DEEP RESEARCH · MOBIIS

Mobis: From Big Science Control Systems to Industrial AI

A review of 2025 Q3 results, backlog, and revenue visibility from smart-factory and fusion-control projects

0. Bottom line first

Mobis is still facing lower revenue and operating losses through 2025 Q3, but the rising smart-factory revenue mix and KRW 4.95318 billion backlog improve 2026 revenue visibility. The key is whether its Big Science control references repeatedly convert into private manufacturing AI and MES revenue.

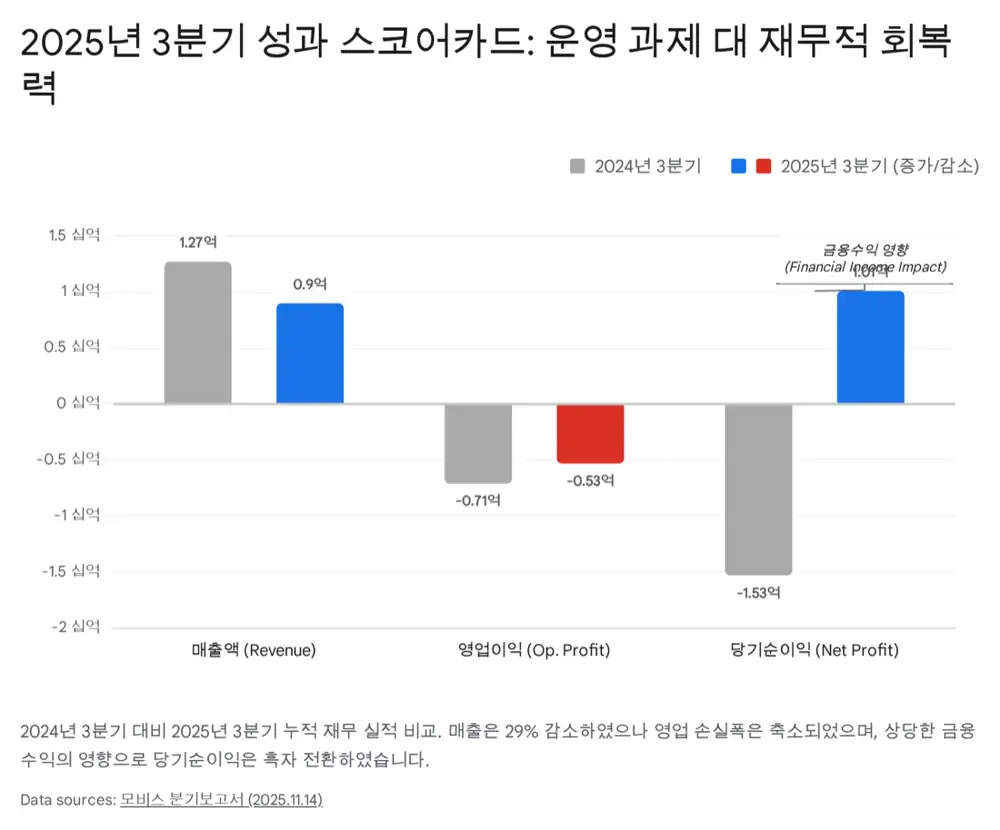

Official fact: The source cites 2025 Q3 cumulative revenue of KRW 3.83287 billion, operating loss of KRW 1.6845 billion, and net income of KRW 613.52 million. It compares those with prior-year revenue of KRW 5.02643 billion, operating loss of KRW 2.21034 billion, and continuing-operation net loss of KRW 2.59557 billion.

Interpretation: The operating line still reflects project gaps and fixed-cost burden, but financial income and liquidity are absorbing the loss. I view this as a project-based technology stock where the 2026 revenue-recognition schedule matters more than current earnings quality.

1. 2025 Q3 financial performance

Mobis began in the specialized field of precision control systems for particle accelerators and nuclear fusion reactors. As of 2025 Q3, it is in transition, using basic-science references to expand into smart factories and industrial AI solutions.

| Item | 2025 Q3 cumulative | Comparison | Read |

|---|---|---|---|

| Revenue | KRW 3.83287 billion | Down about 23.7% from KRW 5.02643 billion | Large project completion and early-stage new projects |

| Operating profit | -KRW 1.6845 billion | Loss narrowed from -KRW 2.21034 billion | Some cost-control effect visible |

| Net income | KRW 613.52 million | Rebound from continuing-operation net loss of KRW 2.59557 billion | Financial income of KRW 3.14149 billion absorbed operating loss |

The source interprets the roughly KRW 31 billion of liquidity secured through the ADM Korea stake sale as a financial buffer that offsets operating losses through interest income and related gains.

2. Business mix: smart factory expands

KRW 1.38938 billion · 36.25%

Mainly engineering service revenue for ITER and domestic accelerator laboratories.

