DEEP RESEARCH · HYUNDAI MOVEX

Hyundai Movex: Smart Logistics Automation in the Physical AI Era

A review of logistics automation, platform screen doors, IT services, and Hyundai Motor Group's Physical AI strategy

0. Bottom line first

Hyundai Movex can be read as an automation-platform company built around logistics automation, which represents about 77.5% of revenue, with PSD and IT services attached. Operating margin fell to 1.5% in 2023 because of new-business entry costs, recovered to 7.2% in 2024, and the source presents 2025 revenue at KRW 405.8 billion.

Official fact: The source lists revenue of KRW 241.0 billion, 210.4 billion, 267.8 billion, 341.3 billion, and 405.8 billion(E) for 2021-2025. Operating margins are 4.5%, 5.7%, 1.5%, 7.2%, and 6.3%(E).

Interpretation: I read Hyundai Movex not as a simple equipment vendor, but as a company trying to supply the operating system for manufacturing logistics by combining hardware, WMS/WCS, robot fleet control, and digital twins. The key is proving non-captive order competitiveness in North America and Europe.

1. Origin and governance

Hyundai Movex was founded in July 2011 when Hyundai Elevator spun off its logistics-equipment business. It internalized IT service capability through the 2017 merger with Hyundai U&I and listed on KOSDAQ in 2019 through a SPAC merger with NH SPAC No.14.

Official fact: As of 2025 Q3, Hyundai Elevator is the largest shareholder with about 55.9%, and friendly holdings including related parties are about 60.2%. The head office is in Jongno-gu, Seoul, while the Cheongna R&D center opened in 2019 as a technology testbed.

Interpretation: Stable governance helps long-cycle R&D and group projects, but investors also need to watch captive dependence and pricing power in affiliate deals.

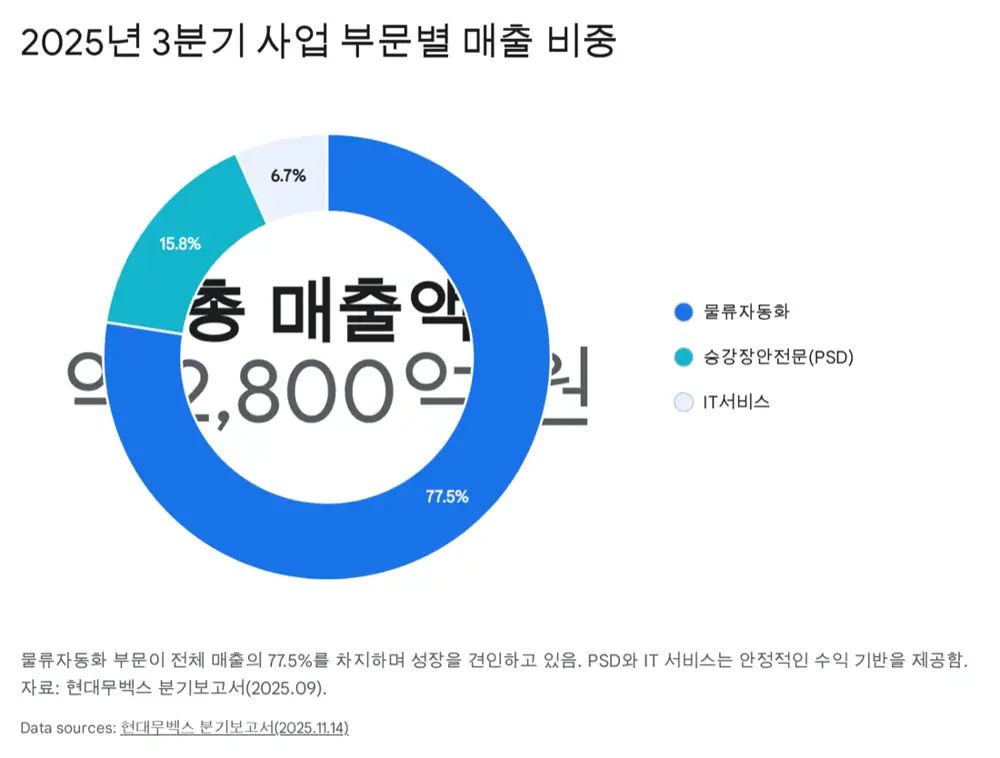

2. Business portfolio: logistics automation is the growth engine

Logistics automation · about 77.5%

The lineup includes AS/RS, stacker cranes, shuttles, conveyors, EMS, RTV, AGV, AMR, transfer robots, wheel sorters, cross-belt sorters, gantry robots, and MRE.

