DEEP RESEARCH · SUNGHO ELECTRONICS

Sungho Electronics: Re-rating a Vertically Integrated Components Maker for Power and Mobility

Film capacitors, PSUs, metallized-film integration, and 2025 M&A expansion

0. Bottom line first

Sungho Electronics is moving through a structural transition from a traditional appliance and IT-parts supplier toward EVs, solar inverters, 5G equipment, power infrastructure, and semiconductor equipment. My core read is the combination of in-house metallized film, PSU-capacitor technology overlap, and the 2025 jump in consolidated subsidiaries from 9 to 14.

52-year electronics parts company

Founded as Jinyoung Electronics on May 15, 1973 and listed on KOSDAQ in November 2001, with PSUs and film capacitors as the two historical pillars.

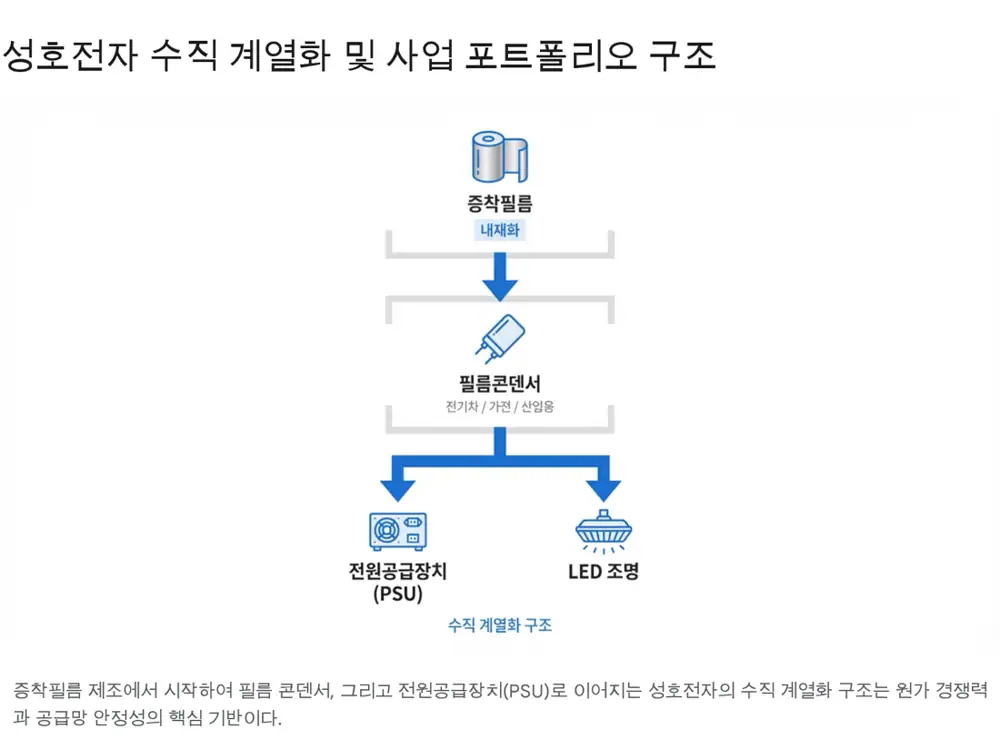

In-house metallized film

Sungho internally produces a core input that the source says accounts for roughly 40-50% or more of capacitor manufacturing cost.

From parts maker to industrial platform

By Q3 2025, consolidated subsidiaries increased from 9 at the beginning of the period to 14, expanding into power infrastructure and advanced equipment.

1. Company identity: from appliance parts to energy and auto electronics

Official fact: Sungho was founded in 1973 and has operated around power supply units and film capacitors. Its early end markets were white goods such as TVs, refrigerators, washing machines, plus PCs and printers.

Interpretation: Since the mid-2010s, electrification and clean energy have shifted the industrial backdrop. Sungho's portfolio is being reframed around EVs, solar inverters, 5G equipment, and power infrastructure. It is better understood as a vertically integrated materials-parts-module company than as a simple parts vendor.

2. Technical moat: metallized film and film capacitors

Official fact: Film capacitors use PP, PET, and other plastic films as the dielectric. They are preferred for industrial and automotive uses because of high-voltage, high-current, and temperature-stability characteristics. The key feature highlighted in the source is self-healing, where the deposited metal film vaporizes around a defect and isolates it.

Official fact: The source says Sungho has internal production lines for metallized film, a core material that can account for roughly 40-50% or more of capacitor manufacturing cost. That supports cost control, supply stability, and customized film properties.

Interpretation: EV drive inverters and onboard chargers require DC-Link capacitors that handle hundreds of volts and heavy ripple current. If Sungho can control ultrathin and heat-resistant films internally, delivery and quality response become meaningful advantages in high-spec auto electronics.

3. M&A and governance: the consolidated entity is growing quickly

Official fact: Based on the Q3 2025 quarterly report cited in the source, Sungho newly established JKI Holdings and Gusoo Heavy Electric Holdings, then acquired stakes in JKI, Gusoo Heavy Electric, and Jinsung Industry, bringing them into consolidation. Consolidated subsidiaries rose from 9 to 14.