KRW 2.44348 billion · 63.75%

Private-company projects such as Heesung Catalyst and Sunil Dyfas are becoming the main revenue source.

Interpretation: A smart-factory revenue share above half suggests the technology can travel beyond public research institutes into private manufacturing sites.

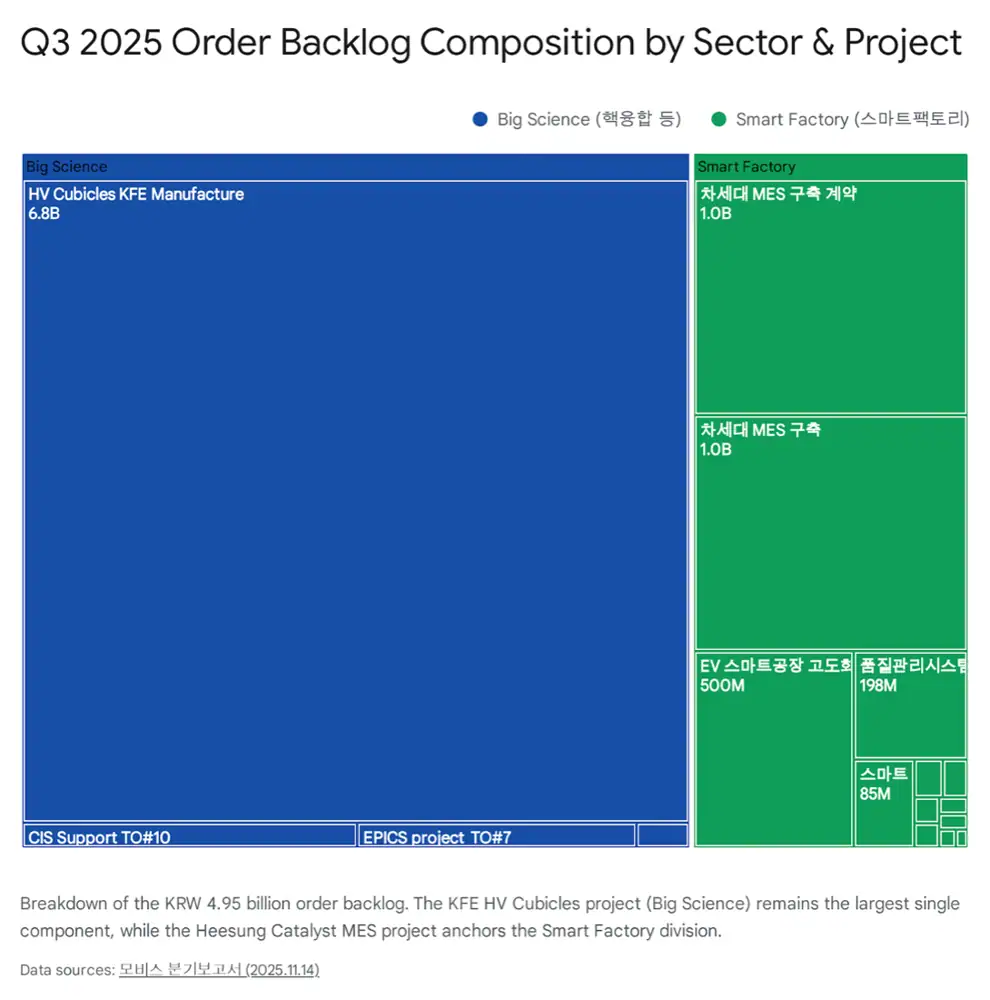

3. Backlog and key customers

Official fact: The source presents total backlog of KRW 4.95318 billion as of September 30, 2025. It says more than KRW 3 billion is expected to be recognized as revenue in 2026, meaning the company starts with about 60% of expected 2025 revenue already visible.

| Project/customer | Contract and backlog | Meaning |

|---|---|---|

| Heesung Catalyst next-generation MES | Total contract KRW 1.279 billion, backlog KRW 1.0291 billion, 2025.04.03-2026.08.03 | QRP/MES reference for strict automotive catalyst and materials quality data management |

| Sunil Dyfas integrated MES | The source mentions a KRW 1.69 billion integrated MES contract | Evidence of expanding private manufacturing partnerships |

| HV Cubicles | Stable revenue recognition expected through 2026 Q3 | Repeat reference in fusion and accelerator control supply chain |

