "compute" to "connectivity" between GPUs. This opens an unprecedented opportunity in the high-performance networking market Celestica targets.

4.1 The rise of the back-end network

AI training and inference involve thousands of GPUs exchanging data simultaneously, so back-end bandwidth and latency determine overall system performance. Hyperscalers are investing heavily in back-end infrastructure, and Celestica's high-performance switches are being adopted as core components of that back-end fabric.

4.2 Speed race: 400G to 1.6T quantum leap

Official fact: Per Dell'Oro Group and 650 Group, growth in the AI networking market will be led by 800G+ ultra-high-speed ports. Celestica has already won 1.6T switch programs from key hyperscalers, with volume production scheduled to start in 2H 2026.

4.3 Structural shortages and supply chain management

Supply remains tight for high-layer-count boards (MLB), copper-clad laminate (CCL), and glass fiber used in AI accelerators. Celestica mitigates this by reinforcing long-term partnerships with key component suppliers and pre-collecting Customer Cash Deposits to share working capital burden with customers.

5. Earnings drivers: the Q · P · C framework

Quantity, price, and cost — the three core profit variables — are all moving in Celestica's favor at once: a "triple-tailwind" window.

5.1 Quantity — explosive demand and high-visibility backlog

- Guidance raise: 2025 revenue guidance lifted from $11.55B to $12.2B; 2026 guidance set at $16B. Publishing detailed guidance two years out signals strong conviction in backlog and customer CapEx plans.

- New program ramp: Multiple 800G and 1.6T switch programs plus AI server rack solutions are scheduled for volume production in 2H 2025 and 2026.

5.2 Price — mix improvement and pricing power

- HPS share expansion: The rising HPS share structurally improves the product mix, so profit grows faster than revenue.

- Turn-key premium: Rack-level integrated solutions deliver Time-to-Market and Plug-and-Play value — justifying premium pricing versus standalone module sales.

5.3 Cost — operating leverage and footprint optimization

- Operating leverage: Revenue is growing faster than fixed costs. 3Q 2025 non-GAAP operating margin hit 7.6% — an all-time high. 2026 target is 7.8%.

- Footprint: Strategic placement across Thailand, Malaysia, Mexico, and Texas. This hedges U.S.–China tariff risk while enabling near-shore production for North American customers, reducing logistics costs and lead times.

6. Financial health and capital allocation

6.1 Strong cash generation

- FCF raised: 2025 free cash flow guidance raised from $400M to $425M; 2026 target $500M. Revenue and margin gains are translating into real cash inflows.

- Healthy leverage: Non-GAAP adjusted net debt / EBITDA stands at 1.0x — very healthy versus industry averages, preserving flexibility for future investment or M&A.

6.2 Shareholder-friendly capital allocation

- NCIB: The new normal course issuer bid plans to repurchase and cancel up to 5% of shares outstanding.

- Reinvestment: Continued R&D and North American capacity investment funds future growth.