Interpretation: The source infers that Gusoo Heavy Electric may be linked to heavy electrical equipment, transformers, switchgear, and power infrastructure. JKI and Jinsung Industry require further disclosure checks, but the source views them as possible expansions into semiconductor equipment or specialized industrial machinery.

- The source says the share price moved more than 500% from a 2025 low of KRW 895 and settled in the KRW 7,000 range, suggesting the market may be treating the change as a structural level-up.

- The opposite side is PMI cost, organizational integration, accounting cost, and consolidated liabilities from rapidly adding five subsidiaries.

4. Business structure: capacitors, PSUs, and metallized film

| Business | Core content | Growth logic |

|---|---|---|

| Film capacitors | High voltage/current, temperature stability, self-healing | Demand from EV inverters, OBCs, solar and wind inverters |

| PSU / SMPS | Power supplies that convert AC into stable DC | Printers, copiers, air purifiers, boilers, and LED lighting are cash cows; server and EV charger PSUs add growth |

| Metallized film | Vacuum deposition of Al or Zn onto base film | Direct control of thickness, margin pattern, and coating uniformity improves high-end capacitor development |

Official fact: The source says Sungho uses its Weihai, China entity as a production base and maintains long-term customers including HP and Sindoh in the traditional PSU business.

Interpretation: The traditional PSU business funds new-business investment, while capacitors and metallized film drive the shift into higher-margin automotive and renewable-energy products.

5. End markets: EVs, solar, and the power-grid supercycle

Official fact: EV inverters require DC-Link film capacitors to stabilize voltage and reduce noise while converting battery DC power into AC. The shift to 800V systems can increase both unit price and content per vehicle for high-spec film capacitors.

Official fact: The source says Sungho has secured supply references for Porsche and Audi EV platforms within Volkswagen Group. Because auto parts markets prioritize safety, a verified supplier reference has long-term value.

Official fact: The source cites the PV inverter market growing from USD 16.6 billion in 2025 to USD 27.6 billion in 2032 at an 18.62% CAGR. It also cites the global film capacitor market growing from about USD 4.84 billion in 2023 to USD 6.25 billion by 2030.

6. Financial and valuation checkpoints

Official fact: The source notes that the Q3 2025 expansion in consolidated subsidiaries materially changed Sungho's asset base and composition. It also states that exact Q3 revenue and operating-income figures were not included in the text basis, limiting precise numerical analysis.

- Debt ratio may have temporarily risen because acquisition financing and acquired-company liabilities enter consolidation. The source says the B+ stable credit rating as of May 2025 suggests leverage may be manageable.

- Quarter-end cash and equivalents may reflect both M&A cash outflows and cash held by newly consolidated subsidiaries. Operating cash flow is the key health signal.

- The source estimates December 2025 market cap at about KRW 450-520 billion, with the stock in the KRW 7,000 range near 52-week highs.

- PBR is cited around 2.47-2.9x, while PER may appear negative or very high in some data because of low prior earnings, M&A one-offs, or the sharp share-price rise.

7. Risks and final view

- M&A integration risk: Bringing five companies into consolidation quickly can create unexpected organizational, financial, and operating costs.

- Overhang risk: Convertible bonds or bonds with warrants issued for earlier financing can create dilution pressure when the share price rises.

- End-market cyclicality: A prolonged EV demand slowdown or reduced renewable subsidies can delay the growth case.

- Proof of execution: Revenue contribution from new subsidiaries and operating-margin stabilization are the key quarterly KPIs.

I would not frame Sungho only as a short-term theme stock. The more useful question is whether it can redefine itself from an old condenser maker into an integrated provider of energy and industrial core parts and equipment. 2025 may become the second leap year after 52 years of operating history, but sustained re-rating has to be proven through subsidiary contribution and margin stability.

Sources

- Naver Blog original: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116277095

- Research Alume/Etoday on Sungho film capacitor share: https://www.etoday.co.kr/news/view/2398910

- Judal Sungho investment analysis: https://www.judal.co.kr/?view=stockAI&shareToken=IRO27gQU3iGoSs2R

- Herald Economy report on Audi EV investment: https://mbiz.heraldcorp.com/article/2580454

- MoneyS Porsche/Audi EV film supply report: https://www.moneys.co.kr/article/2020112509018088098

- Korea Economic Daily Porsche/Audi EV report: https://www.hankyung.com/article/2020112466511

- Fortune Business Insights photovoltaic inverter outlook: https://www.fortunebusinessinsights.com/ko/industry-reports/photovoltaic-inverters-market-100947

- Allied Market Research film capacitor market data: https://www.alliedmarketresearch.com/press-release/film-capacitor-market.html

- ChemLOCUS China film condenser plant expansion: https://www.chemlocus.co.kr/news/view/22452?url=L25ld3MvZGFpbHkvMTYvMTUzNT9jYXRlZ29yeT0wMg==

- Investing.com Sungho share price: https://kr.investing.com/equities/sungho-electronics-corp

- AlphaSquare Sungho market data: https://alphasquare.co.kr/home/stock-summary?code=043260

- Toss Securities Sungho live quote: https://www.tossinvest.com/stocks/A043260/order