PSD · about 15.8%

The PSD business designs, manufactures, installs, and maintains platform screen doors for metro and light-rail stations. The source cites SIL certification in 2019 and overseas projects such as Sydney Metro.

IT services · about 6.7%

WMS manages inventory, inbound/outbound flow, and facility operations, while WCS controls robots, conveyors, and cranes in real time.

Applications are expanding from retail and food/beverage into batteries, tires, petrochemicals, and pharmaceuticals. Battery-process logistics is a high-value area because it requires cleanliness, precision, and safety.

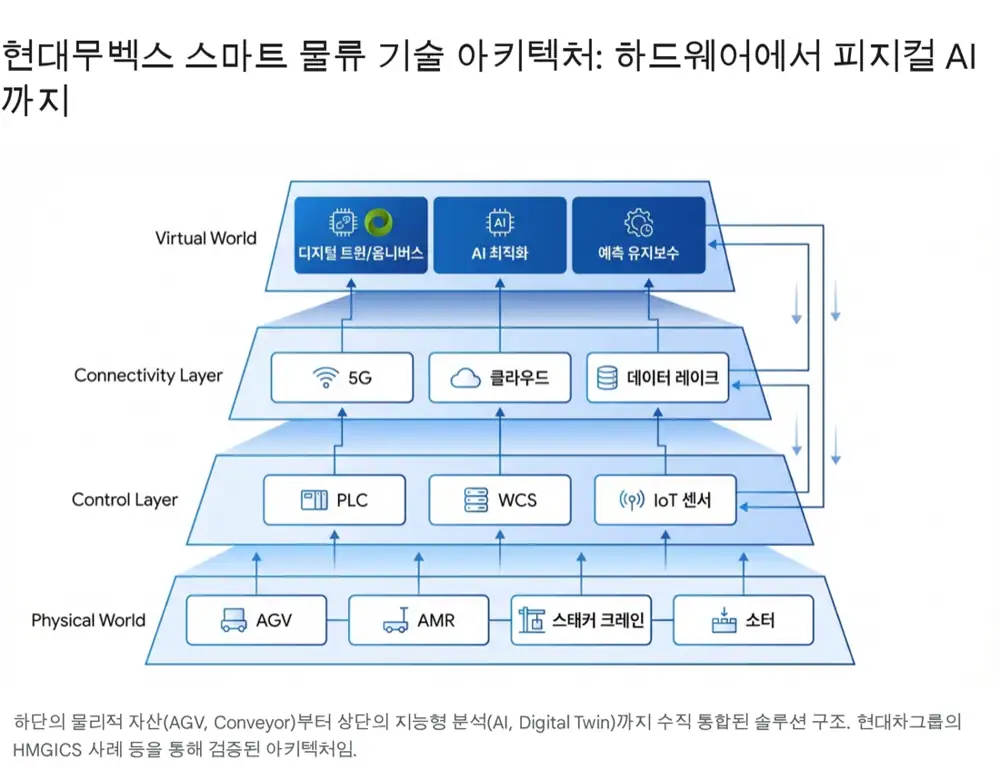

3. Physical AI and digital twins

Official fact: The source says Hyundai Movex applies reinforcement-learning algorithms to AGV/AMR route optimization, collision avoidance, and deadlock resolution, and develops 3D vision and deep-learning recognition for irregular cargo picking and palletizing.