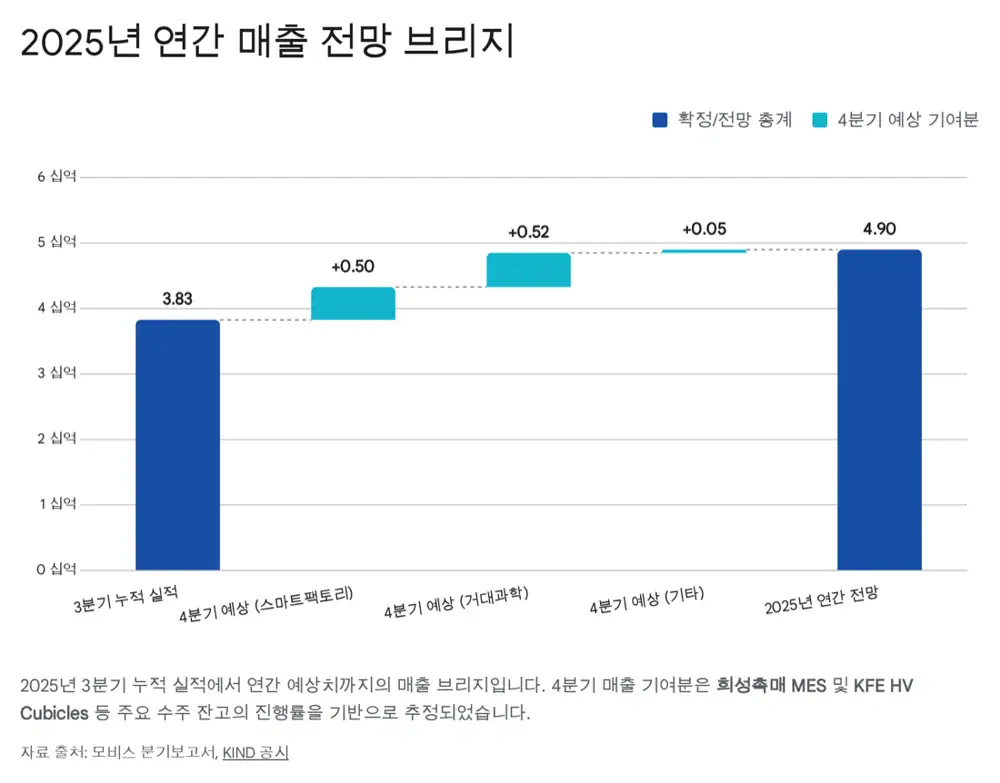

4. 2025 outlook and 2026 growth drivers

| Item | 2024 | 2025 Q3 cumulative | 2025 Q4 estimate | 2025 full-year outlook | YoY |

|---|---|---|---|---|---|

| Revenue | 50.3 | 38.3 | 14.5 | 52.8 | +5.0% |

| Operating profit | (23.9) | (16.8) | (3.5) | (20.3) | Loss narrowed |

| Net income | 92.2* | 6.1 | 0.5 | 6.6 | Profitable |

*Source note: 2024 net income includes discontinued-operation gain from the ADM Korea sale.

- 2026 revenue visibility: More than KRW 3 billion of the KRW 4.95 billion backlog is expected to be recognized in 2026; the source sees a high possibility of revenue above KRW 7 billion.

- Naju artificial sun: The government is pursuing a KRW 1.2 trillion artificial-sun research facility in Naju, targeted for completion in 2028.

- K-DEMO: If Korea's fusion demonstration reactor becomes visible, the company's addressable market could expand sharply.

- MOI-STD: The AI smart-factory solution launched in November 2023 creates the possibility of moving from one-off SI revenue to license and maintenance revenue.

5. Overall view

Mobis' near-term numbers show revenue decline and operating loss first. But the customer portfolio is broadening from government projects to private manufacturers such as Heesung Catalyst and Sunil Dyfas, and the 2026 backlog schedule is meaningful. Investors should focus less on 2025 earnings alone and more on backlog conversion, recurring revenue from MOI-STD, and actual order potential from Naju artificial sun and K-DEMO projects.

Sources

- Original blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116277923

- Mobis half-year report: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250812000618&docno=&viewerhost=&

- Bloter Heesung Catalyst contract: https://www.bloter.net/news/articleView.html?idxno=634369

- KRX supply contract: https://kind.krx.co.kr/common/disclsviewer.do?method=search&acptno=20250403000187&docno=&viewerhost=&

- Marketin contract article: https://marketin.edaily.co.kr/News/ReadE?newsId=02138566638861368

- Hankyung disclosure: https://www.hankyung.com/article/202404306637L

- KRX quarterly report: https://kind.krx.co.kr/external/2024/11/14/002115/20241114004713/11013.htm

- Mobis audit report: https://www.mobiis.com/index.php?tpf=common/save_as&file_path=/attachment/202503&file_name=1742285618938348.pdf&orig_name=%EC%A0%9C9%EA%B8%B0+%28%EC%A3%BC%29%EB%AA%A8%EB%B9%84%EC%8A%A4+%EA%B0%90%EC%82%AC%EB%B3%B4%EA%B3%A0%EC%84%9C.pdf

- Acrofan fusion control project: https://mkr.acrofan.com/article_sub3.php?number=241377