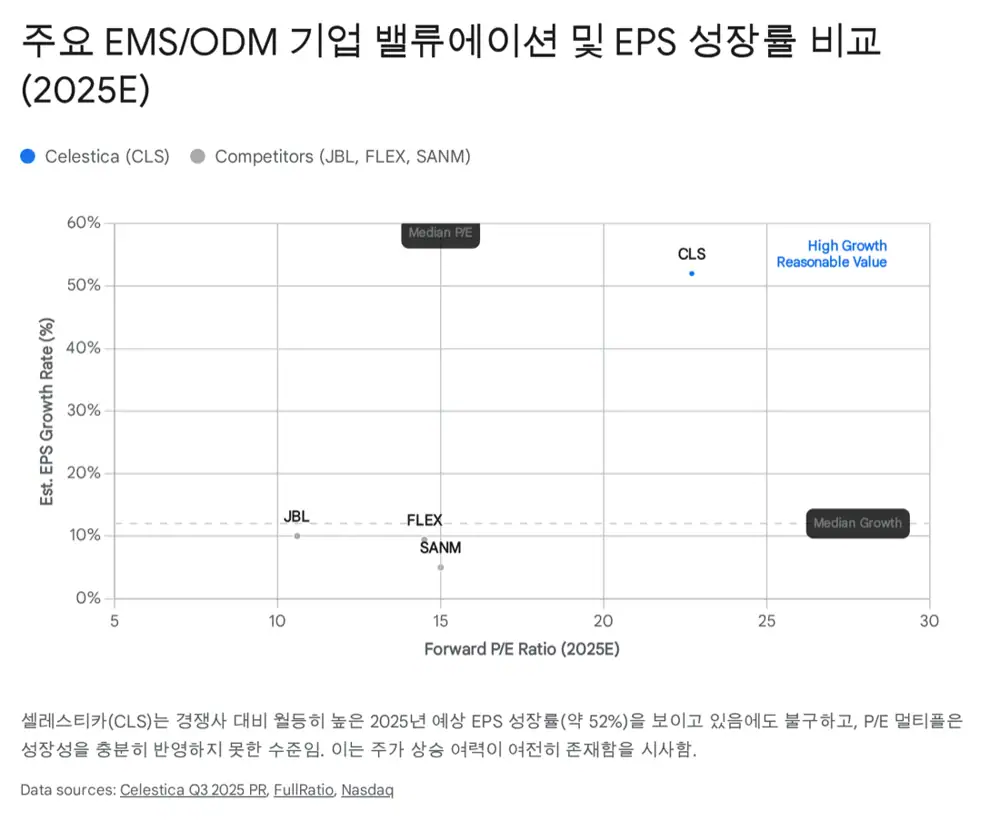

7. Valuation and risk

7.1 Justifying the re-rating

| Company | Forward P/E | Note |

|---|---|---|

| Celestica (CLS) | ~14–22x | 2025E EPS growth 52% |

| Jabil | ~10–18x | Peer |

| Flex | ~14x | Peer |

Interpretation: Celestica's headline P/E looks slightly higher, but on a PEG basis — given 50%+ earnings growth — it is actually undervalued. A company expected to grow earnings 50%+ trading in the low-20s P/E is rare in the AI sector.

7.2 Key risks

Top 4 hyperscalers

A strategy shift or CapEx cut would hit results immediately. With intense AI competition, however, near-term cuts look unlikely.

U.S.–China tensions

Most tariff costs are contractually passable to customers. Diversified footprint (Thailand, Mexico) hedges further.

Next-gen (e.g. CPO)

Beyond 1.6T, failure to keep leadership through the Co-Packaged Optics transition could erode share.

8. Conclusion: a real beneficiary of the AI infrastructure build-out

Celestica has entered a structural growth phase backed by (1) a successful transition to an HPS-led high-margin business mix, (2) dominant technology leadership in AI network switching, and (3) deep partnerships with hyperscalers. Strong 2025/2026 guidance and the raised FCF target reflect management's confidence.

From an investor's perspective, Celestica should be seen not as a contract manufacturer but as a core solutions provider designing and building the AI data center infrastructure itself. Today's valuation does not yet fully reflect that explosive growth potential. For investors seeking "Pick and Shovel" exposure to AI infrastructure build-out — beyond chipmakers like Nvidia — Celestica is a compelling alternative.

Sources

- Naver blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116350172

- Celestica Q3 2025 slides: AI-driven growth propels 31% revenue outlook for 2026 — investing.com

- Celestica Inc. Upgraded To 'BB+' On Strong Operat — S&P Global Ratings

- Broadcom Ships Tomahawk 6: World's First 102.4 Tbps Switch — broadcom.com

- 0001104659-25-102804 | 8-K | iXBRL Viewer | Celestica INC — corporate.celestica.com

- Celestica Achieves Key Milestones in Market Share and Growth for Data Center Switching (Dell'Oro Group Report) — celestica.com

- Data Center AI Networking to Surge to Nearly $20B in 2025 (650 Group) — 650group.com

- ITServices 2026 Annual Outlook — Surviving the Shortage in the AI Boom (Isu Petasys, Samsung Electro-Mechanics, 2025-11-24, SK) — drive.google.com

- Celestica vs. Flex: Which EMS Stock Has Better Growth Potential? — Nasdaq