R&D items cited from filings include TRIPLE synchronized RTV, stacker-crane servo control, SLAM algorithm development, and stacker robot development. Combined with Hyundai Motor Group's NVIDIA Omniverse digital twin initiative, the direction is to reduce bottlenecks and errors through virtual factories and virtual commissioning before physical installation.

| Technology | Role in the source | Investor checkpoint |

|---|---|---|

| AGV/AMR | Autonomous movement using LiDAR and SLAM, adapting to layout changes | References, uptime, maintenance revenue |

| Digital twin | Omniverse-based simulation and virtual commissioning | Delivery-time reduction and project margin |

| WMS/WCS | Software layer for facility control and operating optimization | Recurring software revenue versus hardware sales |

4. Results and orders: numbers behind the turnaround

| Item | 2021 | 2022 | 2023 | 2024 | 2025(E) |

|---|---|---|---|---|---|

| Revenue, KRW bn | 241.0 | 210.4 | 267.8 | 341.3 | 405.8 |

| Operating margin | 4.5% | 5.7% | 1.5% | 7.2% | 6.3% |

The source cites 2024 Q3 cumulative revenue of KRW 341.3 billion and operating profit of KRW 16.3 billion, attributing the turnaround to North American project revenue recognition and the removal of low-margin projects. A December 1, 2025 KRW 55.9 billion contract with Kolmar Korea for logistics automation modules and robots is presented as a large order equal to more than 16% of revenue.

5. Risks and checkpoints

- Captive dependence: Group volume is stable, but results can be tied to affiliate investment plans and pricing pressure.

- Independent overseas orders: The U.S., Hungary, China, and Vietnam entities matter, but non-affiliate references are necessary.

- Cost and FX: Steel and other input prices, plus FX volatility on overseas projects, remain risks.

- Technology competition: The company must prove independent AMR and AI-solution capability against Chinese low-cost vendors and global high-end leaders.

6. Overall view

The investment case rests on backlog, expansion into batteries, tires, pharmaceuticals, and retail, diffusion of Hyundai Motor Group smart-factory projects such as HMGICS and HMGMA, and margin improvement from AI and digital twins. The checks are non-affiliate order mix, project-level profitability, and the reality of recurring software revenue.

Sources

- Original blog: https://m.blog.naver.com/PostView.naver?blogId=star_of_self&logNo=224116249137

- Source 1: https://www.the-tech.co.kr/news/article.html?no=40430

- Source 2: https://eureka.hankyung.com/insight/detail/15569

- Source 3: http://www.ttlnews.com/news/articleView.html?idxno=3022251

- Source 4: https://www.tossinvest.com/stocks/A247540/news?symbol-or-stock-code=A247540&contentType=news&contentParams=%7B%22id%22%3A%22financial_202511110803096264%22%7D

- Source 5: https://seo.goover.ai/report/202504/go-public-report-ko-5b98e54c-99d0-42a3-b4bc-e427193cc9f9-0-0.html

- Source 6: https://www.cmesrobotics.ai/en/about/value

- Source 7: https://blogs.nvidia.co.kr/blog/hyundai-motor-group-ces/

- Source 8: https://www.mediapic.co.kr/news/articleView.html?idxno=1446

- Source 9: https://mobile-industrial-robots.com/ko/blog/agv-vs-amr-whats-the-difference

- Source 10: https://www.hankyung.com/article/202512015455L

- Source 11: https://www.hyundai.com/worldwide/en/brand-journal/mobility-solution/unveiling-hmgics-singapore

- Source 12: https://www.hyundai.news/eu/articles/press-releases/hmgics-grand-opening-2023.html

- Source 13: https://drive.google.com/open?id=1dBQUhVZEl1KTneRh53gn4JOYgeqq3zt_PAE5NoVWKoY

- Source 14: https://marketin.edaily.co.kr/News/ReadE?newsId=02341926642296840

- Source 15: https://market.us/report/global-logistics-automation-market/

- Source 16: https://dealsitetv.com/articles/124437

- Source 17: https://www.fdatabot.com/top-10-logistics-robot-manufacturers-and-suppliers-in-the-world/